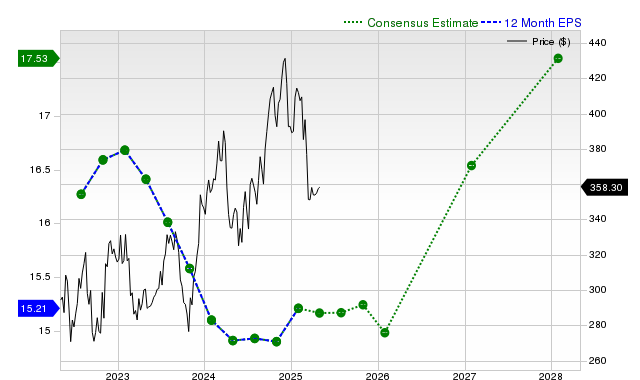

Home Depot (HD) is drawing investor attention, with its shares gaining +2.6% over the last month, trailing the S&P 500 and its industry. Consensus estimates project current quarter EPS at $4.71 (+0.9% YoY) and sales at $45.51 billion (+5.4% YoY), though the current fiscal year EPS is anticipated to decline by 1.3% before a projected 9.2% rebound in the next fiscal year. While HD has consistently surpassed revenue estimates, its last reported EPS missed consensus. The stock holds a Zacks Rank #3 (Hold) and a 'C' valuation score, suggesting it is expected to perform in line with the broader market in the near term.

Home Depot (HD) presents a mixed fundamental picture, characterized by recent stock underperformance and contrasting short-term versus long-term earnings outlooks. Over the past month, the stock's +2.6% return has lagged both the S&P 500 composite and the broader Zacks Retail - Home Furnishings industry. Analyst consensus projects a challenging current fiscal year, with an expected earnings per share (EPS) decline of 1.3% to $15.04, despite a 3.1% rise in revenue. This dynamic suggests potential margin compression. However, the outlook for the next fiscal year is notably stronger, with forecasts calling for a 9.2% rebound in EPS to $16.43 on a 4.4% revenue increase. While the company has consistently beaten revenue estimates over the last four quarters, its most recent report included an EPS miss of -0.84%. The stock's valuation is deemed fair, reflected by a Zacks Value Style Score of 'C', and its Zacks Rank of #3 (Hold) indicates an expectation of in-line performance with the broader market, suggesting the current headwinds and future recovery are largely priced in.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment