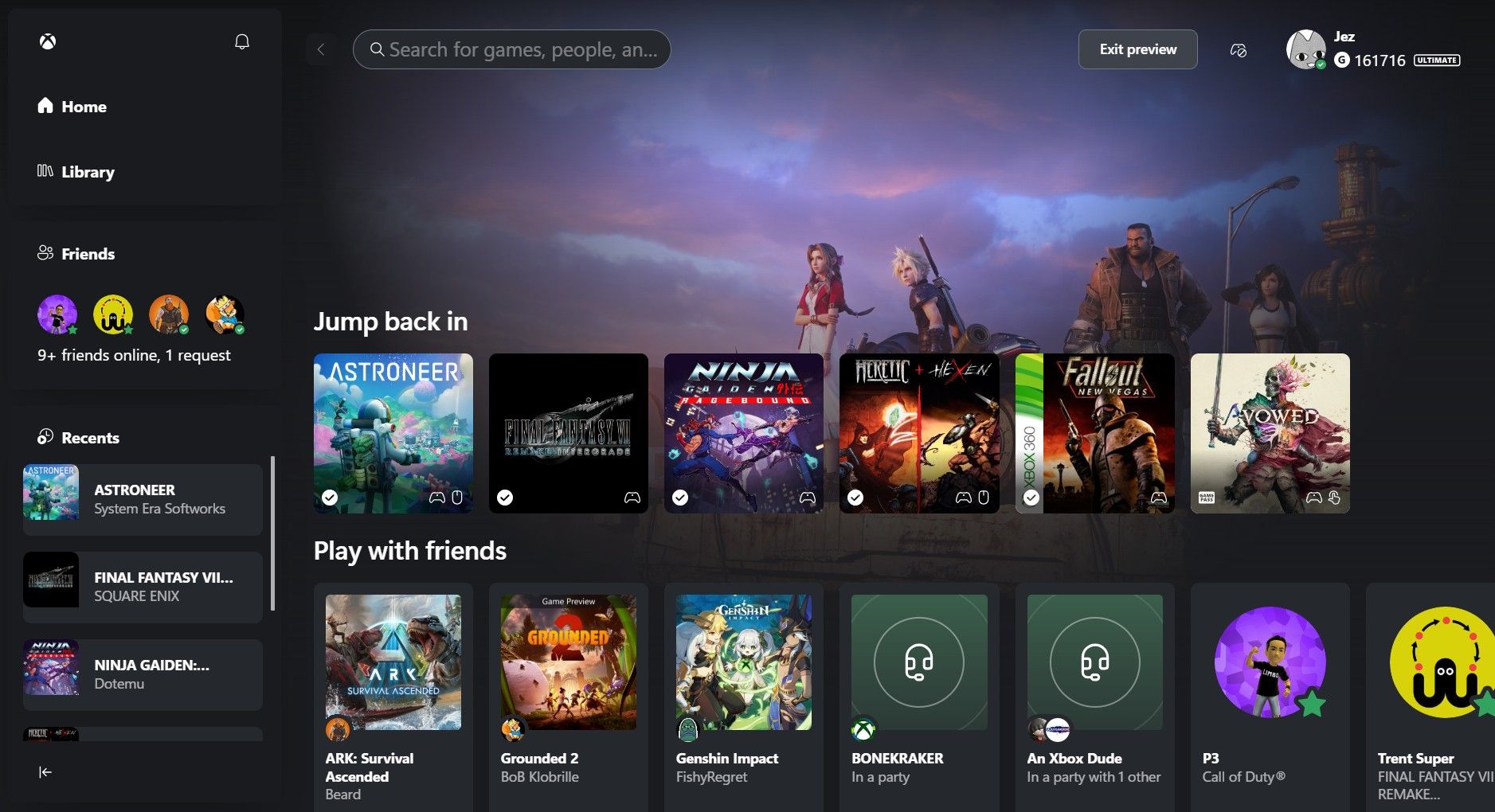

Microsoft has rolled out a preview of a redesigned Xbox Cloud Gaming dashboard (accessible via play.xbox.com) that closely mirrors the Xbox Series X|S console UI and offers TV/handheld and desktop-optimized modes. The service recently exited beta, expanded to new markets, provides cloud access to supported owned games for all tiers, offers 1440p streams to Ultimate subscribers, and is preparing an ad-supported free tier in H1; these moves aim to lower hardware barriers and accelerate user acquisition for Game Pass, though the long-term economic viability remains uncertain.

Market structure: Microsoft (MSFT) and cloud-infrastructure suppliers (NVDA, INTC, and Azure-capex beneficiaries) are primary winners as a successful ad-supported Xbox Cloud Gaming tier shifts value from one-time console sales to recurring platform revenue; expect 3–8% downside to console OEM unit growth (SONY, NTDOY) over 2–4 years if adoption accelerates. Pricing power shifts toward platform owners and publishers who capture recurring revenue and ad yield; consumer DRAM/GPU demand could reallocate from retail to data-center channels, tightening data‑center component pricing while softening retail margins. Risk assessment: Key tail risks include antitrust scrutiny of bundling (EU/US) and economics of streaming (bandwidth + GPU costs) that could make a free tier loss-making; regulatory action or materially higher per-user streaming costs could erase upside. Timeline: immediate (days) — negligible; short-term (weeks–months) — H1 free tier launch is the primary catalyst; long-term (2–4 years) — structural shift in console demand and margin reallocation. Hidden dependencies: broadband penetration (5G/fiber), publisher licensing, and Azure capacity constraints are gating factors. Trade implications: Tactical overweight MSFT (1–3% portfolio) into H1 launch, paired with a modest short on SONY (0.5–1%) to capture relative retail weakness; consider NVDA (1–2%) for data-center GPU exposure. Options: buy a 3–6 month MSFT call spread ~3–5% OTM to capture positive re-rating around the launch, funded by selling further OTM calls. Rotate into cloud infrastructure (NVDA, INTC) and out of consumer hardware (SONY, NTDOY) if quarterly Game Pass/DAU misses by >5% versus consensus. Contrarian angles: Consensus assumes rapid monetization of free cloud tiers; missing is the high per-hour marginal cost — this could compress ARPU by 10–20% before scale ad rates improve. Historical parallels (OnLive) show latency, UX, and economics can stall adoption; unintended consequence: Game Pass ARPU falls while user counts rise, creating an earnings-quality issue that could produce a 5–12% re-rate if not offset by ad/sync revenue growth.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment