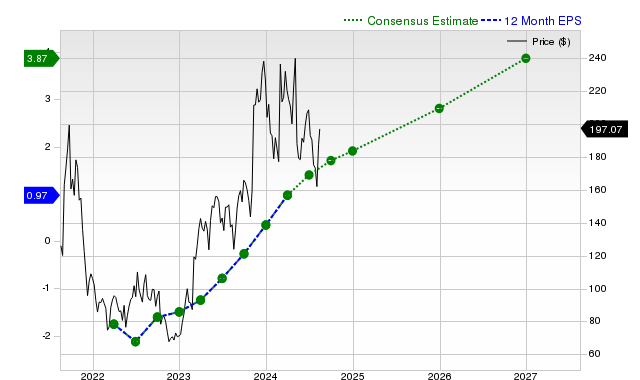

Duolingo (DUOL) has demonstrated strong recent momentum, with shares gaining 14.8% in the past month, underpinned by robust earnings and revenue growth projections. The company anticipates current fiscal year EPS growth of 66% and revenue growth of 36.2%, having consistently surpassed consensus estimates in recent quarters. While its Zacks Value Style Score of 'F' indicates a premium valuation relative to peers, Duolingo's Zacks Rank #1 (Strong Buy) suggests potential for near-term market outperformance.

Duolingo, Inc. (DUOL) is exhibiting strong fundamental momentum, which has translated into significant stock price appreciation of +14.8% over the past month, outpacing the S&P 500 composite's +4.8% gain. The company's operational strength is highlighted by its last reported quarter, where it posted a +41.5% year-over-year revenue increase to $252.26 million and an EPS of $0.91, representing a substantial +65.45% surprise over consensus estimates. This performance is part of a consistent trend, with Duolingo surpassing revenue estimates in each of the last four quarters and EPS estimates in three of them. Forward-looking consensus estimates project this growth will continue, with expectations for a +66% increase in EPS and a +36.2% rise in revenue for the current fiscal year. Despite these robust growth metrics and a Zacks Rank #1 (Strong Buy) suggesting near-term outperformance, a significant counterpoint exists in its valuation. The stock receives a Zacks Value Style Score of 'F', indicating that it is trading at a premium relative to its peers, a critical risk factor for investors to consider.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment