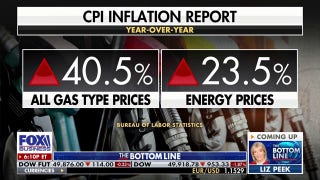

The article argues that secretly moving more than 100 million barrels of oil through the Strait of Hormuz over the past month has added roughly 3 million barrels per day to global supply, helping cap oil prices and reduce inflation pressure. It cites WTI falling from a peak of $113 to $90, gasoline easing from $4.56 to $4.15, and headline CPI at 4.2% year on year versus 2.9% ex-food and energy. The piece frames the geopolitical and energy developments as supportive for lower oil prices and less restrictive Fed policy.

The key market implication is not the near-term absolute level of crude, but the implied reduction in geopolitical tail risk premium. If maritime flows through a chokepoint can be preserved without a visible force posture, the market starts pricing a higher probability that oil supply disruption risk is being actively managed rather than merely threatened — that compresses the upside skew in crude more than it changes spot immediately. The second-order effect is on rate volatility: breakeven inflation and front-end real yields should soften if energy stays contained, which matters more for equities than the headline CPI print itself. The beneficiaries are downstream users with the most elastic margins to fuel input costs: airlines, parcel/logistics, trucking, chemicals, and consumer discretionary transport. The losers are not just energy producers; it is also any long-duration inflation hedge that has been leaning on a persistent energy shock, because a fast fade in gasoline can remove the marginal justification for sticky 3%+ inflation in the next 1-2 prints. Defense and maritime-security contractors may see less incremental urgency if the market concludes the corridor can be stabilized with limited escalation. The contrarian risk is that this is a fragile, narrative-driven supply bridge rather than durable capacity. If the corridor is re-threatened, if insurers widen risk premia, or if there is a single visible disruption, crude can gap higher very quickly because traders will have been leaning short volatility on the assumption that the premium is already fading. Conversely, if oil continues to drift lower over the next 2-6 weeks, the bigger market trade becomes not energy downside but a rotation into rate-sensitive cyclicals and small caps via lower inflation and easier financial conditions. From a policy lens, the market may be underestimating how much a few tenths lower in energy inflation can change the Fed's reaction function at the margin. That does not imply imminent cuts, but it does reduce the odds of a hawkish surprise if core services cool alongside energy. The trade setup is asymmetric because the upside to inflation from this channel is capped while the downside to oil can extend quickly if positioning is still crowded long.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.15