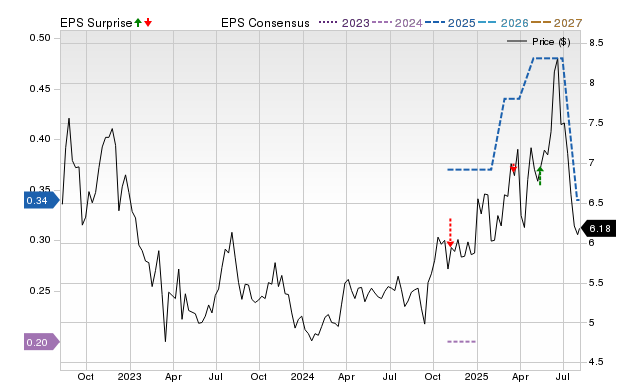

Epsilon Energy Ltd. (EPSN) is projected to report a significant year-over-year increase for the quarter ended June 2025, with consensus estimates at $0.08 EPS (+100%) and $11.85 million revenue (+62.1%). However, the consensus EPS estimate has undergone a substantial 70% downward revision over the past 30 days. Coupled with a 0% Zacks Earnings ESP and a Zacks Rank of #4, the company is not considered a strong candidate for an earnings beat ahead of its August 13 release, suggesting limited upside potential from a positive surprise.

Epsilon Energy Ltd. (EPSN) presents a conflicting pre-earnings profile for its quarter ending June 2025. While consensus estimates project substantial year-over-year growth, with EPS expected to double to $0.08 and revenue to climb 62.1% to $11.85 million, this positive surface-level outlook is severely undermined by recent analyst activity. The consensus EPS estimate has been revised downward by a significant 70% over the last 30 days, indicating a sharp deterioration in sentiment regarding the company's near-term profitability. This bearish turn is corroborated by quantitative models; EPSN holds a Zacks Rank of #4 (Sell) and an Earnings ESP of 0%, a combination that historically makes an earnings beat difficult to predict. Furthermore, the company's track record shows only one consensus EPS beat in the last four quarters, suggesting a limited history of positive surprises. The primary takeaway is that while the year-over-year comparison appears strong, the negative revision trend and weak predictive indicators suggest a high degree of risk and low potential for a positive catalyst from the upcoming report on August 13.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30

Ticker Sentiment