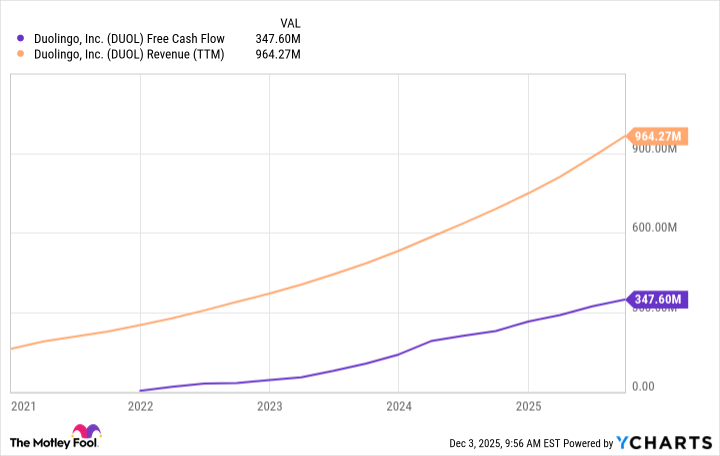

Duolingo reported 135 million monthly active users as of Q3 2025 and 11.5 million paying subscribers (which account for ~84% of revenue), with paying subscribers up 34% year-over-year. The company has generated nearly $350 million of free cash flow over the last 12 months, and management is pursuing product expansion into areas such as chess, math and literacy to broaden monetization beyond language learning; less than 10% of total users currently pay. Despite a ~66% share-price decline, the author argues the combination of high growth, strong monetization and positive free cash flow makes the stock an attractive buy.

Market structure: Duolingo (DUOL) is the primary beneficiary — 135M MAU, 11.5M subscribers (84% of revenue) and 34% YoY paid growth imply strong pricing power in a low‑marginal‑cost digital product; traditional in‑person language schools and ad‑heavy freemium players (lower conversion) are the losers. Competitive dynamics favor scale: high FCF ($~350M LTM) and low incremental cost create room for margin expansion and selective price increases, but rapid AI commoditization could erode differentiation within 12–36 months. Risk assessment: Tail risks include AI commoditization of tutoring, stricter data/privacy regulation, a cyclical ad recession cutting non‑subs revenue, and a surprise decline in retention (churn >10%/yr would kill LTV economics). Immediate (days) — rebound rallies; short (weeks–months) — subscriber/ARPU prints and new‑product adoption; long (quarters–years) — TAM expansion into math/chess hinges on retention conversion staying ≥10% of MAU. Hidden dependency: CAC trending up would compress LTV/CAC; monitor cohort LTV and CAC monthly. Trade implications: Direct: tactical long DUOL with protective downside (see decisions). Relative value: long DUOL vs short CHGG and/or COUR over 6–12 months betting on engagement-driven monetization benefits. Options: preferred structure is a 9–12 month call‑spread to cap premium versus buying naked calls; consider selling OTM puts 15–20% below entry to collect premium and lower basis. Rebalance away from loss‑making edtech and into proven FCF generators if rates rise. Contrarian angles: Consensus may underweight Duolingo’s ability to upsell from <10% conversion — 3–5× conversion upside is plausible if product expansion succeeds. The market may be over‑penalizing DUOL for growth‑to‑value rotation (66% drop) — a disciplined buy with strict metric triggers could exploit mispricing. Unintended risk: gamification may not scale to new subjects, producing stretched SG&A with little incremental retention.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.65

Ticker Sentiment