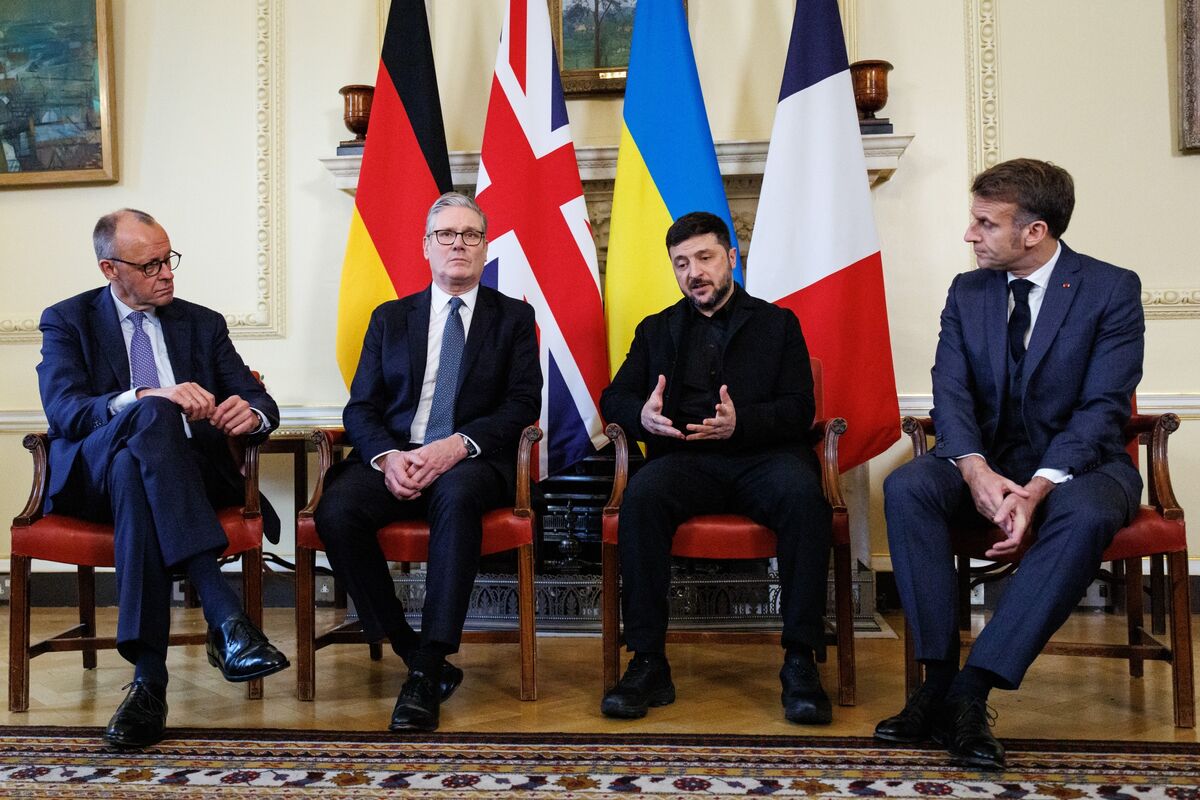

Ukrainian President Volodymyr Zelenskiy said there is no consensus on key elements of a US-brokered plan to end the war with Russia, noting that sensitive issues — including the future of the Donbas region and security guarantees — remain unresolved. Speaking to Bloomberg ahead of meetings in London with UK, French and German leaders, his comments undercut recent optimism about a near-term settlement and prolong geopolitical uncertainty that could sustain risk premiums in energy, defense and regional markets.

Winners are defense primes (U.S./EU aerospace & munitions suppliers) and commodities tied to energy and grain; losers are Ukraine-exposed assets, European energy-importers and discretionary sectors sensitive to regional supply disruptions. Expect incremental defence procurement to add measurable revenue tailwinds—anticipate 5–15% revenue uplift for major primes over 12–24 months if current uncertainty persists—while airlines and tourism in Europe face 10–30% downside risk to near-term cash flows from renewed restrictions or Black Sea disruption. Competitive dynamics favor large primes (RTX, LMT, GD) with scale, aftermarket and long lead-time contracts; small vendors and subcontractors (specialty electronics, precision munitions) will see pricing power but face capacity constraints. Supply bottlenecks for artillery, air-defence and semiconductors mean lead times of 6–24 months and spot price spikes (potentially +20–50% for constrained components) before new capacity comes online. Cross-asset: expect short-term safe-haven flows into USD, USTs and gold (GLD/IAU) with transient drops in 10y yields followed by higher risk premia pricing if conflict prolongs; oil is the primary commodity shock vector — a moderate escalation could push Brent +$5–$15 in weeks, widening EM FX stress and equity implied vols by 30–70% in affected names. Tail risks include NATO direct involvement, major cyber attacks on energy grids, or a near-term negotiated deal — each would flip asset performance sharply within days to months. Key catalysts to watch over 0–90 days: London summit outcomes, EU/US funding votes, and any material battlefield events. Contrarian risk: markets may be overpricing perpetual escalation—if a deal materializes within 2–3 months, defense equities could see 15–30% mean reversion; conversely, underinvestment in munition stockpiles risks persistent supply shocks and sustained margin expansion for producers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25