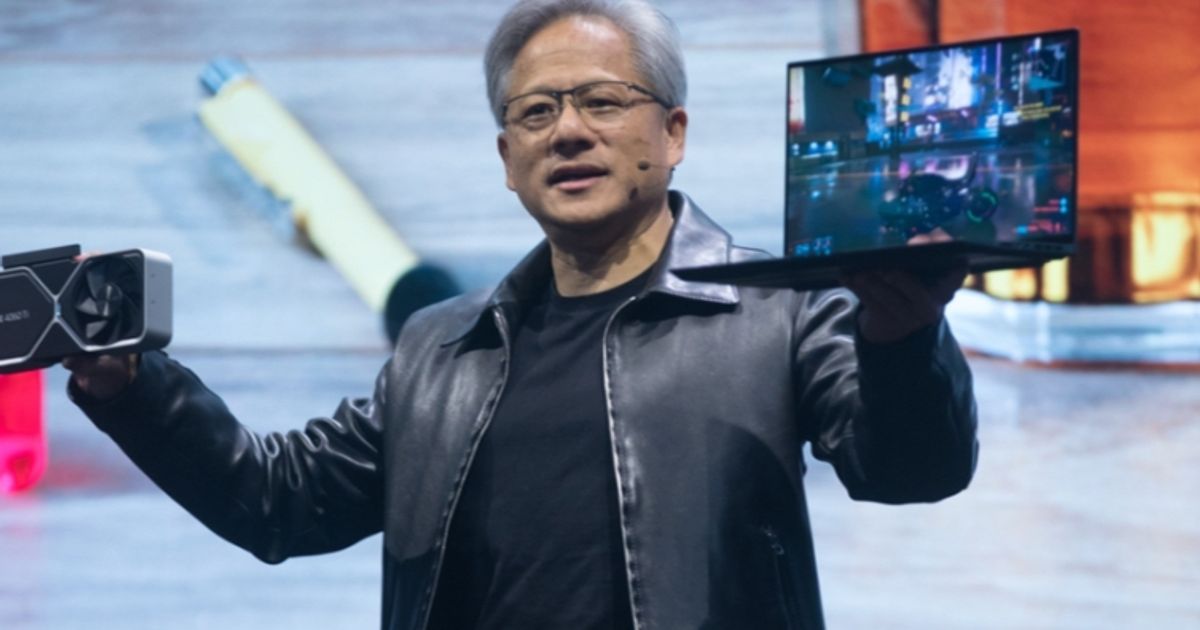

At CES 2026 Nvidia CEO Jensen Huang framed the company as a platform leader in "physical AI," unveiling new AI models and specialized hardware for humanoid robotics used by partners including Boston Dynamics, Caterpillar, LG Electronics and NEURA Robotics. Nvidia also introduced Alpamayo, a family of large-scale autonomous-vehicle training models drawing interest from Lucid, Uber and Berkeley DeepDrive, positioning virtual training and robotics platforms as revenue-expanding opportunities across manufacturing and logistics markets the company estimates at $50 trillion.

Market structure: Nvidia’s CES push strengthens its role as the platform provider for physical-AI, likely increasing GPU/HBM demand and software services revenue over 6–24 months. Direct winners: NVDA (platform fees, chips), cloud providers (training cycles), industrial OEMs (CAT, LG) that adopt off-the-shelf stacks; losers: small custom-chip vendors and software vendors that charge per-vehicle runtime if Nvidia captures the training-to-deploy standard. Expect pricing power for high-end accelerators to persist near-term unless memory supply normalizes; model-training hours could grow 30–60% YoY in target verticals. Risk assessment: Tail risks include U.S./export controls on advanced GPUs or HBM (low probability, high impact), regulatory constraints on humanoid deployment, or a large training-accident PR event; these could cut 20–50% off near-term growth projections. Time horizons: days – share-price knee-jerk on CES; weeks–months – order announcements and partner integrations; 12+ months – material revenue from robotics only if OEM adoption scales. Hidden dependencies: HBM supply, datacenter capacity, and software monetization cadence (licensing vs. one-off) are critical second-order drivers. Catalysts: partner pilot wins, SG&A disclosure of robotics revenue, or public safety incidents. Trade implications: Primary trade is long NVDA exposure to capture platform monetization; prefer structured options to limit capital and vega. Tactical longs: selective industrial plays (CAT) for on-prem robotics and logistics; avoid allocating material capital to Lucid (LCID) or Uber (UBER) based solely on model interest – their value capture is uncertain. Rebalance into semis/automation versus legacy auto/EV hardware over next 3–9 months. Contrarian angles: The market may be overpricing immediate monetization from humanoid robotics—revenue realization likely 2+ years out—meaning NVDA’s current premium is on optionality, not guaranteed cash flow. Standardization could paradoxically commoditize some middleware, enabling rivals or open-source stacks to capture share. Historical parallel: early autonomous stacks promised rapid monetization but required multi-year virtuous cycle of data, compute, and regulatory clearance; expect similar delayed payoff here.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment