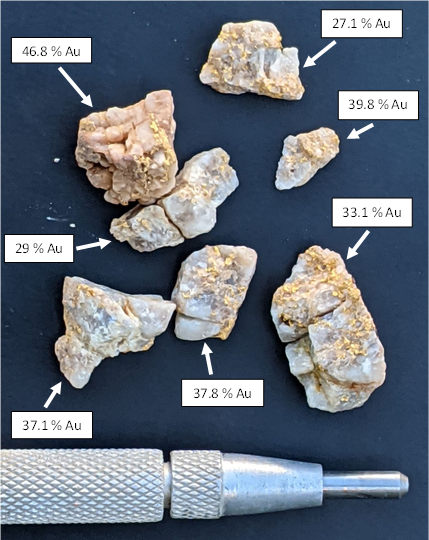

Au Gold Corp (TSXV: AUGC) agreed to acquire a 100% interest in the 11,663-hectare Havelock gold‑antimony project in Victoria, Australia from Leviathan Gold Australia for C$75,000 (C$10k on signing, C$65k on TSXV acceptance) plus 5 million AUGC shares, with contingent payments of C$3/oz for discovered resources and legacy payments to Mercator (A$1/oz discovered and A$1/oz produced, each capped at A$1M). Leviathan will hold 5,000,000 shares (≈11.16% post-close); the project hosts historical high‑grade workings and notable 2021 drill intercepts (e.g., 21LEV002: 1.11 m @ 56.40 g/t Au and other multi‑gram intercepts), and AUGC is preparing an NI 43-101 and plans rapid follow-up exploration pending TSXV approval. The transaction modestly dilutes shareholders but materially expands AUGC’s project portfolio; near-term market impact is likely low absent further exploration results that convert historical and drill signals into formal resources.

Market structure: AUGC (TSXV:AUGC) and service contractors (drillers, assayers) are the immediate winners — AUGC gains a Victorian epizonal gold ticket with near-term drill targets while LGA/Leviathan (TSXV:LVX) receives 11.16% equity and tail royalties. Major producers (e.g., Agnico Eagle AEM) see negligible direct impact; global gold supply/demand and bullion prices won’t move meaningfully unless multiple Victorian discoveries scale to multi-M+ oz, which is a multi-year outcome. Antimony upside is local: meaningful antimony production would be a positive NPV kicker but unlikely to perturb global antimony prices in the next 3–5 years. Risk assessment: Key tail risks are regulatory/First Nations disputes, groundwater pumping constraints, metallurgical complexity for antimony recovery, and dilution from AUGC financing rounds — each can destroy project economics; probability of a negative drill result is high (>50%) given anecdotal historic sampling. Time horizons: immediate (days) for TSXV acceptance and Early Warning Report; short-term (3–9 months) for permitting and initial drill assays; long-term (2–6 years) for resource definition and potential production. Hidden dependencies include continuity of the quartz reef system below historic workings and antimony metallurgy; catalysts are NI 43‑101 filing (within 30–60 days) and first drill assays (3–6 months). Trade implications: Direct play — establish a small, staged long in AUGC (2–3% portfolio) only after TSXV acceptance and NI 43‑101 are posted; add upon 1st positive drill intercept >5 g/t over ≥2 m. Pair trade — long AUGC vs short the GDXJ (market cap weighted junior index) is logical: capture idiosyncratic re‑rating while hedging gold price risk. Options — if liquid, buy 9–12 month call spreads on AEM (1–2% notional) to play regional rerating with capped downside. Rotate 1–2% of passive gold ETF exposure (GDX) into targeted Victorian exploration exposure. Contrarian angles: Consensus underprices the antimony co‑product and coarse-nugget potential — a single high-grade reef could rerate a microcap by 2–4x, but history shows only a tiny fraction of Victorian targets scale. The market may overreact positively to early surface nuggets and underreact to drilling risk; treat initial assays as high-volatility binary events. Unintended consequences: upfront share issuance (5M shares) and uncapped discovery payments create overhang and financing pressure — watch subsequent financings and insider/major holder activity closely.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35