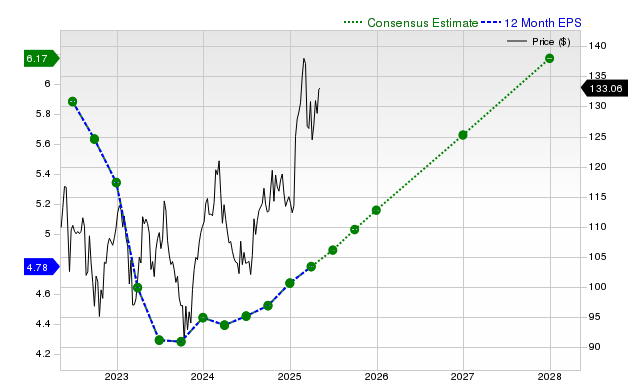

Abbott Laboratories (ABT) has been a trending stock, though its shares returned +1.9% over the past month, underperforming the S&P 500's +5.1%. Despite this recent market underperformance, analysts project robust growth, with current quarter EPS expected to rise 9.7% to $1.25 and full-year revenue anticipated at $44.7 billion (+6.6%). The company's consistent earnings beats (3 of last 4 quarters) and a Zacks Rank #2 (Buy) suggest potential near-term market outperformance driven by favorable earnings estimate revisions, even as its valuation is assessed as at par with peers.

Abbott Laboratories (ABT) presents a case of solid fundamental prospects contrasted with recent market underperformance. Over the past month, the stock's +1.9% return has lagged the S&P 500 composite's +5.1% gain. However, forward-looking indicators are robust, with consensus estimates pointing to double-digit earnings growth for both the current fiscal year (+10.5%) and the next (+10.0%). This is supported by healthy revenue growth projections, which are expected to accelerate from +6.6% in the current fiscal year to +7.6% in the next. While the company's recent execution has been mixed, with a slight revenue miss (-0.56%) in the last quarter and topping revenue estimates in only two of the last four quarters, it has consistently surpassed EPS estimates in three of those four periods. Despite a minor downward revision to the current quarter's consensus EPS (-0.4%), the overall positive trend in earnings estimates has earned the stock a Zacks Rank #2 (Buy). Valuation appears fair, with a 'C' grade indicating it trades at par with its peers, suggesting the positive outlook may be partially priced in.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment