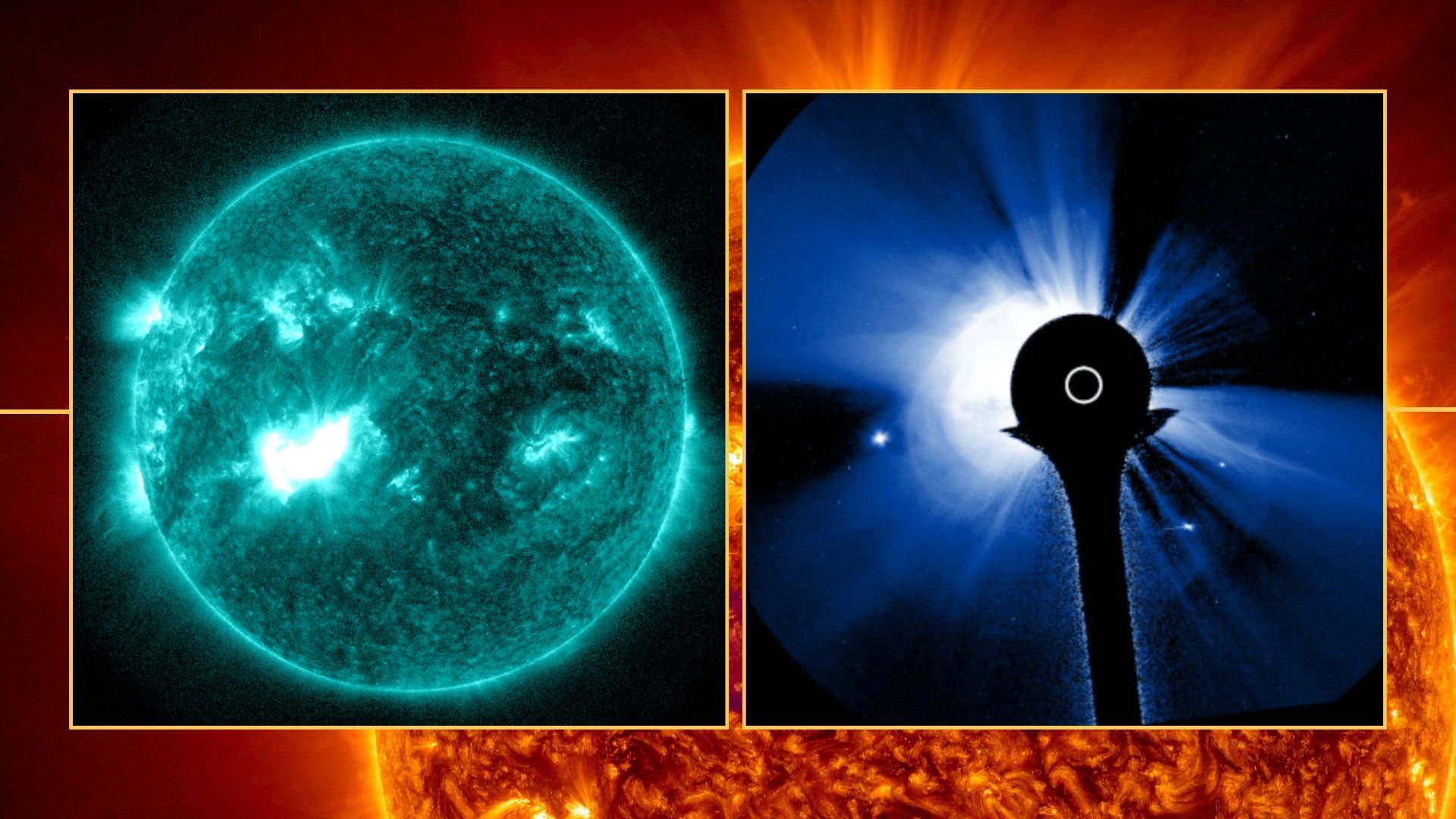

The Sun produced an X1.9-class solar flare from sunspot AR4341 and an Earth-directed coronal mass ejection (CME) currently forecast to arrive within ~24 hours; the flare triggered R3 radio blackouts across the sunlit Americas. UK Met Office guidance warns the CME could produce strong (G3) to severe (G4) geomagnetic storm conditions if its magnetic Bz component is southward, potentially disrupting satellite operations, degrading GPS navigation and increasing atmospheric drag on spacecraft; operators and insurers of satellite, navigation-dependent and aviation assets should monitor upstream probes (DSCOVR, ACE) for definitive magnetic-field sampling.

Market structure: Near-term winners are defense/space integrators (Lockheed Martin LMT, Northrop Grumman NOC, L3Harris LHX, RTX) and specialist satellite operators/in-orbit-servicers (Iridium IRDM, Maxar MAXR) due to expected demand for hardened systems; losers in a short window are GPS-reliant transport/logistics (JETS ETF, UPS UAL, FDX) if navigation outages occur. Pricing power should favor prime contractors with long backlog; expect modest revenue tailwinds (mid-single-digit % uplift) over 3–24 months if regulators fund resilience programs. Cross-asset: a transient risk-off could lift US 2Y yields -5–15bps and push gold (GLD) +1–3% intraday; FX: slight bid for USD and JPY as safe-havens; commodities largely unaffected except for selective industrial metals if prolonged satellite loss disrupts mining ops. Risk assessment: Tail risk of a Carrington-scale event is very low (<1% annual), but a G3–G4 hit (article-consistent) has 10–30% probability — capable of satellite anomalies, increased atmospheric drag, and localized grid impact. Immediate horizon (24–72h): GPS/shortwave blackouts and satellite comms glitches; short-term (weeks–months): anomaly investigations, insurance claims, early contract wins; long-term (12–36 months+): accelerated utility and defense capex (+3–10%). Hidden dependencies include insurer exposure, semiconductor lead times (12–24 months) and government procurement cycles that can amplify or delay revenue realization. Key catalysts: DSCOVR/ACE Bz readouts (threshold Bz <= -10 nT for >3 hrs), NOAA advisories and reported satellite anomalies. Trade implications: Tactical long exposure to LMT, LHX, RTX sized 1–2% each for 3–12 months to capture resilience program spending; buy 3-month call spreads on LHX (5–15% OTM) sized 0.5% notional to leverage upside. Short JETS ETF 0.5–1.0% or buy 2-week ATM puts to capture operational disruption risk while DSCOVR/ACE data is unsettled; hedge portfolio with 1% GLD to protect against risk-off. Use conditional triggers: if DSCOVR/ACE Bz <= -10 nT sustained 3+ hrs, add 50% to defense/space longs and close JETS short. Contrarian angles: The market will likely overreact intraday; consensus underestimates low-frequency capex upside for primes — buy-on-dip in LMT/LHX if shares fall >5% intraday. Conversely, selling small-cap satellite names with weak balance sheets (e.g., speculative OTC names) is attractive if sector ETF/prime rallies >10% without fundamental orders; historical parallels (1989/2003 grid events) show policy-driven capex follows weeks–months after events, not immediately, so patience on revenue realization is required.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.10