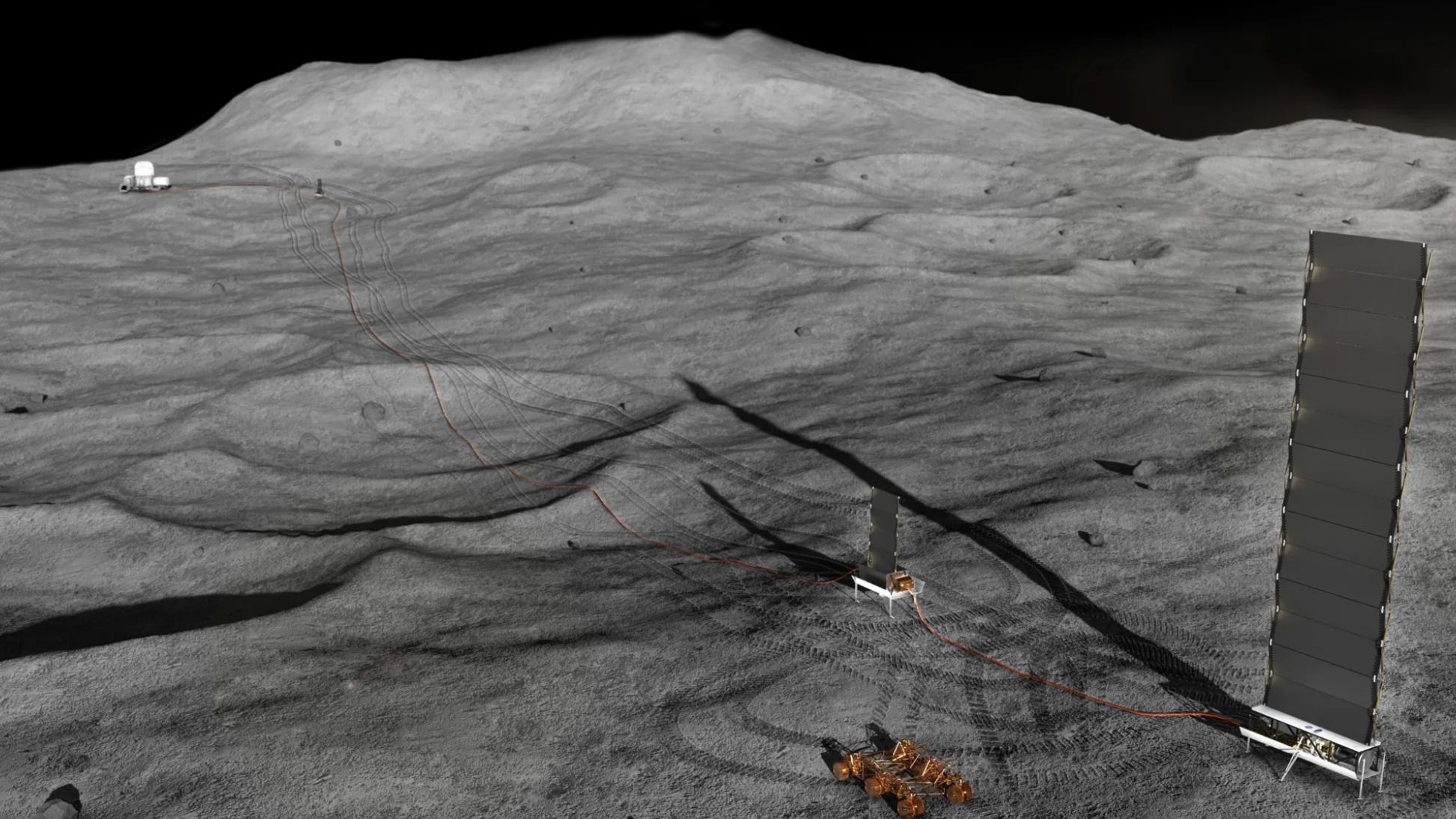

NASA and the U.S. Department of Energy signed a memorandum of understanding reaffirming a joint effort to develop a fission-based nuclear reactor intended to power lunar surface bases, with a target to have a reactor ready to launch by 2030 pursuant to a presidential executive order. Agency leaders framed the move as necessary for sustained crewed operations on the Moon and future deep-space missions, leveraging decades of U.S. experience with space nuclear systems (RTGs) and signaling potential government contracting opportunities for nuclear and space-defense suppliers.

Market structure: The primary winners are nuclear reactor integrators and engineering contractors that can win DOE/NASA build-and-test awards (e.g., BWXT, Lockheed Martin LMT, Northrop Grumman NOC) and launch service suppliers paid per-kg to the lunar surface. Commodity uranium miners (CCJ, UEC) and broad solar installers are weak candidates — lunar fission uses specialized fuel and DOE stockpiles, so spot-uranium demand impact is limited through 2030. Expect concentrated pricing power for a small set of suppliers; supply constraints in radiation-hardened electronics and space-qualified heat rejection systems will push margins for niche vendors for 3–7 years. Risk assessment: Tail risks include program cancellation or de-funding with an administration change (20–40% probability over 4 years), technical failure or catastrophic launch loss (10–15%), and export/regulatory constraints on HEU use that delay timelines. Realistic timing risk: 50% chance the 2030 target slides to 2032–2035; cost overruns could be 2x–3x initial budgets, pressuring contractor margins and prompting fixed-price contract renegotiations. Key hidden dependencies: congressional appropriations cycles (annual), DOE fuel availability, NRC/ODC approvals, and launch insurance markets. Trade implications: Direct plays — overweight A&D contractors and BWXT-type niche suppliers for 12–36 months; keep uranium miners underweight. Recommended instruments: 12–24 month LEAPS calls on BWXT (buy up to 0.5–1.5% notional) and tactically add LMT/NOC/RTX longs (0.5–1% each) on pullbacks >5%. Pair trade: long BWXT vs short CCJ (size 1:1 notional) to capture integrator vs commodity divergence; use stop-loss at 18% and target +35–50% on winners. Rotate 2–5% into Aerospace & Defense ETFs (ITA/XAR) and reduce pure renewable installer exposure by 1–2%. Contrarian angles: The consensus that “nuclear = uranium miners” is wrong for the moon program; DOE/stockpile fuel and HEU/security constraints mute spot-uranium upside — miners are likely overvalued on this narrative in the next 12–36 months. Historical parallel: Apollo-era winners were systems integrators and defense primes, not commodity suppliers. Unintended consequences include tighter export controls and geopolitical escalation that could increase defense-budget tailwinds — favor liquid large-caps over small illiquid names where schedule risk is binary and bankruptcy risk exists.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.05