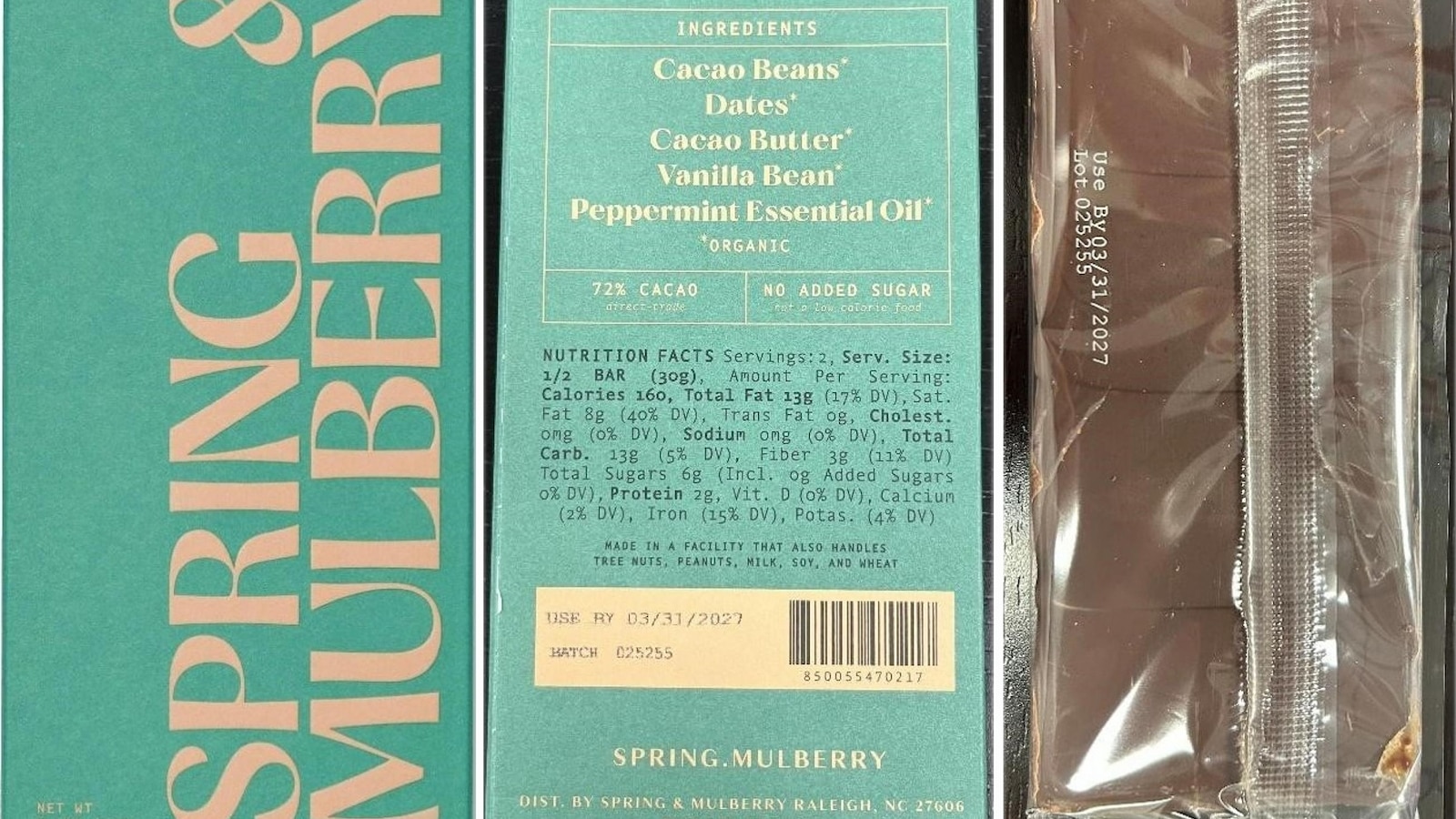

Spring & Mulberry, a Raleigh, N.C. chocolatier, voluntarily recalled one lot (Lot No. 025255) of its 2.1-ounce Mint Leaf Date Sweetened Chocolate Bars on Jan. 12 after routine third‑party lab testing flagged potential Salmonella contamination; no illnesses have been reported. The recall is limited to a single lot and the company is offering refunds upon submission of a photo of the lot code, implying minimal near‑term financial impact, though investors should monitor for any expansion of the recall, regulatory action or reputational consequences.

Market structure: This isolated recall of a single lot by a tiny brand is a negative idiosyncratic event for artisanal/DM-to-consumer chocolatiers but a modest relative tailwind for large-cap confectioners (HSY, MDLZ, KHC) and major grocers (WMT, AMZN) as consumers trade safety for scale; expect 1–3% incremental share shift toward national brands over 3–6 months in affected regional channels. Pricing power is largely unchanged at category level; however boutique players could see revenue hits >10% in quarters where recalls force delisting or inventory destruction, amplifying consolidation risk. Commodities (cocoa) and FX are unaffected; credit spreads on small private food companies could widen modestly if recalls aggregate. Risk assessment: Tail risks include a multi-state outbreak or class-action that raises recall costs into mid-six figures or higher for a small firm, prompting regulatory scrutiny and retailer delistings within 30–90 days; worst-case industry reputational damage could accelerate private-label testing mandates within 6–18 months. Immediate (days) impacts are PR and returns/refunds; short-term (weeks–months) are wholesale delisting and manufacturer audits; long-term (quarters–years) are regulatory standards, higher compliance capex and M&A of weakened independents. Hidden dependencies: third-party lab reliability and retailer shelf-space rules; catalysts to watch are FDA enforcement notices, >3 linked illnesses, or major retailers issuing removal orders. Trade implications: Direct plays favor modest long positions in HSY and MDLZ (quality defensive confection exposure) sized 1–2% of portfolio with a 3–9 month horizon and 6% stop-loss; consider buying 3–6 month call spreads on ERF.PA (Eurofins) or SGSN.SW to capture incremental testing demand, risk budget 0.5% each. Pair trade: long HSY vs short a small-cap specialty food name exposed to DTC/organic chocolate concentration (e.g., SFM or targeted private-equity-backed names) to express consolidation; use 1:1 dollar neutral sizing. Options: sell short-dated hedges on small-cap food names if volatility spikes >25% implied. Contrarian angles: The market will mostly ignore single-lot recalls — consensus underestimates the cumulative regulatory tightening if several small recalls cluster; a contrarian play is buying select small-cap food makers that pass enhanced third-party audits (buy on evidence of audit completion within 30–60 days) because they become acquisition targets. Reaction is likely underdone for testing labs and overdone for isolated artisanal brands; historical parallels (small recalls in 2015–2018) show brand consolidation over 12–24 months, not category demand collapse. Unintended consequence: heavy retailer delisting of niche SKUs could create short-term shelf vacancies that incumbents fill, accelerating share gains for large brands.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00