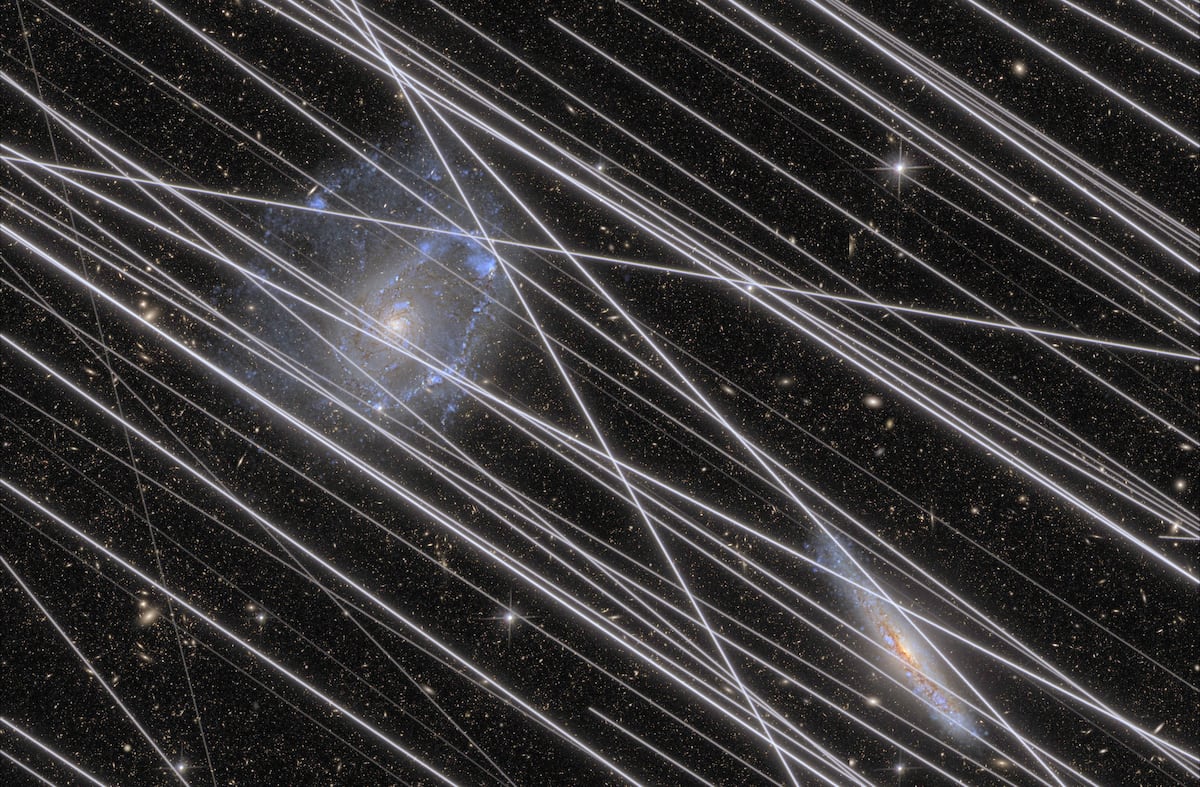

A NASA-led study warns that large satellite constellations—with industry plans exceeding 500,000 deployments—could contaminate a significant fraction of space-telescope imagery, projecting roughly 40% of Hubble images and up to 99% of SPHEREx observations affected under a 560,000-satellite scenario and predicting 96% contamination for ESA’s ARRAKIHS. ESA and ARRAKIHS team members dispute the worst-case ARRAKIHS estimate, citing final pointing/orientation and operational redundancy that they say would limit impact to around 1% of images. The findings highlight potential scientific degradation, increased costs for repeat observations, and broader space-debris and operational risks that could prompt regulatory scrutiny and operational changes for megaconstellation operators.

Market structure: Megaconstellation plans (≈500k+ satellites) shift demand toward launch providers, satellite builders, and space-traffic-management (STM) services while creating headwinds for smaller launch pure-plays and for astronomy-dependent science outputs (Hubble contamination ~40%, ARRAKIHS up to 96%, SPHEREx up to 99%). Pricing power concentrates with vertically integrated players able to scale (SpaceX private, Amazon/AMZN Kuiper) and with defense primes that win government STM and debris-mitigation contracts (Lockheed LMT, Northrop NOC, L3Harris LHX). Revenue pools reallocate from pure science grants to operational STM, insurance and collision-avoidance software. Risk assessment: Tail risks include regulatory caps or slowdowns (FCC/ITU/ESA interventions within 3–12 months) that could cut launch cadence by >30%, and a Kessler-cascade collision scenario (low probability, >12–36 months) that would spike insurance and grounding costs. Hidden dependencies: small-launch firms (RKLB) rely on predictable mass-market rides; vertical integration by SpaceX can compress margins by 15–40% in years. Catalysts: high-profile collision/nearmiss, major insurer repricing (within 6–12 months), or national security directives accelerating STM spend. Trade implications: Favor long exposure to STM and defense primes with proven government contracting (2–3% position in LHX or NOC, 12–36 month horizon) and selective imagery/analytics names (PL, MAXR) that monetize data, while hedging/sizing against launch commoditization. Short or hedge pure small-launch risk (RKLB) via 6–12 month put spreads 15–25% OTM; buy optionality on primes (long-dated calls) to capture discrete contract wins. Contrarian angles: Consensus fears about “astronomy ruin” understate government response — expect accelerated public funding for STM and telescope hardening (benefit to LMT/NOC/LHX) within 12–24 months. The market may over-penalize all launch players; winners will be those with integrated services (manufacture+ops+STM) rather than pure launch. Short-term volatility around regulatory headlines will create tactical entry points — set thresholds (e.g., FCC cap proposals or insurer rate hikes) to scale positions.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35