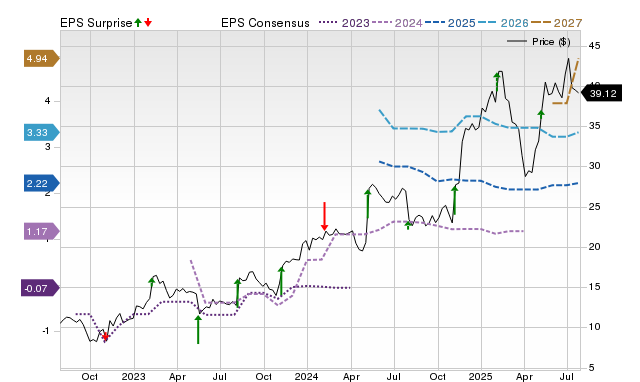

Kyndryl Holdings (KD) is forecast to report Q2 2025 earnings of $0.37 per share, a 184.6% year-over-year increase, on $3.8 billion in revenue, up 1.6%. However, the consensus EPS estimate has been revised 8.57% lower over the past 30 days, and the company's Zacks Earnings ESP of -4.05% suggests recent bearish analyst sentiment. Combined with a Zacks Rank of #3, this indicates it is difficult to conclusively predict an earnings beat for KD, making it a less compelling candidate for a positive surprise ahead of its August 4 release.

Kyndryl Holdings (KD) is approaching its quarterly earnings report with a mixed but cautious outlook. Consensus estimates project substantial year-over-year growth, with earnings per share (EPS) expected to rise 184.6% to $0.37 and revenue to increase 1.6% to $3.8 billion. However, this positive long-term growth narrative is tempered by recent negative revisions from covering analysts. Over the past 30 days, the consensus EPS estimate has been revised downward by a notable 8.57%. This bearish short-term sentiment is further quantified by a negative Zacks Earnings ESP (Expected Surprise Prediction) of -4.05%, which indicates that the most recent analyst estimates are below the consensus, reducing the statistical likelihood of an earnings beat. While the company has a history of surpassing EPS estimates in three of the last four quarters, the current combination of a neutral Zacks Rank #3 (Hold) and a negative ESP makes it difficult to predict a positive surprise for its upcoming August 4th release.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15

Ticker Sentiment