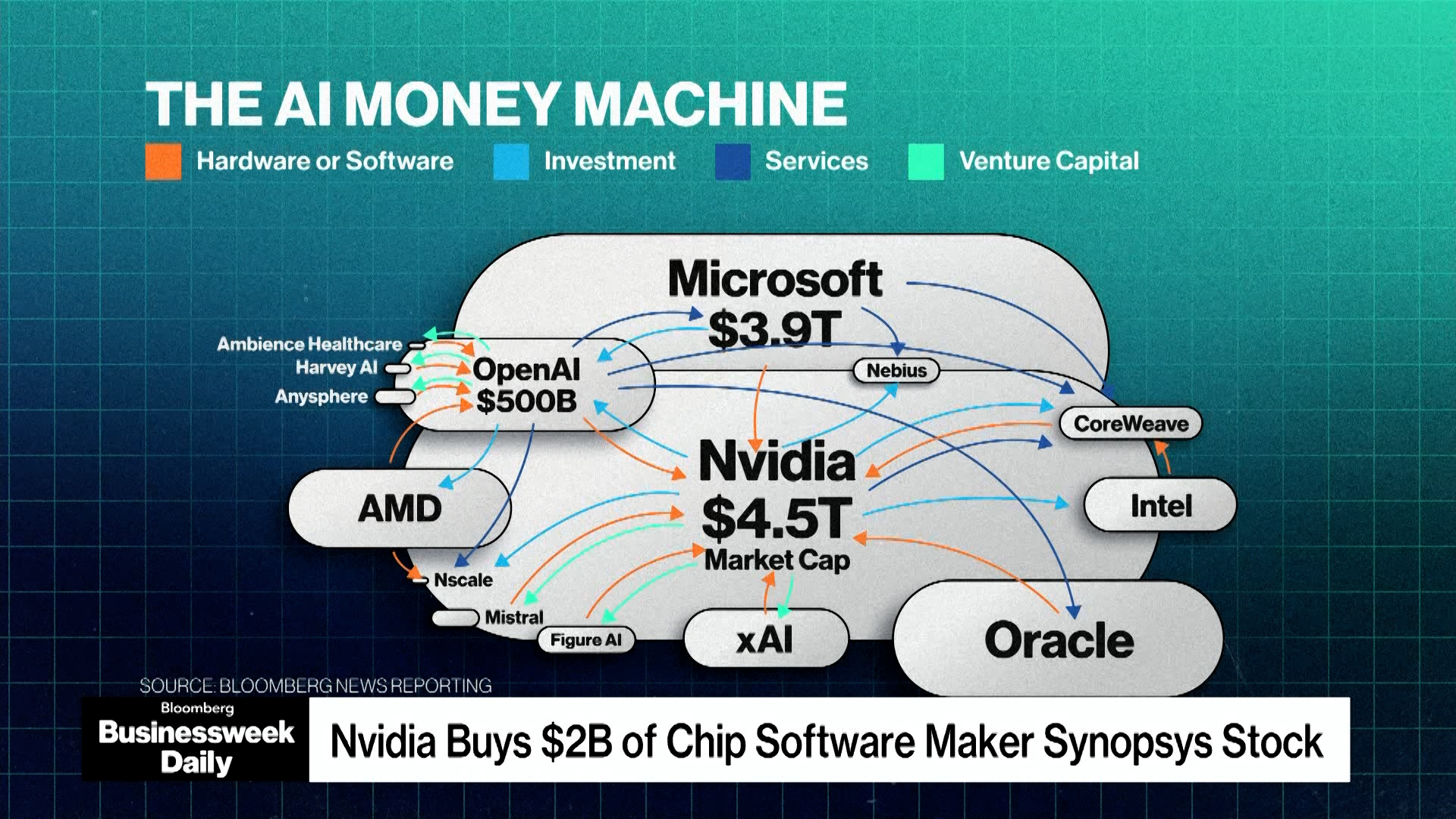

Nvidia made roughly a $2 billion strategic equity investment to acquire about a 2–3% stake in Synopsys at $414.79 per share (the stock trading near ~$440), which CEO Jensen Huang frames as both a financial investment and an engineering partnership to accelerate running EDA software on GPUs without exclusivity constraints. The story signals continued industry consolidation around AI-accelerated chip design tools and underscores investor positioning — exemplified by Masayoshi Son selling Nvidia stock to fund other AI bets — while competing open-source efforts (a Chinese ‘Deep Sea’ model v3.2/3.2 XP using mixture-of-experts) claim GPT-5-comparable performance through parameter-efficiency, raising stakes on cost and deployment efficiency in generative AI.

Market structure: Nvidia’s minority stake in Synopsys (and similar strategic equity moves) increases Nvidia’s optionality as a distribution and software-acceleration platform — winners are NVDA (higher software stickiness, incremental GPU demand) and EDA vendors that embrace GPU-accelerated toolchains (Synopsys/SNPS). Losers could include legacy CPU incumbents (INTC) and EDA vendors that resist integration; expect 6–24 month share gains for GPU-optimized toolchains if adoption accelerates to even 10–20% of large-node tapeouts. Risk assessment: Tail risks include regulatory/antitrust scrutiny of cross-ownership, customer walkaways from perceived lock‑in, or a tech pivot where MOE/efficient LLMs materially reduce dense-GPU inference demand. Immediate (days) risk: headline-driven volatility; short-term (weeks–months): re-rating around guidance/partner commentary; long-term (quarters–years): structural shift in chip-design workflows and hardware mix. Hidden dependency: Synopsys’s enterprise contracts and multi-vendor integrations — a 10% decline in third‑party OEM deals would be material. Trade implications: Direct play: overweight NVDA via equity or 3–9 month call spreads to capture integration narrative; relative value: long NVDA vs short INTC to express AI compute share shift (target 15–30% outperformance over 6–12 months). Options: buy 3–6 month call spreads (10%–20% OTM) funded by selling 30%+ OTM calls to limit premium outlay; use 0.5–1.5% portfolio risk sizing for directional exposure. Sector rotation: increase weight in AI software/EDA (SNPS) and GPU supply chain, trim traditional x86 data-center hardware exposure (INTC) over next 12 months. Contrarian angles: Consensus assumes stake equals exclusive commercial capture — that is likely overstated and could provoke pushback from customers/regulators, so upside may be capped if Synopsys reassures multi‑vendor support. Conversely, markets underprice the compounding effect if GPU-acceleration becomes default in EDA; historical parallels: Intel’s earlier platform plays created multi-year incumbency but also regulatory heat. Watch for unintended consequence: customers shifting to alternative EDA vendors to avoid perceived lock-in, creating a bifurcated market rather than full consolidation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment