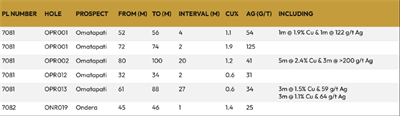

Oscillate PLC (Serval Resources) has entered a conditional agreement to acquire Kalahari Copper Limited, gaining 100% interests (subject to licence renewals/transfers) in four Namibian tenements (c.789 km2) and 17 Botswana tenements (c.1,453 km2) that include >9,000m of historic drilling with Cu-Ag intersections. Consideration includes £2.0m cash (deferrable/convertible), 30% of issued shares on AIM (subject to a minimum £5.0m fundraising), up to £9.0m of country-specific milestones, a 1.9% NSR, and options totalling up to 6% of share capital; completion is conditional on licence/consent approvals and successful AIM admission. Board and senior appointments accompany the deal (seller to nominate a NED; Richard James appointed CFO), positioning the company for an AIM move and to capitalise on copper demand tied to the energy transition.

Market Structure — Winners are junior copper explorers and AIM-listed resource plays (direct beneficiary: AQSE:SRVL on successful Admission) and investors seeking early-stage discovery optionality; losers are incumbent explorers/developers with less new-prospect exposure. This deal does not change near-term physical copper supply (projects are pre-resource), but it signals increased capital flow into Kalahari/Kaoko belts which can compress risk premia for African copper juniors over 6–24 months. Cross-assets: modest positive for copper futures and miners ETFs (COPX) on sentiment; GBP funding risk vs AUD/USD miners could widen basis spreads briefly around Admission. Risk Assessment — Highest tail risks: failure to raise ≥£5.0m, refusal of Takeover Panel waiver, or non-renewal of EPL licences (deadlines by 6 Mar 2026) which would materially dilute equity value; each has >10% probability and would likely cut valuation >50%. Immediate (days): AIM Admission and Fundraise; Short (weeks–6 months): licence renewals, first drilling assays; Long (12–36 months): Maiden JORC → PFS → FID which trigger up to £9m in milestones. Hidden dependency: seller retains 30%+ options and convertibility rights (anti-dilution/30‑day VWAP mechanics), creating multi-year downward price pressure and governance risk. Trade Implications — Direct: conditional, tactical long (2–3% portfolio) in SRVL only after (a) AIM Admission confirmed, (b) Fundraise ≥£5m cleared, and (c) evidence of licence transfers; use a strict stop at −35% and take-profit at +50–100% or on Maiden JORC. Pair trade: long SRVL / short SFR.AX (Sandfire) 1:0.5 to isolate discovery vs copper-price exposure during next 6–12 months. Options: buy 6–12 month call spreads on COPX (size 0.5–1% notional) to capture copper upside without single‑name governance risk. Contrarian Angles — Consensus underestimates seller governance and dilution: 30% Consideration Shares + 6% options + anti-dilution rights mean effective free‑float may be small post‑Admission, so post-listing sell pressure is likely after lock-up expiries (12 months). Historical parallels: many African junior consolidations re‑rate on initial news but fade on licence/regulatory setbacks; therefore value may be front‑loaded and fragile. Watch for contingent payments (EPL 7081 / Sandfire fee) that could entangle future asset sales and restrict management optionality.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment