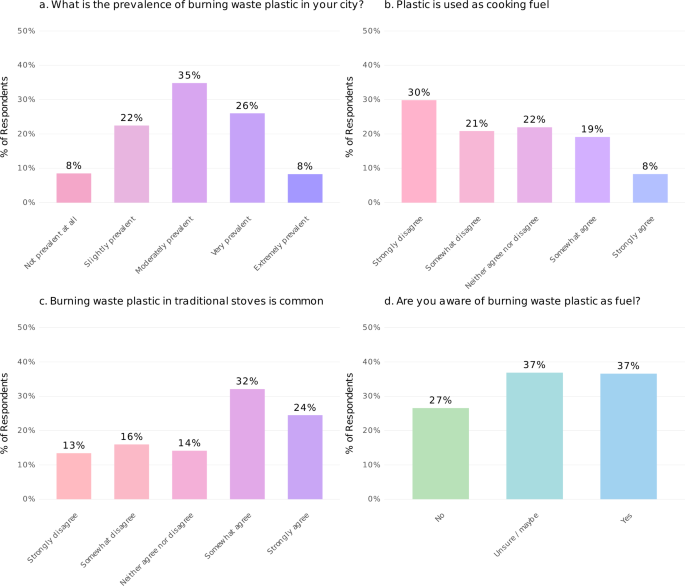

A cross-sectional survey of 1,018 key informants across 26 Global South countries finds widespread integration of plastic waste into household energy practices: 37% of respondents were aware of household plastic burning, 16% reported having burned plastic themselves, and sizable shares reported it as common in traditional stoves (32% somewhat agree, 24% strongly agree). Regression results link plastic burning to supply-side factors (city-level plastic waste volumes, p≤0.023; populations without waste collection, p<0.001) and demand-side drivers (perceived high cost of clean fuels, p<0.004), highlighting a combined waste-management and energy-affordability problem; respondents ranked expanded solid waste collection and improved access to clean cooking as top solutions. For investors, the findings underline elevated ESG, public-health and regulatory risks in rapidly urbanizing emerging markets and point to potential demand for investments in urban waste infrastructure, low-cost clean cooking solutions, and firms positioned to address municipal waste-management gaps.

Market structure: The primary beneficiaries are large municipal/infrastructure operators and waste‑to‑energy contractors (e.g., Veolia VEOEY, SUEZ/SEV.PA, BFF.L) and clean‑fuel distributors (IGL.NS, MGL.NS) because rising mismanaged plastic creates pressure for contracted collection and subsidized clean fuels. Losers include single‑use plastic packagers (AMCR, other polymer producers) and informal waste‑dependent value chains; expect pricing power to shift toward integrated contractors as cities outsource collection and pay for capex-heavy solutions. On assets, rising municipal capex should tighten EM municipal bond spreads (benefit for green bond ETFs) and lift LPG/propane physical markets; EM FX may strengthen where donor financing and green bond issuance accelerate. Risk assessment: Tail risks include abrupt regulatory plastic bans or litigation (national bans within 3–12 months), donor funding reversals, or political backlash that suspends municipal contracts—each could wipe out >20% of forward EBITDA for operators in affected cities. Time horizons: immediate (days–weeks) for headlines and WHO/UN reports that move sentiment; short (3–12 months) for green bond windows and pilot programs; long (1–4 years) for order‑book realization and plant commissioning. Hidden dependencies: project economics hinge on municipal fee collection rates and currency stability; monitor donor/DFI commitments and local tax receipts as gating variables. trade implications: Direct plays — establish a 2–3% portfolio long in Veolia (VEOEY) with 12–24 month horizon to capture contract wins; add 1–2% long in Indian LPG distributors IGL.NS/MGL.NS as domestic clean‑fuel uptake catalysts over 6–18 months. Fixed income — allocate 2–4% to green bond ETFs (BGRN, GRNB) and 1–2% to EM local bond ETF (EMLC) to capture municipal financing flows; Pair trade — long VEOEY vs short AMCR (notional ~15% of the VEOEY leg) to play regulatory pressure on packaging. Options — buy 9–12 month VEOEY call spreads (20% OTM) size 0.5–1% to lever upside while limiting premium. contrarian angles: Consensus underestimates operational difficulty of delivering collection in dense informal settlements — early contract announcements often disappoint, creating idiosyncratic risk and potential rewrites of orderbooks (watch for >€500m new contract threshold). The market may be underpricing health‑liability externalities: if indoor burning rises after outdoor bans, expect accelerated public funding (positive shock to contractors) rather than permanent demand loss for them. Historical parallel: water/Waste PPP cycles where political risk produced multi‑year value traps — prioritize counterparties with municipal fee collection KPIs and DFI co‑financing to avoid moral‑hazard losses.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25