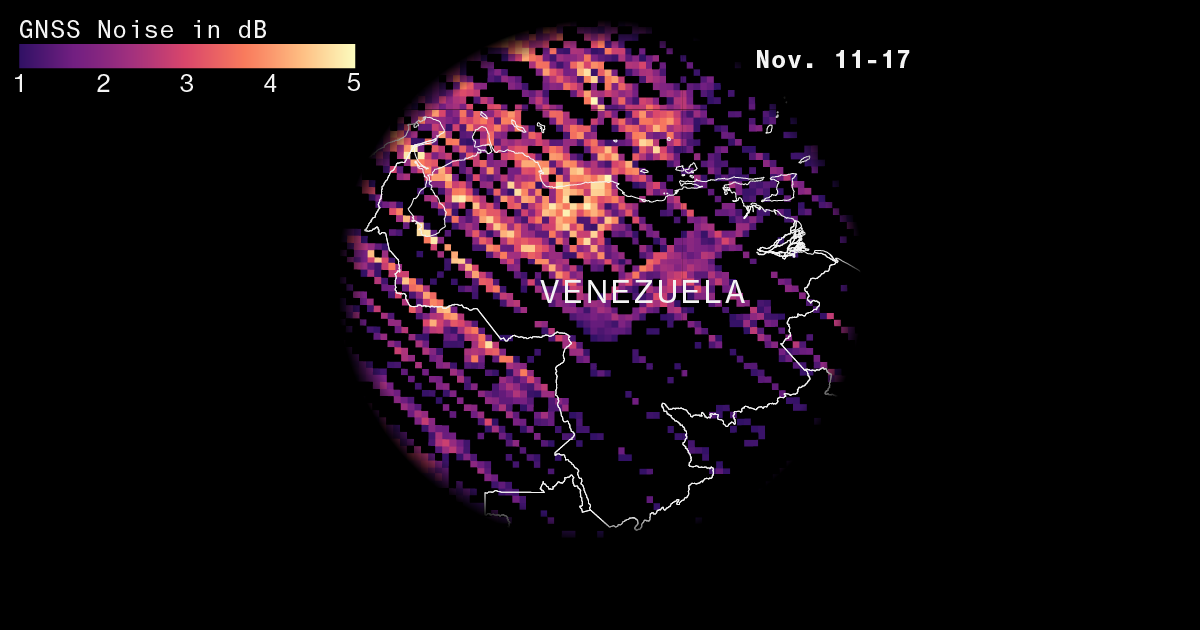

Electromagnetic interference attributed to heightened U.S. and Venezuelan military activity has degraded GNSS/GPS signals over Venezuela and the Caribbean, prompting a Nov. 20 FAA warning and the suspension of international carriers including Avianca, Iberia and Gol. Satellite and aviation monitoring firms (CYGNSS, Spire) show a measurable rise in interference in recent months — Spire data indicated more than 10% of regional air traffic reported navigation integrity degradation prior to the FAA advisory — raising operational risks for airlines, LEO satellite constellations (Starlink, OneWeb) and navigation-reliant infrastructure while local carriers continue service under government pressure.

Market structure: Immediate winners are satellite-data and GNSS-resilience vendors (SPIR) and defense/ECM suppliers (LHX, RTX, NOC) as demand for monitoring, ADS‑B augmentation and anti‑jamming rises; losers are regional carriers and travel/reliability‑sensitive logistics providers (GOL, carriers with Venezuela routes, airline ETF JETS) facing route cancellations and higher ops costs. Pricing power shifts to niche telemetry/data providers and avionics retrofit vendors because >70% of global commercial receivers are legacy L1‑only and upgrades to L5 are multi‑year, creating an inelastic short‑term supply of resilience tech. Risk assessment: Short horizon (days–weeks) sees flight diversions, revenue loss and volatility in regional airline equity; medium (3–12 months) brings contract awards and higher defense capex if FAA warnings persist >2–4 weeks; long term (1–3 years) structural uplift to avionics retrofit and EW budgets. Tail risks include escalation to broader maritime conflict creating commodity/insurance shocks; hidden dependencies include fintech, power and LEO‑sat constellations (Starlink/OneWeb) that rely on GNSS timing — sustained >4‑week jamming could force expensive operational workarounds. Trade implications: Direct tactical: buy SPIR (data/ADS‑B) and selective exposure to LHX/RTX for EW upside; short targeted airline exposure (JETS, GOL) or buy puts on carriers with >5% revenue exposure to Venezuela routes. Options: 3–12 month calls on LHX or SPIR for asymmetric upside; buy 1–3 month puts on JETS to express immediate disruption. Entry triggers: FAA extension of advisory, Spire/FlightAware ADS‑B degradation >12% sustained 2 weeks, or public naval deployments. Contrarian view: Consensus underprices recurring recurring revenue from GNSS‑monitoring (data monetization + SaaS) — SPIR can monetize telemetry quickly and scale at low incremental cost, implying 20–40% upside in 6–12 months if contracts accelerate. Overreaction risk: broad shorts of major global airlines (IAG) are likely overdone because few have material Venezuela exposure; historical parallel: Ukraine jamming increased EW vendor orderbooks for 12–24 months, not permanent collapse of commercial air traffic.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

Ticker Sentiment