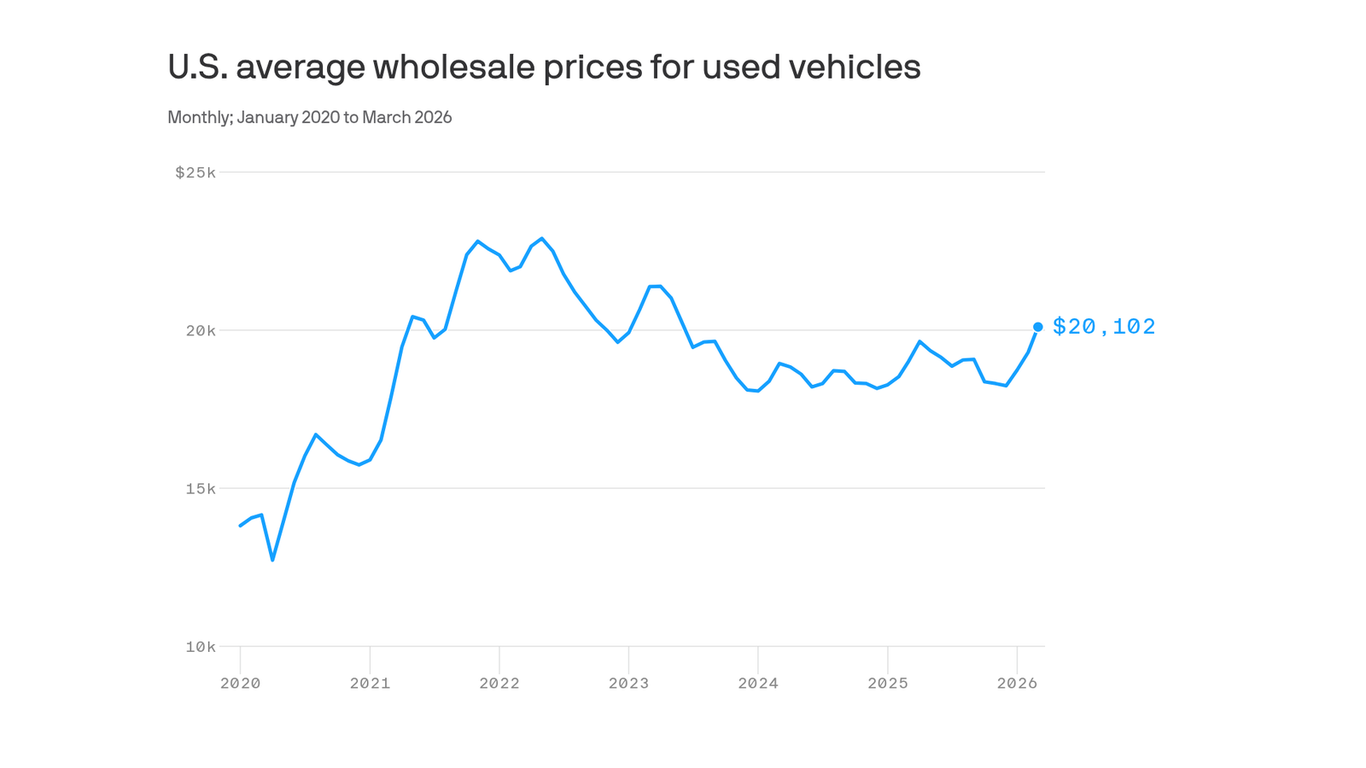

Manheim's Used Vehicle Value Index rose 6.2% year-over-year in March and 1.4% month-over-month, with the non-seasonally adjusted average wholesale price at $20,102 and average list prices above $25,000. Dealer inventory tightened to a 40-day supply, supporting firm retail pricing despite affordability constraints; wholesale prices remain below the May 2022 record of $22,902. Cox cites higher-than-average tax refunds as a demand booster and flags potential market effects from the Middle East conflict and rising energy prices.

Dealer economics are the immediate, underpriced lever here — structurally tighter wholesale supply and firm retail pricing translate into higher gross margins per unit for franchised and independent dealer groups, which convert into FCF through lower inventory carrying losses and faster turns. Expect acceleration in dealer M&A and buybacks over the next 3–12 months as balance-sheet flexibility improves, even if overall unit demand remains flat; that amplifies equity upside for well-capitalized groups relative to smaller competitors with higher cost-of-capital. Credit and securitization are the hidden hinge: elevated used values reduce LTVs across recent originations and cushion ABS pools, compressing expected loss rates near-term, but rising interest rates and the transitory nature of the tax-refund bump create a fast path to stress if retail demand fades. Watch IRS timing and monthly payroll trends over the next 2–3 months as the most actionable short-term trigger for demand normalization; conversely, a semiconductor-driven surge in new-car availability would mechanically depress used pricing on a 6–12 month lag. Energy/geopolitics provide an asymmetrical risk: a sustained crude spike (>+$10/bbl) in 0–3 months will disproportionately rerate demand toward higher‑MPG used cars and accelerate depreciation of large trucks/SUVs, boosting parts & aftermarket spend but compressing residuals on heavy vehicles. Separately, limited used-EV supply supports residuals relative to ICE peers — a bifurcation that will widen valuation dispersion across dealer inventories and insurer loss models over the next 6–18 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.20