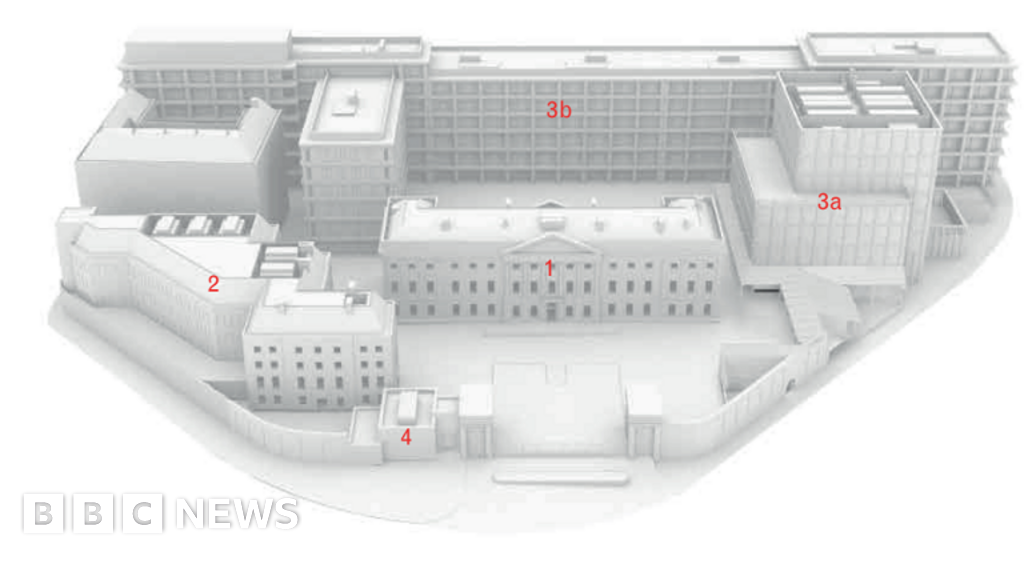

UK ministers have pushed back to 20 January a planning decision on a proposed Chinese 'mega' embassy at Royal Mint Court that would consolidate seven diplomatic sites into a single complex with capacity for about 200 staff and substantial basement space close to key fibre‑optic cables. Government officials contend consolidation could yield security advantages and say national security issues have been addressed after redacted blueprints and scrutiny, but MI5 warnings, opposition criticism and espionage concerns keep security uncertainty high, with potential implications for UK‑China political and cyber risk exposure.

Market structure: Consolidating seven diplomatic sites into one London mega‑embassy shifts demand into a concentrated security envelope; winners are cybersecurity/defense contractors and secure construction/infrastructure firms (higher near‑term revenue for vetting, screening, hardened builds). Losers are central‑London office landlords and boutique services that rely on unconstrained access — expect London office REIT implied spreads to widen 20–50bp versus gilts if political scrutiny persists, and headline risk to move GBP ±0.5–1% around the Jan‑20 decision. Risk assessment: Tail risks include diplomatic escalation or targeted cyber retaliation (probability <10% but systemic impact), and regulatory tightening forcing retrofits or restricted access near fibre routes (multi‑quarter CAPEX shock). Immediate catalyst window is the Jan‑20 planning decision and any MI5 closed‑door findings (days–weeks); medium term (3–12 months) depends on policy outcomes that could reprice UK office real estate and telecom/operators exposed to fibre‑adjacency rules. Trade implications: Tactical allocation should overweight cyber/defense and underweight central London office REITs. Expect a 5–15% re‑rating potential for cyber names on renewed government procurement and a 10–25% downside scenario for poorly located office landlords if leasing volumes decline. Use 1–3 month directional options around the Jan decision to cap downside and harvest headline‑driven volatility. Contrarian angles: Consensus focuses on espionage risk, but consolidation may lower cumulative attack surface and lead to clearer security liabilities (a net positive for insurers and compliant developers). Small‑cap UK cyber/security names (e.g., DARK.L, NCC.L) and data‑center REITs (EQIX, DLR) could be underappreciated beneficiaries over 6–12 months if policy favors onshoring and certificated secure facilities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.30