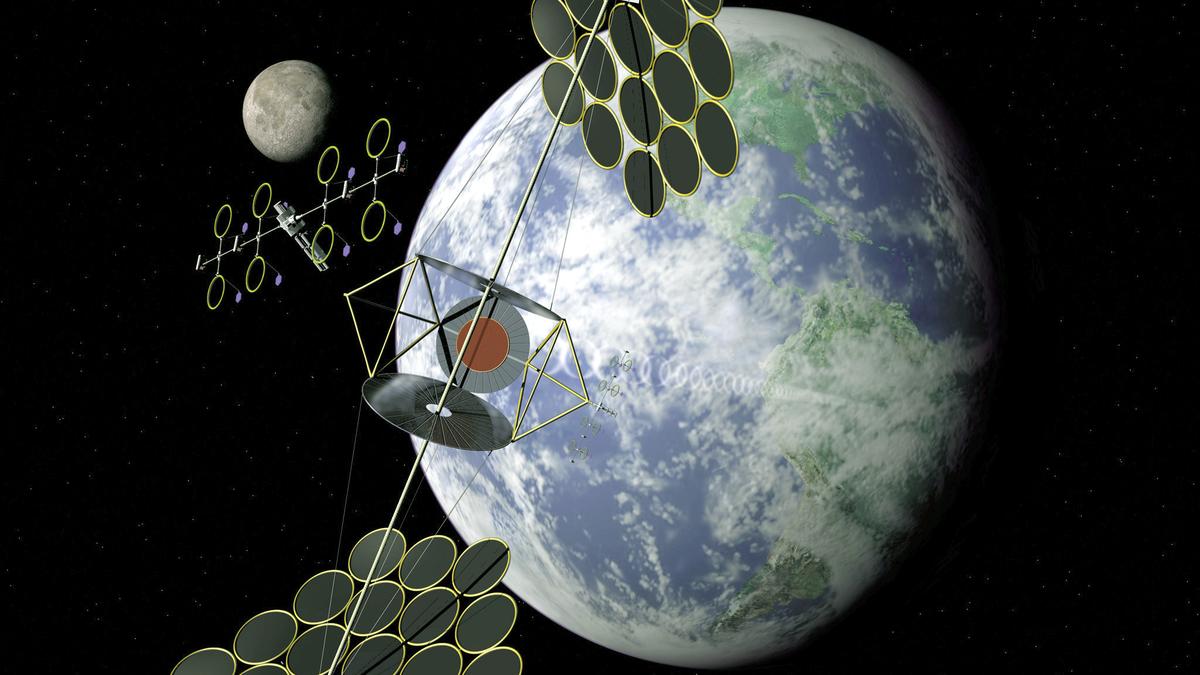

Shimizu Corporation proposed an 11,000 km “Lunar Ring” of lunar-surface power plants to collect solar energy and beam it to Earth as microwaves. The article flags major economic and engineering hurdles — transporting “thousands of tonnes” to the Moon, large atmospheric transmission losses, collision risk with space debris, and high maintenance costs — and notes terrestrial solar plus battery storage is becoming cheaper, leaving space-based solar economically unviable for now.

Space-based or lunar baseload concepts will only move from science-fiction to investable when three independent cost curves bend simultaneously: heavy‑lift marginal launch cost, in‑situ resource/utilization (ISRU) cost per tonne delivered on the moon, and wireless power transmission end‑to‑end efficiency. Today those remain staggered across decades; economically rational capital allocators will demand demonstrable pathways to sub‑$50/MWh delivered (or other parity metrics) before allocating meaningful balance‑sheet capital, which implies multidecade deployment timelines and very high discount rates for any developer. Second‑order winners are therefore the incumbents that close the margin between grid need and terrestrial supply: large-scale storage integrators, utility developers that can aggregate distributed solar, and RF/microwave component specialists that could commercialize power‑beaming for niche terrestrial or defense applications. Losers are the speculative small caps that price in rapid space‑infrastructure monetization and insurers/reinsurers exposed to low‑frequency/high‑severity orbital debris risk; the insurance cost curve for orbital assets is likely to remain a non‑linear tax on scale. Catalysts that would reset the landscape are binary but identifiable: a credible ISRU demo (12–36 months), an order‑of‑magnitude step‑down in $/kg to LEO/Trans‑Lunar injection (18–48 months after technology maturation), or a sovereign strategic program with multi‑year guarantees. Tail risks include Kessler‑type debris cascades or regulatory bans on high‑power downlinks — each could destroy the business case overnight. The realistic path is incremental: niche military/remote‑grid pilots first, commercial ambition later, so position sizing should reflect optionality rather than conviction.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30