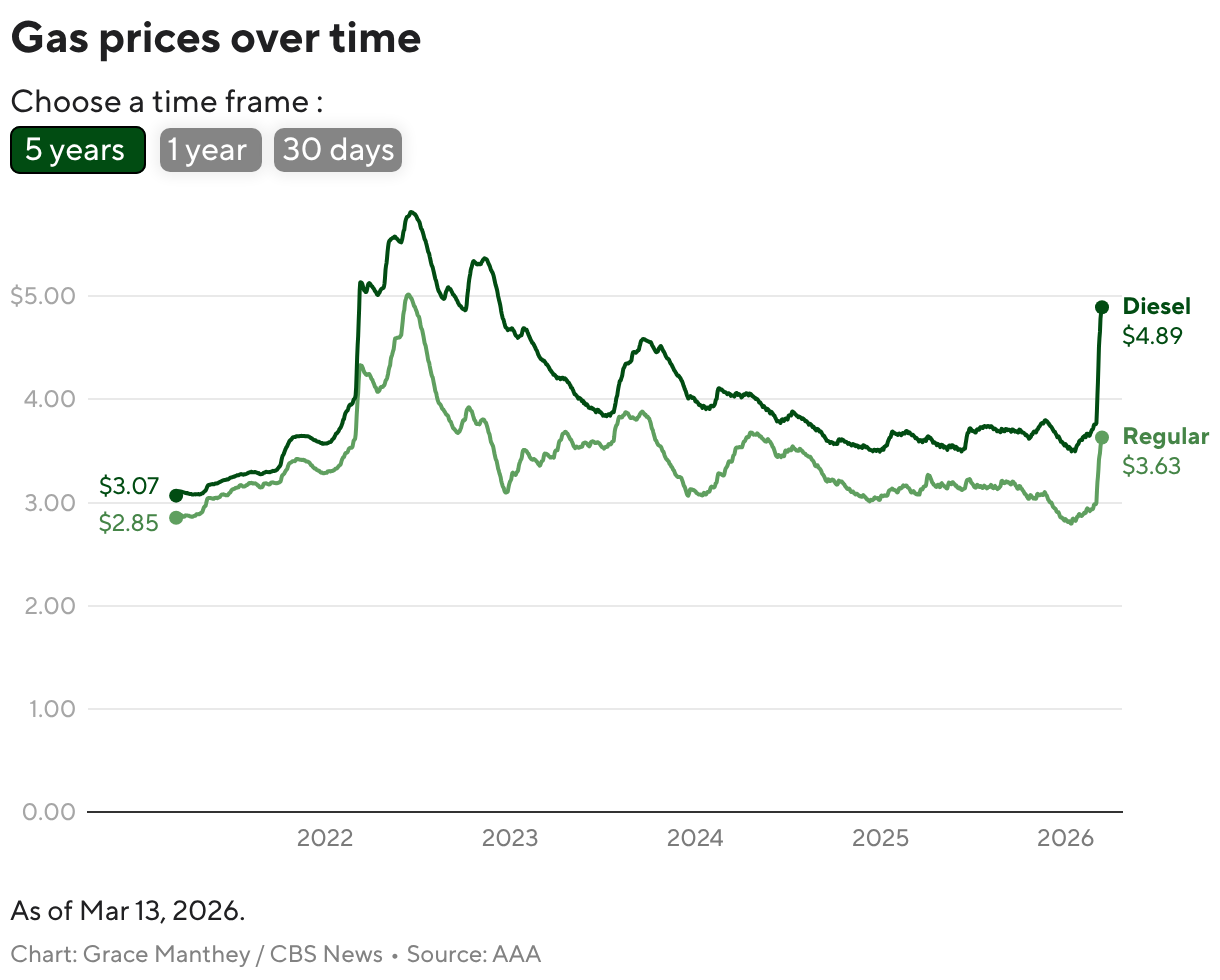

Brent crude hit $111.45/barrel and U.S. benchmark crude rose to $99.24, driving the U.S. average gasoline price to $3.84/gal from $2.92 a month ago (≈+$0.92, +31.5%), the highest since Sept 2023. Diesel topped $5/gal nationally and exceeds $6/gal in California, Hawaii and Washington. The rally is attributed to Middle East supply risks—Iranian threats to regional infrastructure and Strait of Hormuz shipping disruptions—and the White House issued a 60-day Jones Act waiver that analysts call a temporary, limited relief measure.

The current price move is being driven by a supply-side shock transmitted through chokepoints, insurance premia and refinery/transport frictions rather than a pure change in long‑run demand. That amplifies regional crack spreads: refiners with export access and spare blending capacity can convert a shipping squeeze into outsized margins for middle distillates, while end‑users who cannot reroute (regional consumers, short‑haul trucking, intrastate markets) face sharper price pressure and passthrough. Second‑order winners include owners of tonnage and storage capacity — higher voyage rates and a steeper prompt curve lift tanker equity cashflows and create arbitrage opportunities for crude/diesel flows around capacity bottlenecks; losers include freight‑intensive industrials, airlines and domestic hauliers where fuel is a large variable cost and fuel surcharges lag. The temporary domestic regulatory relief on coastal shipping eases logistics frictions but does little for global risk premia or insurance costs, so expect only modest, localized relief. Key near‑term catalysts are binary and fast: further attacks or credible threats that materially impede Gulf throughput would tighten prompt markets within days; diplomatic de‑escalation, coordinated strategic releases, or a rapid capacity response from major producers would unwind risk premia over weeks. Watch leading indicators — tanker time‑charter rates, Singapore diesel cracks, maritime war‑risk premiums and US refinery utilization — for signal timing of mean reversion versus sustained structural tightening over the next 1–6 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.35