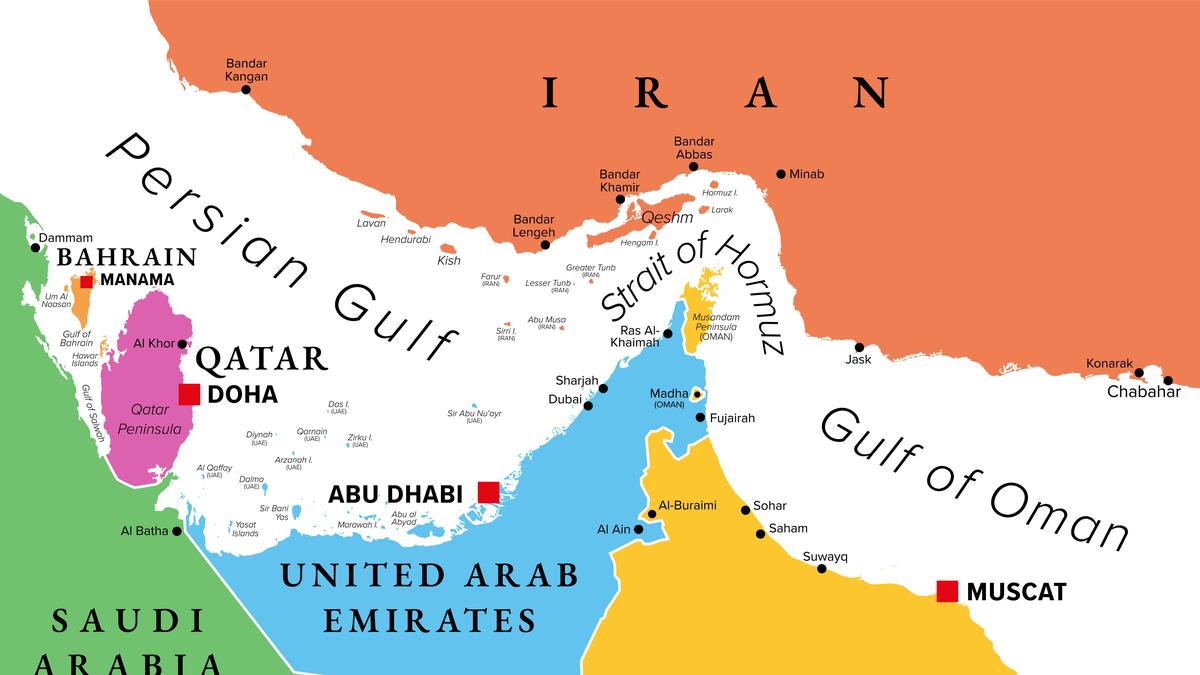

China called for a lasting truce in West Asia and for shipping lanes to reopen as soon as possible, underscoring the market significance of the Strait of Hormuz closure. The strait normally carries roughly 20% of global oil and LNG shipments, and Iran has largely blocked traffic since fighting began on February 28, creating a major supply-risk shock. China also said it hoped a ceasefire could be reached soon, while Iran said it allowed some Chinese ships to pass through the waterway.

The market is likely underpricing how quickly a partial reopening of Hormuz can unwind the entire risk premium stack, not just crude. The first-order move is obvious in front-month energy, but the bigger second-order effect is a rapid normalization in freight, insurance, and working-capital terms for Asian importers that had been forced into longer haul/alternative routing. That matters because the beneficiaries are not only commodity consumers; lower delivered-input costs can expand margins for chemicals, airlines, refiners, and selected industrials within days, while commodity-exporting balance sheets face a valuation de-rating over months. China’s public positioning is more important than the diplomacy theater suggests. If Beijing is signaling a preference for open shipping and no military aid to Tehran, it is implicitly protecting its own energy-security corridor and preserving the option value of discounted Iranian barrels later, rather than maximizing Tehran’s leverage now. That creates a ceiling on how long the disruption can stay extreme: once the main outside patron wants de-escalation, the market should expect a quicker-than-expected shift from supply shock pricing to surplus/normalization pricing, especially if even limited transits resume. The main tail risk is a short-lived but violent re-escalation that closes the strait again or broadens attacks to offshore terminals and tanker assets, which would create a 1-3 week spike in vol even if the structural outcome is a truce. The base case, however, is that risk assets overreact on the upside in energy and then fade as shipping data confirm incremental reopenings over the next 1-4 weeks. Contrarianly, the best fade may be through the underowned consumers with direct feed-through to margins, because the market tends to focus on headline oil and ignore the compounding benefit of lower logistics friction and improved inventory turns.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.45