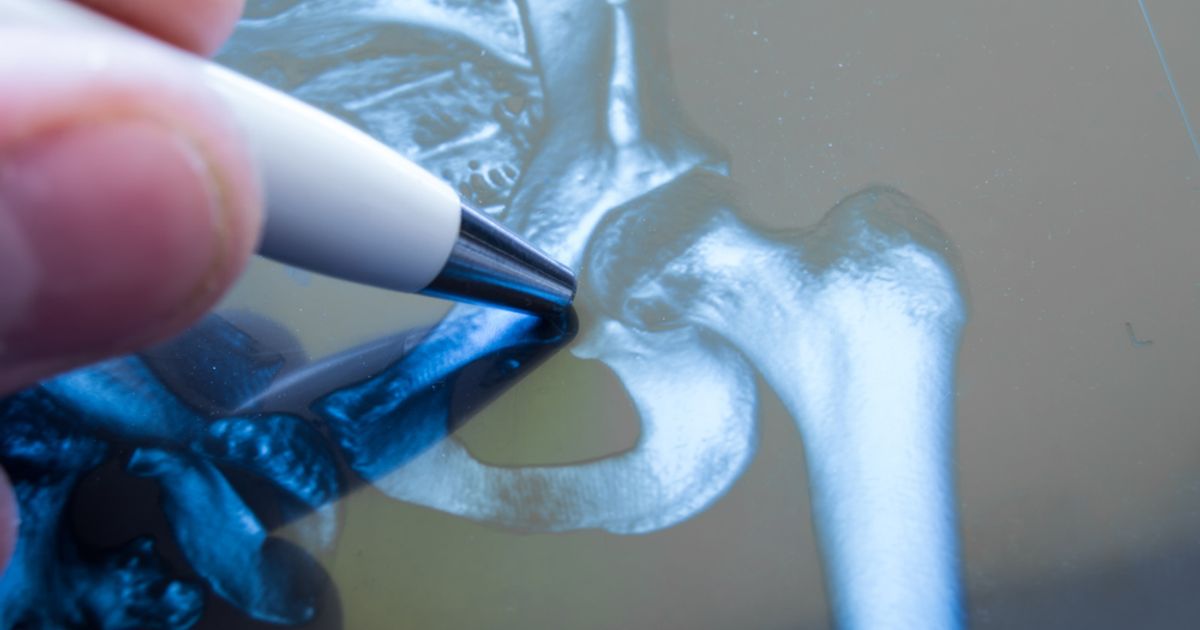

Smith & Nephew unveiled a new RISE strategy and set 2028 targets of 6–7% CAGR revenue, 9–10% trading profit growth and over $1bn in free cash flow, while tightening 2025 guidance to ~5.8% underlying revenue growth, trading profit margin of at least 19.5% and raising 2025 free cash flow guidance to ~$800m. The company flagged a one-off non‑cash provision of ~ $200m in 2025 to support portfolio rationalisation (aimed at reducing gross inventory by ~$500m) and expects ~6% underlying revenue growth and another ~$800m free cash flow in 2026; Capital Markets Day events on Dec 8/11 will present further detail.

Market structure: Smith & Nephew (SNN) strengthening margins and guiding $800m FCF in 2025 with 6–7% revenue CAGR to 2028 shifts payoff to cash-generative med‑tech names. Winners: SNN, suppliers with scale and high-margin implant franchises; losers: smaller pure‑play orthopaedics and regional distributors facing inventory rationalisation and one‑off charges. Currency exposure matters — guidance is “based on current exchange rates”, so a sustained USD/GBP move >3% will materially swing reported growth. Risk assessment: Tail risks include execution failure on portfolio rationalisation (inventory write‑downs >$200m), regulatory setbacks on implants, or a cyclical slowdown in elective surgeries that could erase margin gains. Immediate risk window is the Capital Markets Days (Dec 8/11) and 30‑90 days post‑presentation for management detail; medium term (6–18 months) centres on inventory reduction delivery and FCF conversion; long term is delivery against 2028 targets. Hidden dependency: margin targets assume reinvestment and M&A discipline — aggressive bolt‑ons could dilute returns. Trade implications: Tactical long SNN exposure for 6–12 months to capture margin upside and cash conversion, sized 1–3% of portfolio; use call spreads to finance upside if IV is rich. Consider a relative play long SNN vs short ZBH/SYK if you believe SNN’s inventory-led gross margin recovery will outpace peers. Fixed income: tighten credit view — SNN bonds should benefit if FCF >$800m is sustained; monitor CDS tightening >10bp as a buy signal. Contrarian angles: Consensus may underprice execution risk of rationalisation and overprice structural improvement; the $200m non‑cash charge signals potential legacy product or obsolescence issues that can recur. If inventory reduction is achieved too fast it could tighten supply and depress near‑term revenue, creating a 3–6 month sell‑the‑news opportunity. Historical parallel: prior multi‑year turnaround plans in med‑tech often took 12–24 months to fully translate into EPS, so patience and tranche sizing matter.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment