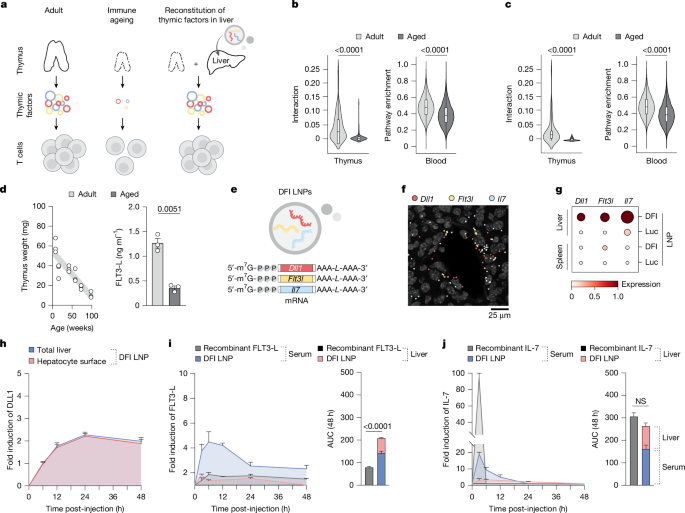

In aged mice, hepatic delivery via SM‑102 LNPs of mRNAs encoding DLL1, FLT3L and IL‑7 (DFI) transiently reconstituted thymic-supporting signals, expanded common lymphoid progenitors, increased circulating naïve CD4+/CD8+ T cells and cDC1s, and materially improved antigen-specific CD8+ vaccine responses and antitumour immunity (including ~40% complete rejection in a B16‑OVA model). Effects were reversible after dosing, showed minimal liver toxicity compared with recombinant cytokines, and investigators have filed a provisional patent, indicating a promising but early-stage mRNA-based immunorestorative platform with potential translational and commercial value contingent on human safety and efficacy data.

Market structure: The paper accelerates demand signals for mRNA-LNP manufacturing, modified nucleotides and high-throughput immune monitoring — beneficiaries include platform manufacturers and diagnostics infrastructure (expect incremental revenue tail of $100M–$500M across several leaders within 2–4 years if human translation is positive). It simultaneously threatens the recurring-revenue model of high-dose recombinant cytokine therapeutics and may compress pricing for episodic protein biologics as mRNA enables lower-frequency, hepatic factories. Expect tight supply for proprietary ionizable lipids and GMP-modified nucleotides in the next 6–12 months, lifting suppliers’ pricing power unless capacity expands quickly. Risk assessment: High-impact tail risks include translational failure in humans, emergent autoimmunity or liver toxicity that triggers FDA hold or label restrictions — a single Phase 1 adverse event could cut valuations of small platform suppliers by >30% within weeks. Near-term (0–3 months) newsflow will be preclinical-to-clinical transitions and IP filings; mid-term (3–18 months) are INDs/first-in-human data; long-term (1–4 years) are commercialization, reimbursement and chronic-dosing safety readouts. Hidden dependencies: reliance on specific lipids (SM-102/alternatives), cold-chain and repeat dosing economics; watch patent landscape and freedom-to-operate litigation as immediate catalysts. Trade implications: Tactical exposure to immunosequencing and oligo/LNP suppliers is highest-conviction (durable secular demand if translated). Favor long, option-defined exposure to diagnostic/seq names and large-cap pharma with mRNA scale (to capture partnerships) while avoiding binary small-cap therapeutics that monetize recombinant cytokines. Volatility should spike around IND and Phase 1 readouts — use defined-risk options to limit tail losses. Contrarian angles: The market underestimates requirement for repeated dosing and payer resistance — a one-year repeat regimen versus a single vaccine changes TAM dramatically and limits valuations; historical parallel is the 2020 mRNA exuberance then selective consolidation. Reaction is likely underdone for infrastructure suppliers (sequencing, oligo, LNP contract manufacturers) and overdone for speculative small cytokine pure-plays; unintended consequences (autoimmunity signals, regulatory tightening) could rapidly invert winners into losers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment