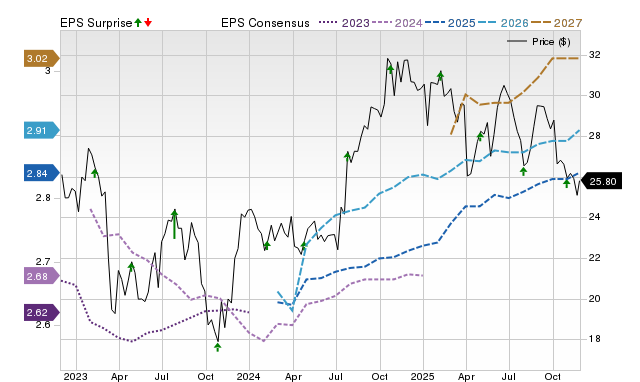

Cousins Properties (CUZ) closed the last session at $25.80 while the mean Wall Street price target of $32.33 implies a 25.3% upside; the 12 analyst targets range from $27.00 to $35.00 with a standard deviation of $2.46 (implied upside range +4.7% to +35.7%). Analysts have revised two current-year EPS estimates higher in the last 30 days and the Zacks Consensus Estimate rose 0.4%, with CUZ holding a Zacks Rank #2 (Buy), but the piece cautions that price targets can be biased and should be treated with skepticism despite the favorable near-term signals from estimate revisions.

Market structure: CUZ is trading at $25.80 vs a mean analyst PT of $32.33 (+25.3%) with 12 covers and SD $2.46, signalling concentrated optimism but limited market-impact (market score 0.25). Direct beneficiaries would be select value-add office REITs and landlords in Sunbelt growth corridors if fundamentals (leasing spreads, occupancy) reaccelerate; losers are gateway CBD office landlords and highly levered peers if capital markets tighten. Cross-asset: a meaningful re-rating of CUZ would be rate-sensitive — positive for equities if driven by fundamentals, negative if driven by spread compression versus USTs; expect options IV to compress after positive earnings and bond yields to dictate 6–12 month returns. Risk assessment: Near-term (days–weeks) moves are analyst- and earnings-driven; short-term (3–6 months) depends on leasing prints and same-store NOI; long-term (12+ months) depends on tenant demand and refinancing maturities. Tail risks include a >100bp rapid rise in 2-year yields, a large tenant default on key assets, or a refinancing cliff on covenanted debt. Hidden dependencies: CUZ’s upside is contingent on access to low-cost capital and execution on leasing/development pipelines; small +0.4% EPS revisions to date are fragile and can reverse quickly. Key catalysts: quarterly earnings, major leasing announcements, and the next Fed rate decision. Trade implications: Tactical direct play: consider establishing a 2% long position in CUZ common stock sized to portfolio risk on a conviction of 20–35% upside over 3–12 months, with primary targets $32 and $35 and stop-loss at $22 (≈15% downside). Options: implement a 3–6 month bull-call spread (buy CUZ 6m $26 call, sell $34 call) sized equivalently to 2% capital to cap premium and capture upside to ~+30%. Relative trade: long CUZ (2%) vs short VNQ (1%) to express idiosyncratic outperformance while partially hedging sector/rate beta. Reduce exposure to gateway CBD office names (e.g., SLG, VNO) by 25–50% in favor of higher-quality industrial/residential REITs for rate resilience. Contrarian angles: Consensus may underweight refinancing risk and overestimate lease-up speed — the 25% implied upside assumes clean execution and stable rates. The market could be underpricing a short-term squeeze if CUZ reports consecutive positive leasing/earnings beats, but equally crowded longs make the trade susceptible to a single negative leasing print. Historical parallel: post-crisis REIT recoveries rewarded idiosyncratic operational turnarounds while punishing leverage; treat CUZ as an operational turnaround with rate sensitivity and size positions accordingly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment