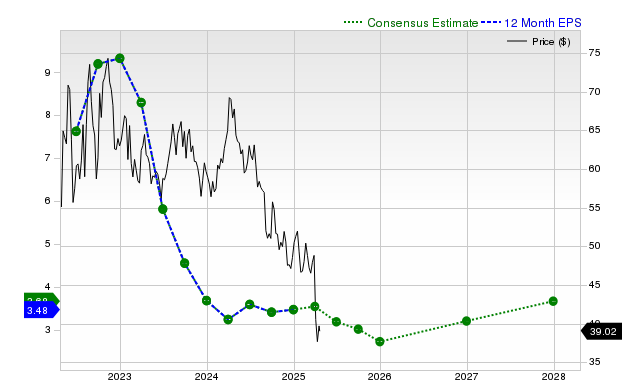

Occidental Petroleum (OXY) has seen its shares decline 3% over the past month, underperforming the S&P 500's 2% gain. While current quarter EPS is projected to fall 39% year-over-year to $0.61, the consensus estimate has positively revised by 5.2% in the last 30 days, though the next fiscal year estimate saw a 6.8% negative revision. The company has consistently beaten EPS estimates in the past four quarters and is assessed with a Zacks Value Style Score of 'B', indicating it trades at a discount to peers. OXY currently holds a Zacks Rank #3 (Hold), suggesting a near-term performance in line with the broader market.

Occidental Petroleum (OXY) exhibits a mixed fundamental picture, characterized by recent stock underperformance and conflicting analyst estimate revisions. The stock's 3% decline over the past month lags both the S&P 500's 2% gain and its industry group's 2.6% loss. Projections indicate significant year-over-year headwinds, with current quarter earnings expected to fall by 39% to $0.61 per share and revenue to decline by 6.4%. Despite these stark YoY comparisons, sell-side analysts have recently upgraded their consensus estimates for the current quarter and fiscal year by 5.2% and 1.2% respectively, suggesting a potential bottoming in near-term expectations. However, this optimism does not extend to the longer term, as the consensus earnings estimate for the next fiscal year has been revised downward by a notable 6.8% in the past month. While the company has a strong history of exceeding EPS estimates in the last four quarters, its valuation, marked by a Zacks Value Style Score of 'B', suggests it is trading at a discount to its peers. This combination of factors culminates in a neutral Zacks Rank #3 (Hold), indicating an expectation of in-line market performance in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.05

Ticker Sentiment