Chubb (CB) is under watch by investors, with shares up 0.3% over the past month, lagging the S&P 500's 6.9% gain. The Zacks consensus estimate forecasts an EPS of $5.84 for the current quarter, an 8.6% increase year-over-year, while revenue is projected to reach $14.85 billion, a 7.2% increase; however, the company's Zacks Rank is currently #3 (Hold), suggesting near-term performance in line with the broader market.

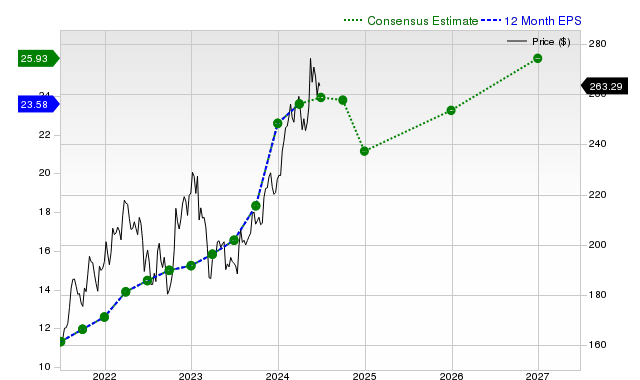

Chubb Limited (CB) presents a mixed financial profile, with its shares returning +0.3% over the past month, substantially lagging the S&P 500's +6.9% gain but outperforming the Zacks Insurance - Property and Casualty sector's -4.2% decline. Current quarter expectations include an 8.6% year-over-year EPS increase to $5.84 and a 7.2% revenue rise to $14.85 billion. However, consensus earnings estimates for the current quarter, current fiscal year, and next fiscal year have experienced slight downward revisions of -0.5%, -0.2%, and -0.3% respectively in the last 30 days. A notable -5.8% decline in EPS is anticipated for the current fiscal year to $21.21, contrasting with a robust projected +19.2% EPS growth to $25.28 for the next fiscal year. In its most recent reported quarter, Chubb's revenues of $13.67 billion (+4.6% YoY) missed consensus estimates by -3.43%, although its EPS of $3.68 significantly surpassed estimates by +12.88%, marking the fourth consecutive quarter of EPS beats. Revenue growth is forecast at +6.3% for the current fiscal year and +6.7% for the next. The stock currently holds a Zacks Rank #3 (Hold) and a Value Style Score of B, indicating it trades at a discount to its peers and suggesting its near-term performance is likely to be in line with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment