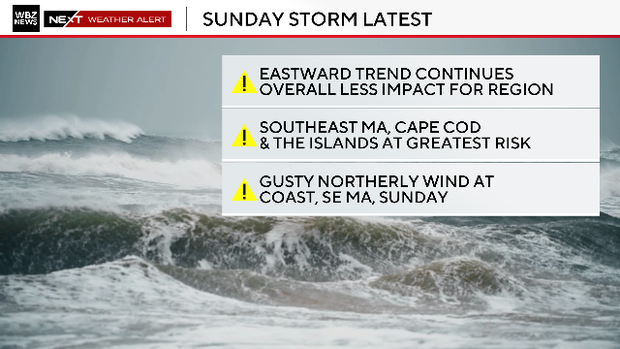

A rapidly deepening winter storm is poised to graze southeastern Massachusetts this weekend, with the highest impacts focused on Cape Cod and the Islands where 3–6" of snow is forecast and 1–3" expected near the Cape Cod Canal to Plymouth; the rest of the coastline (including Boston) is forecast a coating to 1". Strong north to northwest winds will produce gusts of 50–70 mph on the South Shore, Cape Cod, Cape Ann and the Islands (40–50 mph inland through I‑95; 30–40 mph elsewhere), with 6–12 ft waves at east/northeast-facing beaches and 1–2 ft of coastal inundation likely on vulnerable roads during high tides late Sunday and Monday, increasing risk of road closures and localized infrastructure and transportation disruptions. Broader financial market impact is minimal, though insurers, local municipal services and transport/logistics operators could face short-term operational and claims exposure.

Market structure: Near-term winners are regional utility operators (e.g., Eversource ES, National Grid NGG) and remediation/retail suppliers (Home Depot HD, Lowe’s LOW) who capture emergency repair spend; losers are schedule-sensitive transport operators (regional airlines AAL, UAL) and coastal municipalities exposed to flooding. Pricing power will be transient — expect 7–14 day spikes in retail and contractor revenues and 1–2 day spikes in airline cancellations; insurers (TRV, ALL) face loss pick-ups that may pressure quarterly underwriting but are unlikely to move reinsurance pricing absent major catastrophe (> $1bn insured loss in MA). Commodities: prompt Henry Hub (NG) and heating oil futures should see 3–8% knee-jerk lift if cold persists; options IV on regional utility names and airlines will rise 20–50% intraday. Risk assessment: Tail risk remains low-probability/high-impact: an eastward shift producing a direct Cape Cod landfall could create >$500m insured losses and longer supply-chain interruptions (48+ hours) for NE ports. Immediate window is 0–72 hours (disruptions, cancellations), short-term 2–8 weeks (repair revenues, insurance claims), long-term 3–12 months (infrastructure budgets, municipal bond reassessments). Hidden dependencies include tidal timing amplifying flood damage and concentrated contractor capacity (lob-sided recovery if local crews overwhelmed). Key catalysts: updated model runs (6–36 hr), NOAA warnings, and first loss reports from insurers. Trade implications: Tactical plays: buy short-dated call spreads on HD/LOW (7–21 day expiries) to capture incremental DIY/contractor spend; buy front-month NG calls or small long futures position (0.5–1% portfolio) for heating-demand-driven upside. Defensive shorts: small, hedged short of regional airline exposure (AAL/ULCCs) for 3–7 days to capture cancellation risk; buy 2–4 week protective puts on regional utility names only if model shifts toward higher loss probabilities. Rotate 1–3% into civil-construction names (J, VMC, CAT) for 3–9 month recovery play. Contrarian angles: The market likely underprices durable benefits to contractors and construction-equipment OEMs — consensus treats storm as docket noise but municipal repair cycles can drive 6–12 month incremental revenue. Conversely, insurer knee-jerk selling is often overdone for events <$1bn insured loss; shorting broad insurers (TRV, ALL) versus long specialist contractors (J) is a potential pair trade. Historical parallels (localized nor’easters) show retail/contractor revenue pops of +3–8% over 2–6 weeks while insurer reserve adjustments normalize over quarters, creating a window for asymmetric short-term longs in HD/LOW and J.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25