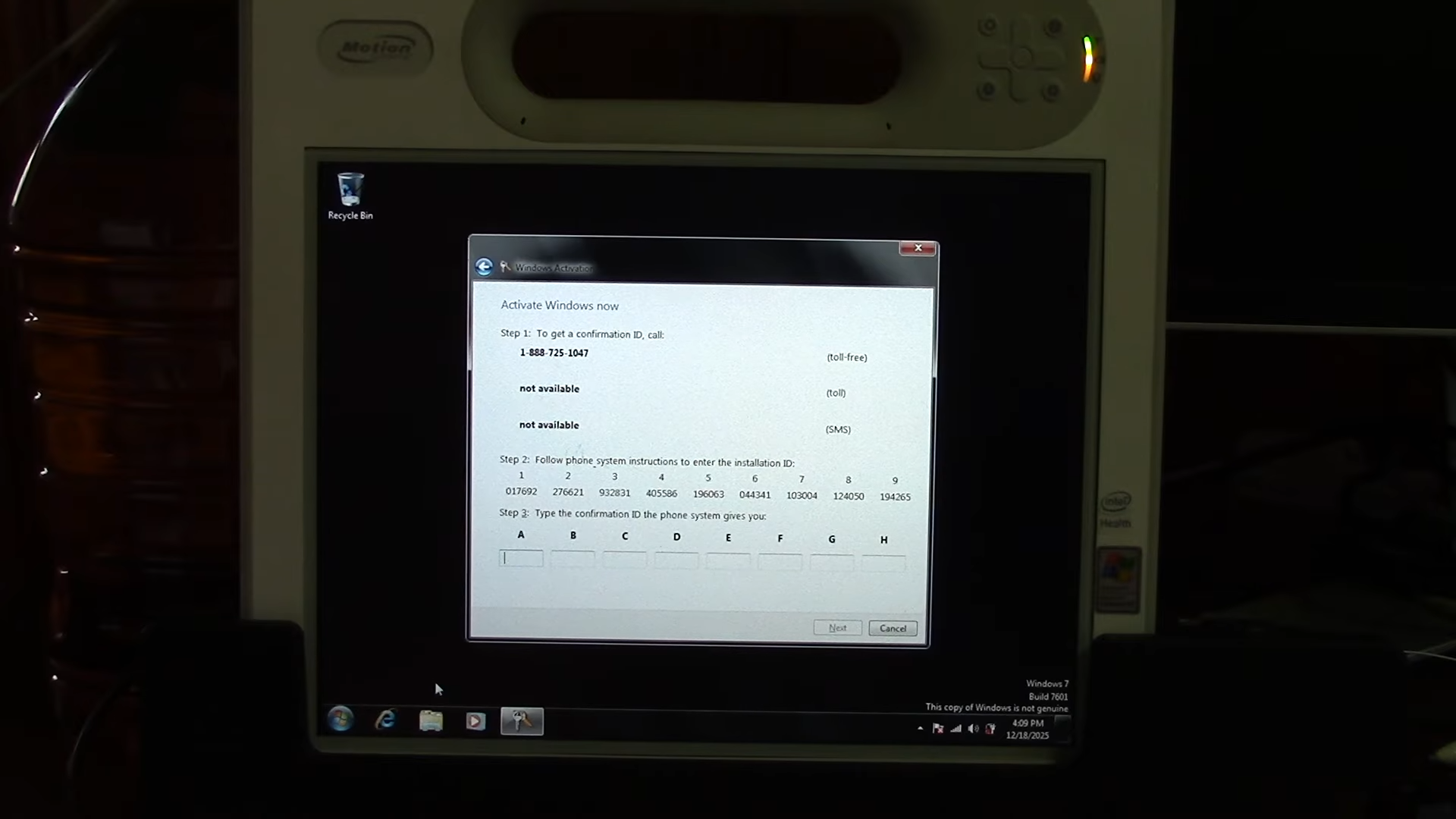

Microsoft has disabled legacy phone-based activation for Windows and Office, routing users to a web-based Product Activation Portal that requires signing in with a Microsoft account; attempts to call the support number yield an automated message and a link to the portal. The change affects legacy systems (e.g., Windows 7 and Office 2010) where local/offline activation was previously used, creating user friction and privacy/account concerns but is unlikely to materially affect Microsoft’s revenues; the move may modestly influence customer sentiment and enterprise migration considerations.

Market structure: Microsoft (MSFT) is the direct beneficiary — forcing web/Microsoft-account activation increases telemetry/touchpoints and marginally strengthens Azure AD/MSA ecosystems and future monetization of identity services. Losers are niche legacy actors (OEM key resellers, refurbishers, help-desk operators) and privacy-first consumers; impact on MSFT top-line is likely immaterial near-term (<1% revenue impact) but strategic for data/moat expansion over years. Risk assessment: Tail risks include EU/UK privacy or competition enforcement (fines or forced opt-outs) and a high-impact operational outage of activation servers that could generate class-action litigation; probability low but severity high (months of reputation/legal cost). Immediate PR/backlash will play out over days-weeks; regulatory and litigation outcomes would materialize over 3–18 months and could force product changes or remediation costs >$100M if precedent cases arise. Trade implications: Favor asymmetric long exposure to MSFT (long-term moat play) while hedging regulatory/oppo risk via short exposure to pure-play identity security vendors whose enterprise moat is weaker (e.g., OKTA) over 6–12 months. Use options for defined risk: buy 6-month MSFT call spread on 5%+ pullbacks and sell short-dated OTM puts to collect premium if implied volatility spikes on headlines. Contrarian angles: The market likely underestimates strategic value of enforced account linkage (data + upsell potential) so a modest buy-on-weakness stance is warranted; conversely, the headline reaction is overdone if investors treat this as a material revenue threat. Historical parallel: Adobe’s online shift compressed friction and expanded recurring revenues — enforcement risk aside, Microsoft’s long-run monetization upside is understated.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment