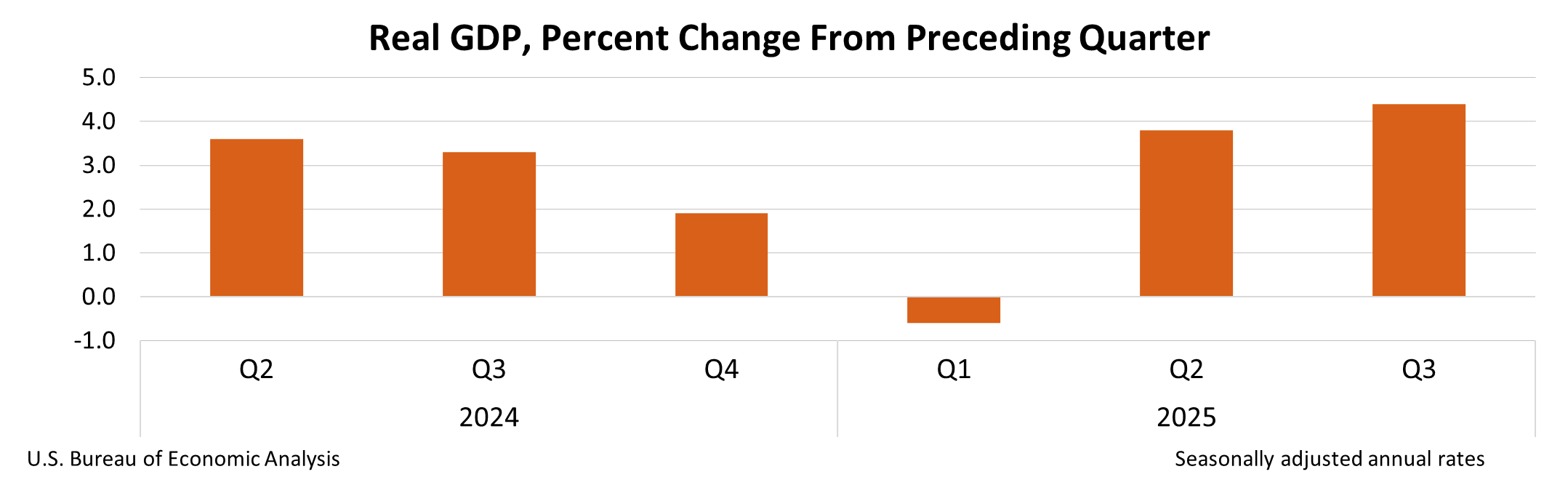

Real GDP rose 4.4% annualized in 2025 Q3 (up 0.1 ppt from the prior estimate), driven by consumer spending, exports, government spending and investment while imports fell. Real final sales to private domestic purchasers increased 2.9%, real GDI rose 2.4%, and corporate profits from current production increased $175.6 billion (a $9.5 billion upward revision). The PCE price index was 2.8% (core PCE 2.9%), and BEA noted industry gains concentrated in private services and goods production; the stronger growth and still-elevated core inflation have implications for risk assets and monetary-policy expectations.

Market structure: A 4.4% Q3 GDP print with 5.3% private services and export-led revisions favors cyclicals and exporters (industrial capital goods, materials, ports/logistics). With PCE at 2.8% and core 2.9%, real demand growth is strong enough to support corporate margins but not so hot as to force immediate aggressive Fed hikes; expect risk-on flows into XLI, XLB, and export-oriented midcaps over the next 1–6 months. Risk assessment: Tail risks include renewed trade restrictions (hitting exporters) and a reversal if inventory-led investment proves transitory; a 20–50% downside in Q4 growth is low-probability but would reflate deflationary impulse in stocks and push 10y yields sharply lower. Near-term (days–weeks) sensitivity centers on 10y yields and upcoming Feb 20 advance GDP and monthly CPI/PCE prints; longer term (quarters) watch residential fixed investment and inventory unwinds. Trade implications: Favor long industrials/materials/transport vs short rate-sensitive defensives. Cross-asset: expect modest USD strength and upward pressure on 10y yields—short-duration fixed income and commodity cyclicals (copper) should outperform; equity option skew will compress as realized vols fall if growth momentum persists, enabling debit call spreads on cyclicals. Contrarian angles: Consensus may underprice the durability of export strength—if ITA data momentum continues, semicapital equipment (DE, CAT) could re-rate before broader cyclical indices. Conversely, the market could be underestimating inventory risk: a repeat inventory drawdown would shock earnings, so size positions with strict stop-losses tied to yield and PCE moves.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.30