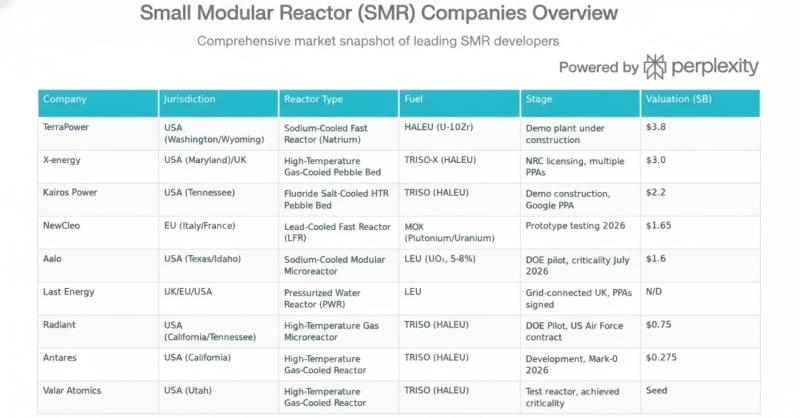

IPO CLUB published a February 2026 note highlighting nine leading Small Modular Reactor (SMR) developers as pre-IPO opportunities, citing projects including TerraPower's Natrium (targeting 2030 commercial ops), Newcleo's lead-cooled LFRs (targeting 2032), X-energy's Xe-100 with Amazon's $500M backing for >5 GW data center deployments, Kairos Power's salt‑cooled Hermes with a TVA PPA for Google by 2027, and Last Energy PWRs with UK/Poland PPAs for 34 units; microreactor firms Aalo, Valar Atomics, Radiant and Antares are pacing 2026–2028 milestones. IPO CLUB — which reports $30M AUM across 30 investments and seven exits — is offering accredited investors access to these opportunities via a $50M Fund I, pitching SMRs as a potential trillion-dollar addressable market driven by AI data-center demand and defense/energy-security spending.

Market structure: Hyperscalers (AMZN, GOOGL, META) and vertically integrated SMR developers (X-energy, Kairos, TerraPower, Newcleo, Last Energy) are primary winners — they capture lower, firm baseload for AI data centers and gain negotiating power on long-term PPAs. Short/intermittent gas-fired generators and merchant power sellers face demand erosion in secured PPA lanes; expect 5–15% potential margin pressure in merchant dispatch revenues over 3–5 years in affected regions. SMR build timelines (2026–2032 targets) create a two-speed market: immediate scarcity of deployed capacity supports premium valuations for proven developers while near-term supply-chain bottlenecks (fabrication, fuel qualification) limit capacity growth. Risk assessment: Tail risks include regulatory reversals (major license denial or ASN-style delay), a serious incident, or anchor tenant withdrawal — each could wipe 30–70% of private valuation for early-stage SMRs and force write-downs. Short-term (days/weeks) market moves will track PPA/regulatory headlines; medium-term (6–24 months) risks center on supply-chain and financing; long-term (3–7 years) execution risk and commodity (uranium, steel) inflation dominate. Hidden dependencies: grid upgrade investment, skilled labor, and continued hyperscaler capital commitment; if any fail, cascade funding shortfalls occur. Key catalysts: new PPAs, NRC/ASN approvals, government subsidy releases; missing any of these for 6–12 months is a material negative. Trade implications: Favor selective exposure — prioritize names with signed anchor PPAs and regulatory milestones (e.g., Kairos/TVA, X‑energy/Amazon). Public plays: overweight AMZN/GOOGL for secular data-center resilience; add uranium/miners for commodity upside. Use options to cap downside (12–24 month call spreads on AMZN/GOOGL; long-dated calls on uranium miners). Size private-secondary bets small (1–3% portfolio) with 5–7 year hold, require milestone-based tranche funding. Contrarian angles: Consensus underestimates timing/execution risk — many targets (2030+) imply multi-year binary outcomes; valuations may be pricing in optimistic deployment curves. Mispricings: premium private secondaries without anchor PPAs or regulatory proof should be avoided; conversely, public uranium miners may underreact to multiple large PPA announcements, creating asymmetric upside. Historical parallel: early renewables hype then consolidation — expect similar shakeouts; political backlash or concentrated on-site reactors could trigger regulatory tightening and re-rate winners and losers unexpectedly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment