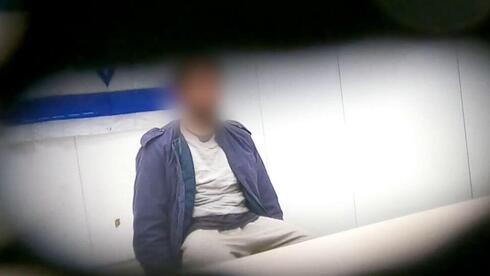

IDF forces captured Hezbollah's Radwan Force operatives in southern Lebanon who were preparing to fire an anti-tank missile; interrogations report low morale and that Hezbollah joined fighting in support of Iran. The incident underscores continued cross-border hostilities with Iran-aligned elements and raises the risk of localized escalation. Expect modest, short-lived risk-off moves in regional assets and oil (potentially up to ~1-2%) and selective interest in defense-related equities; absent broader escalation the market impact should remain limited.

A weakening of front-line morale combined with clearer Iranian direction is likely to change the character of the fight rather than end it — expect fewer close-range ambushes and more stand-off fires (missiles, guided rockets, UAV strikes) and electronic warfare. That shifts near-term demand to precision munitions, sensors, and integrated air/missile defense systems, favoring firms with short production lead times or large inventories; procurement decisions will accelerate within weeks-to-months rather than years. Operationally, the second-order supply effect is an acute draw on precision-guided munitions and seeker heads with replenishment lead times of 6–18 months; NATO/US stockpile assistance or commercial buys will show up as order flows and margin upside for mid-tier suppliers within a 3–9 month window. Conversely, insurers, regional shipping (war-risk premiums), and EM sovereign credit in proximate states will face pressure in days-to-weeks as perceived escalation probability rises above the market’s baseline. Catalysts that will reverse the trend are also identifiable: a credible Iranian de-escalation signal or rapid Hezbollah leadership fractures would remove the premium in 1–8 weeks; sustained Iranian logistics or state-level escalation would entrench demand and re-rate defense names over 3–12 months. Net: tactical risk-off near-term for regional assets, tactical risk-on for missile/air-defense supply chains and selective hedges for energy/shipping volatility.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15