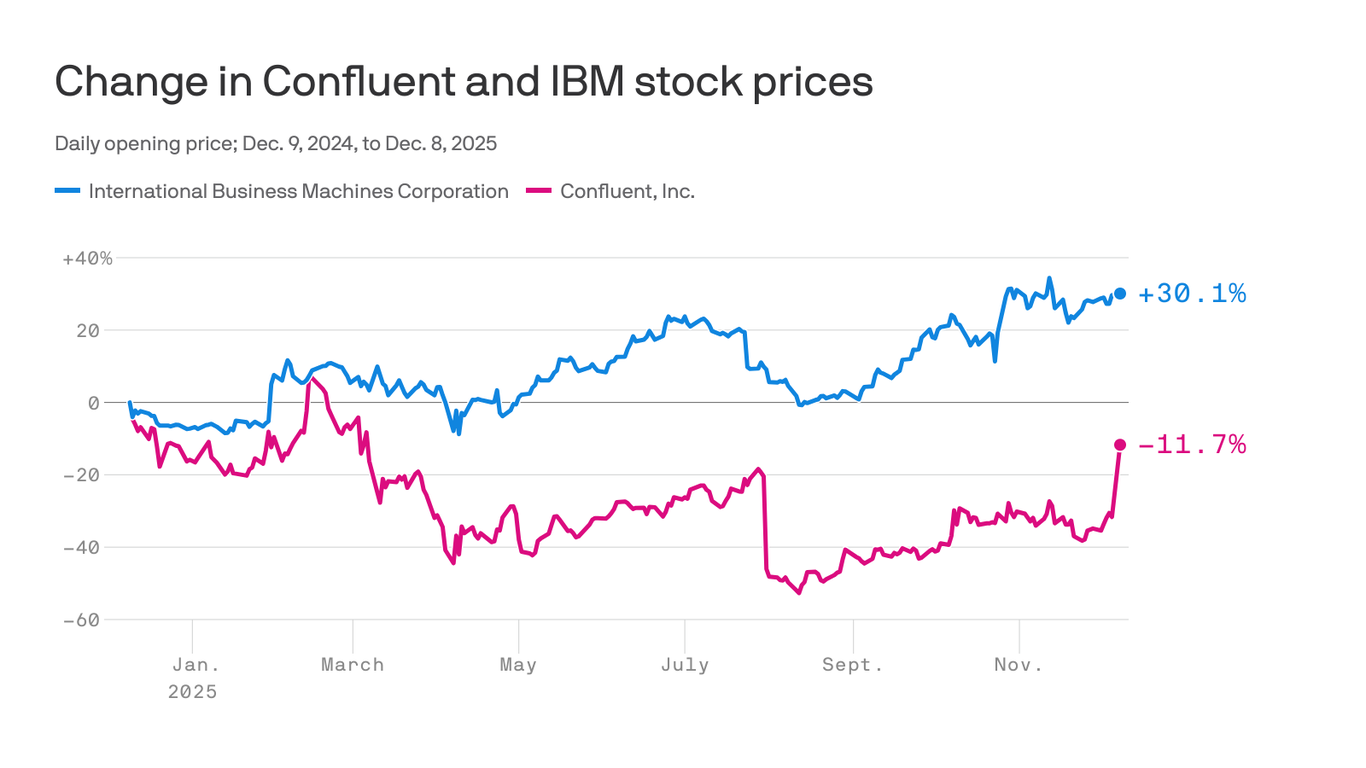

IBM agreed to acquire data-infrastructure firm Confluent for $11 billion in cash, paying $31 per share — a 34% premium to Friday's close — as part of CEO Arvind Krishna's strategy of bolstering AI and open-source capabilities following prior deals like Red Hat and Hashi. Confluent, which went public in June 2021 and peaked at $93.60 later that year, will be integrated to strengthen IBM's competitiveness against Google and Microsoft in large-scale computing and AI infrastructure; the deal helped underscore investor confidence in IBM's strategic pivot as its stock has more than doubled under Krishna.

Market structure: IBM’s purchase of Confluent makes IBM an immediate winner in enterprise streaming and event-driven data, improving its AI data stack and cross-sell into Red Hat customers; Confluent shareholders capture a one-time +34% premium while independent managed-streaming vendors face higher bar for enterprise trust. Pricing power for enterprise managed Kafka will rise modestly as a large incumbent bundles services, tightening supply of fully supported open-source streaming offerings and nudging enterprise demand toward vendor-managed solutions over 12–36 months. Cross-asset: expect modest tightening in IBM credit spreads (positive for IG bonds) and a short-lived rise in IBM equity implied vol; broader USD/FX moves negligible. Risk assessment: Key tail risks include community fork of Confluent projects (undermining enterprise lock-in), material customer churn (>10% ARR loss), or regulatory/antitrust probes; probability low–medium but impact high. Time horizons: immediate (days) — Confluent equity stops trading; short-term (weeks/months) — IBM equity reaction to financing and integration plans; long-term (2–4 years) — revenue synergies and retention determine IRR. Catalysts: definitive merger filings, customer renewal data, and developer-community signals in the next 30–90 days. Trade implications: Primary trade is measured long IBM (IBM) to capture consolidation premium and AI-stack optionality; prefer structured exposure (call spreads) rather than outright leverage given integration risk. Pair/relative ideas favor long IBM vs select hyperscalers only if cloud consolidation increases enterprise preference for vendor-managed open-source; consider IG bond purchases if spread >120bps over Treasuries for 3–5 year duration. Use options to define downside: buy 9–12 month call spreads or collar to cap loss and target 15–25% upside. Contrarian angles: Market consensus treats this as straightforward strategic fit but underestimates open-source fragility and execution risk — Confluent’s peak valuation gap (from $93.6 to $31) signals structural growth deceleration that IBM inherits. Historical parallels: Red Hat worked but many large software takeovers fail to sustain growth; unintended consequence could be increased hyperscaler bundling (Microsoft/Google discounting real-time services) which would compress margins. A specific sell trigger: IPO-like customer attrition data or >$5bn of new debt issuance within 180 days should materially reprice IBM down.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.36

Ticker Sentiment