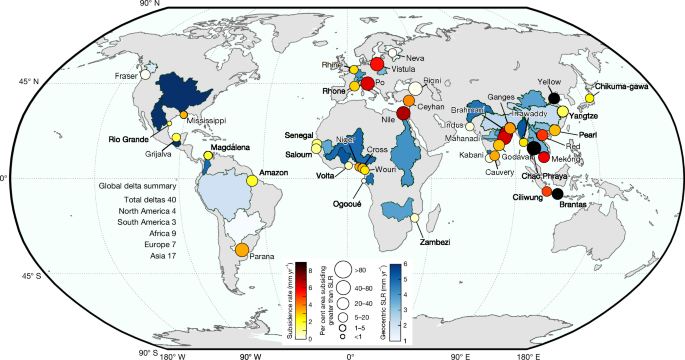

A global Sentinel-1 InSAR analysis of 40 major river deltas finds pervasive and spatially variable subsidence, estimating 460,370 km2 of delta area exposed to sinking and that at least 35% of delta area is subsiding; 38 deltas have >50% area sinking and 19 deltas show >90% of area affected. Thirteen deltas (including Nile, Po, Mekong, Yellow River, Chao Phraya) have average subsidence exceeding current global SLR (~4 mm/yr), 18 deltas have subsidence outpacing regional geocentric SLR—exposing ~236 million people—and groundwater-storage loss is identified as the dominant anthropogenic driver in many systems. The study projects that contemporary subsidence rates will continue to dominate relative sea-level rise through mid- and end-century in most deltas, signaling material long-term risk to coastal infrastructure, ports, real estate and insurance exposures and implying demand for targeted adaptation and capital allocation.

Market structure: Subsidence turns deltas into concentrated winners (flood‑defense & dredging, water‑tech, heavy equipment, reinsurers) and losers (coastal real‑estate, port operators, local sovereigns in low ND‑GAIN countries). Quantitatively, 18/40 deltas already have subsidence > geocentric SLR and ~236M people live where subsidence dominates — implying multi‑decade demand for remediation capex (dredging, levees, managed aquifer recharge) and recurring O&M revenue streams. Risk assessment: Tail risks include sudden port incapacitation (weeks) causing regional grain/coal export shocks and commodity price spikes, and sovereign stress in highly exposed low‑readiness states (years) that could force debt restructurings. Near term (0–12 months) storm/permit events can spike local losses; medium term (1–3 years) policy (groundwater caps, large infrastructure packages) will re‑rate sectors; long term (decades) chronic RSLR + subsidence will reprice coastal land values. Trade implications: Favor equities providing solutions and recurring revenues: engineering (Jacobs J, AECOM ACM), dredging (GLDD), water tech (Xylem XYL), and construction machinery (CAT) on 12–36 month horizons; underweight/hedge coastal RE via VNQ/IYR. Use options: protective put spreads on VNQ (6–12 month) and 12–24 month call spreads on J/ACM to capture re‑rating. Allocate TIPS (TIP) or 5–10yr Treasuries (TLT) as macro hedge against fiscal spending shocks. Contrarian angles: Consensus underprices policy effectiveness — decisive groundwater regulation or sediment‑diversion projects can restore asset values within 3–7 years and create asymmetric upside for contractors already priced for secular demand. Conversely, defence contractors may be crowded; watch for mispricing where VNQ exposure to actual delta risk is low — selective shorting beats blanket REIT shorts. Trigger thresholds: ND‑GAIN improvement >0.05 or announced national adaptation spend >1% GDP should prompt rotation into local infrastructure names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50