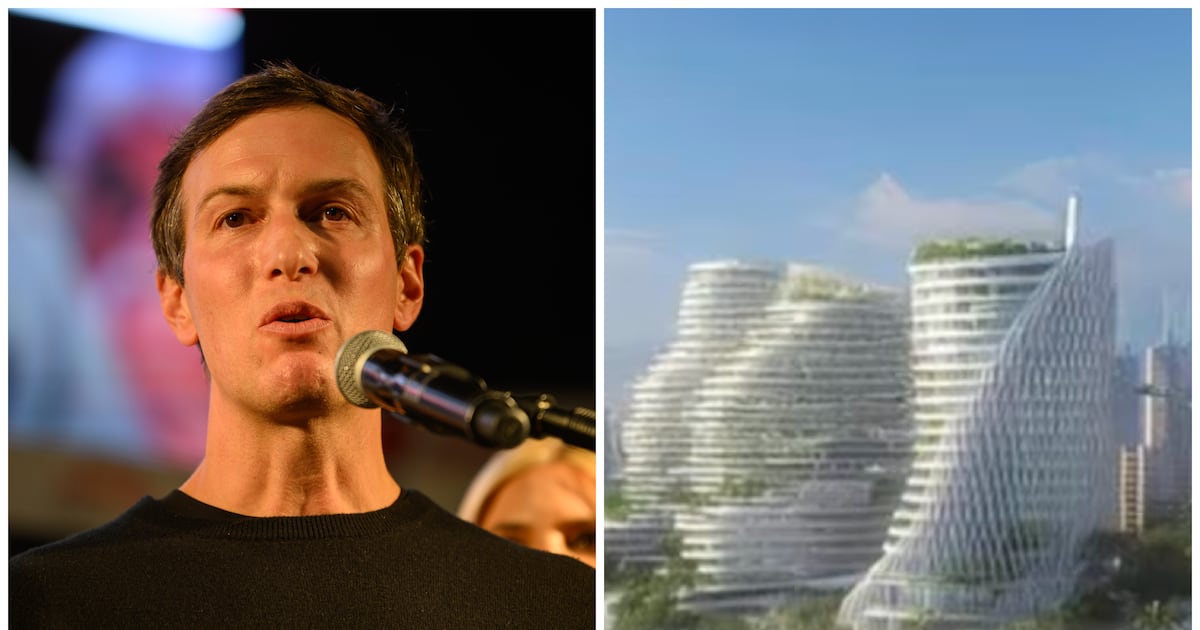

Jared Kushner and developer Steve Witkoff have circulated a 32-slide “Project Sunrise” proposal to Middle Eastern governments outlining a $112.1 billion, 10-year plan to rebuild Gaza as a high-tech tourist metropolis, with the U.S. reportedly committing 20% of development costs and nearly $60 billion in grants and debt guarantees. The pitch touts AI-driven grids, high-speed rail and luxury resorts but lacks concrete plans for resettling 2 million displaced Palestinians and concedes the project cannot proceed unless Hamas disarms; experts and officials voiced serious feasibility and investor-risk concerns given unresolved security, clearance of unexploded ordnance, massive rubble removal and humanitarian obstacles.

Market structure: A $112.1bn reconstruction thesis (≈$10–12bn/year) would concentrate demand in heavy civils, power/AI infra and hospitality supply chains, benefiting large defense/engineering contractors, heavy-equipment makers and steel/cement producers while disadvantaging smaller regional contractors and insurers unwilling to underwrite political risk. Pricing power shifts to global contractors and reinsurers able to absorb credit guarantees; materials prices could see low-single-digit incremental regional demand (1–3% p.a.) if work commences. Risk assessment: The dominant tail risk is political failure — Hamas non‑disarmament or renewed hostilities — which makes a >50% chance of project delay or cancellation in the next 12 months reasonable; operational cost overruns from demining/rubble removal could blow budgets by 30–100%. Key hidden dependency is conditionality: US Congressional appropriations and Gulf sovereign guarantees; catalysts that would materially re-rate assets are (a) a US vote committing >$20bn within 60 days or (b) a credible 90‑day ceasefire and security framework. Trade implications: Tactical overweight defense (RTX, LMT) and materials (CAT, NUE) while underweight MENA sovereign credit and regional banks; prefer option-defined exposure (9–12 month 12–20% OTM call spreads) to capture upside if reconstruction is funded but limit premium loss. Entry should be staged: 25% exposure now, add to 100% if US/Gulf pledges exceed $20bn or a 30‑day ceasefire is sustained. Contrarian angle: Consensus dismisses the plan as fantasy but underestimates Gulf private capital’s ability to co‑finance if guarantees reduce downside; however reputational/regulatory and ESG litigation risk is underpriced — avoid contractors taking direct site roles without political indemnities. Historical parallel: Iraq/Afghanistan rebuilds delivered outsized contractor profits but with long tails, litigation and contingent liabilities—position for multi‑year payoffs, not a quick trade.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45