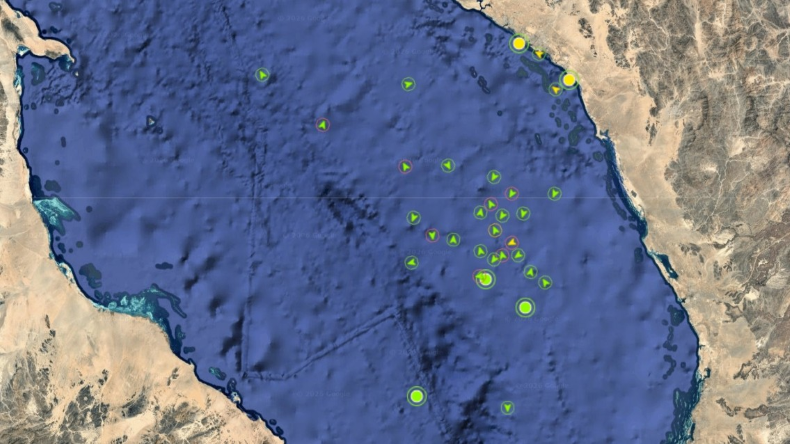

Yanbu loaded 4.1m bpd in the week ending Mar 22 (more than triple the 2025 average of 1.3m bpd) and accounted for ~31% of VLCC loadings that week versus 5% in 2025, while global seaborne exports fell from a 51m bpd 2025 average to ~39m bpd after the Strait of Hormuz closure. The Houthi Humanitarian Operations Coordination Center says there is "no reason to prevent" Yanbu trade at present, but Iranian and Houthi threats and the risk of US military action make Bab el Mandeb a critical single point of failure. Any closure or disruption would force longer reroutes (around Africa or via Suez/Sumed), sharply reduce VLCC trade economics and create outsized oil-supply and tanker-demand shocks, posing material market-wide risk.

The market is treating the Red Sea as the marginal artery for seaborne crude and VLCC demand; as a result, small changes in chokepoint access create outsized moves in freight economics and crude basis. A closure or significant denial of Bab el Mandeb would not just reroute tonnage — it would raise round‑trip voyage days (order-of-magnitude +30–50% on impacted trades), materially increase bunker consumption and ballast inefficiency, and plausibly double spot VLCC time charter equivalents for a multi-week window while vessel repositioning occurs.

Second-order winners and losers are non-obvious: owners of large, slow-moving VLCCs and counterparties long FFAs/charter exposure capture the initial windfall, while Asian refiners and traders that rely on predictable liftings suffer margin compression and financing strain from delayed receipts and wider crude basis. Logistics players (Suez/Sumed substitute routes, bunker suppliers, and freight derivatives liquidity providers) will see immediate revenue upside but also elevated operational risk and insurance costs, raising breakevens for marginal trades by several dollars per barrel.

Key catalysts are discrete and front-loaded: a US/Iran military escalation or a calibrated Houthi interdiction can move markets within days; conversely diplomatic progress or credible local protection arrangements can reverse the move in weeks to a few months as ballast corrects. Given vessel re‑positioning lags (multi-week) the market is prone to overshoot both on the upside and on the downside — volatility, not a new steady state, is the most likely near-term regime.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25