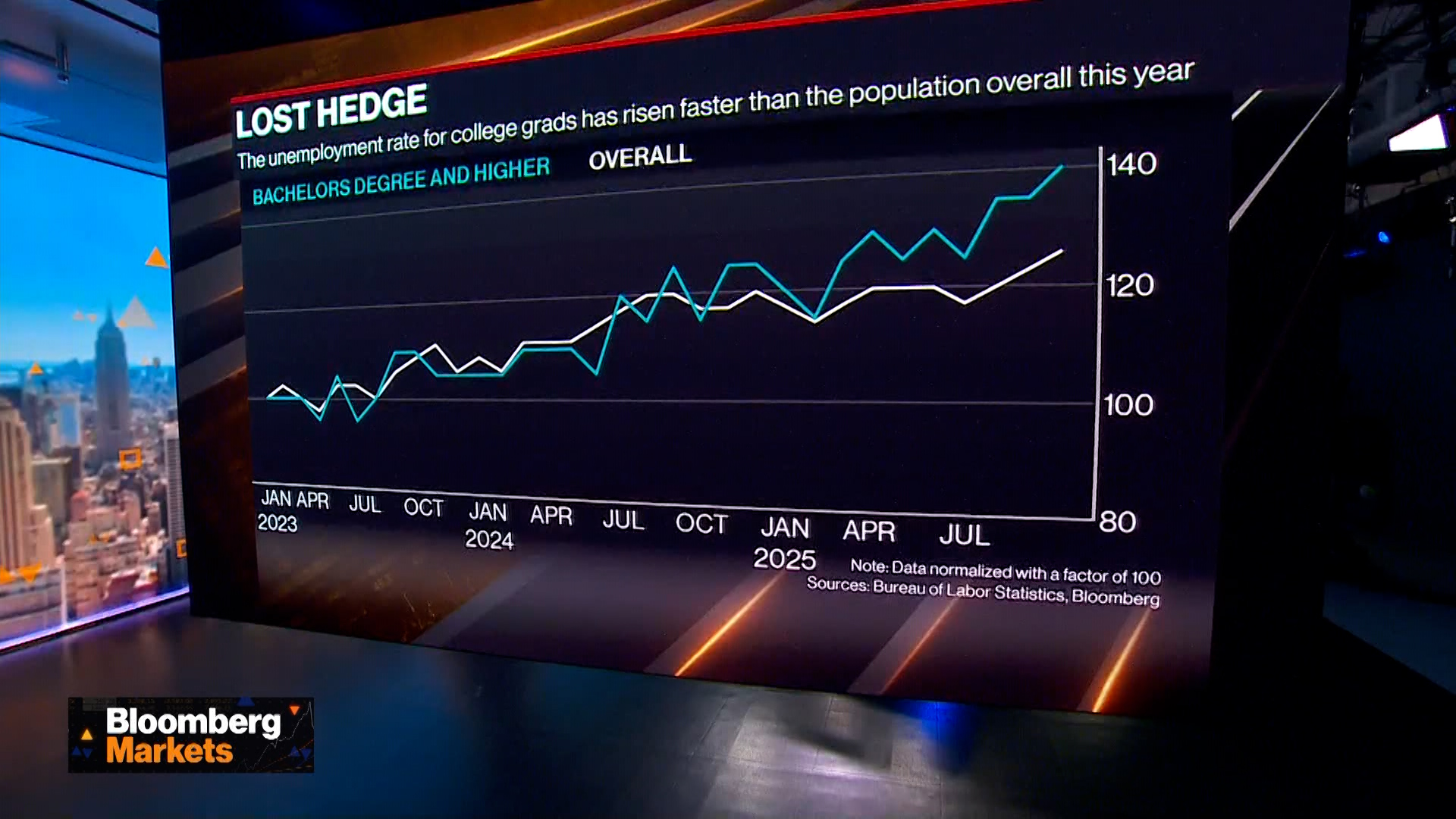

Recent labor-market analysis shows growing convergence between college and non-college outcomes, with recent graduates particularly vulnerable; the share of college-educated workers has roughly doubled since the 1990s (cited ~20% to ~40%), reducing the scarcity premium that previously insulated grads. Current data do not yet show widespread AI-driven displacement, but the author warns a recession could amplify hiring discrimination against inexperienced hires; the column frames college as akin to a 'junk bond'—offering positive expected returns but not the former risk-free, above-market guarantee, so school cost, quality and field of study matter materially for outcomes.

Market structure: Recent-graduate weakness signals winners: AI infrastructure and upskilling providers (cloud, GPU vendors, bootcamps) capture corporate spend as firms substitute training with tooling; losers include entry-level hiring-heavy industries (consumer discretionary, entry-level tech/finance roles) and private student-lenders. Expect pricing power to shift from labor to capital — firms that deploy AI at scale gain margin expansion while low-skill wage growth moderates; near-term demand for starter homes, autos and credit will soften by mid‑cycle if unemployment rises 50–100bps. Risk assessment: Tail risks include a rapid AI-driven substitution shock in a recession (30%+ downside to entry hiring) or policy/regulatory responses (robot taxes, wage subsidies) that re-price labor economics. Immediate (days) risk is sentiment; short-term (3–6 months) is hiring guidance and consumer credit flow; long-term (12–36 months) is structural labor reallocation and higher education ROI erosion. Hidden dependencies: geographic concentration (coastal tech vs. heartland) and student-loan policy changes that can suddenly re-risk banks and ABS conduits. Trade implications: Favor long AI infra (NVDA, MSFT, GOOGL) via capped option structures to monetize continued capex, and hedge with long-duration Treasuries (TLT) if recession probability breaches 25% in Fed funds futures. Short cyclical demand exposures: homebuilders (PHM, DHI) and private-student-lender SLM for 3–12 months; use pair trades to neutralize beta (e.g., long NVDA / short PHM). Monitor hiring guides, MBA/grad enrollment trends and private-loan delinquency monthly as execution triggers. Contrarian angles: Consensus underestimates that experienced-college grads remain scarce — high-skill labor intensives may sustain wage inflation, so pure broad short on “college premium” sectors is risky. Reaction may be overdone for diversified large-cap tech where AI increases productivity and revenue per head; mispricing exists in single-theme consumer names and ABS where credit risk is not fully priced. Historical parallel: 2000 tech-employment shakeouts eventually reallocated capital into higher productivity leaders — favor concentrated winners, hedge cyclicals aggressively.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30