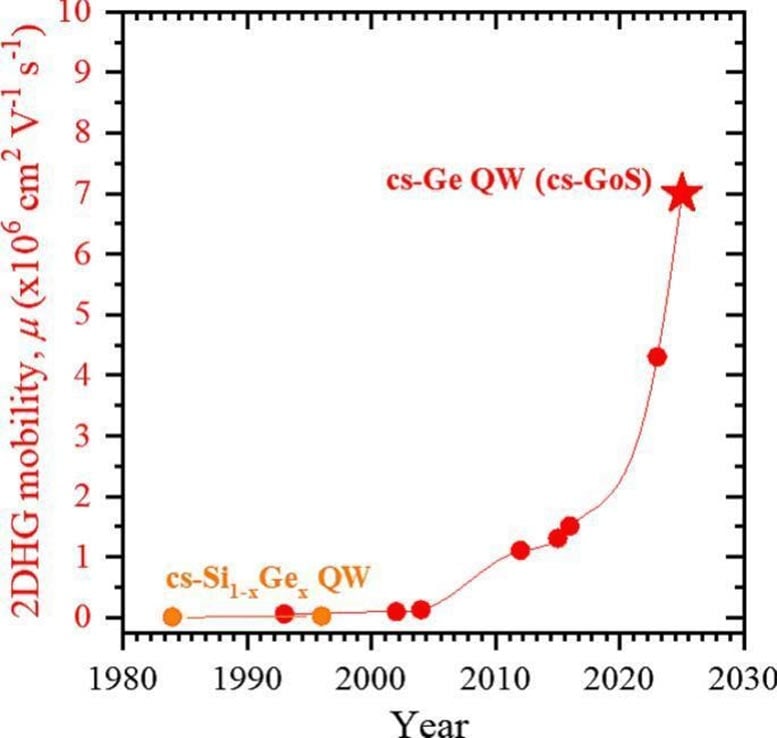

Researchers at the University of Warwick and the National Research Council of Canada report a record hole mobility of 7.15×10^6 cm^2V^-1s^-1 in a nanometer-thin compressively strained germanium-on-silicon (cs-GoS) layer, versus roughly 450 cm^2V^-1s^-1 for industrial silicon. The cs-GoS material is fully compatible with existing silicon manufacturing and could enable faster, lower-power chips with applications in quantum devices, spin qubits, AI accelerators and energy-efficient data-center hardware, although commercial adoption timelines and scaling remain uncertain.

Market structure: Immediate winners are semiconductor equipment and advanced-epitaxy toolmakers (Applied Materials AMAT, Lam Research LRCX, KLA KLAC, ASML ASML) and leading foundries able to qualify new materials (TSMC TSM, Samsung SSNLF, Intel INTC). Losses are niche III-V/GaAs RF suppliers (Qorvo QRVO, Skyworks SWKS) and small germanium material vendors if scale-up fails; pricing power will accrue to equipment vendors and qualified fabs as early adopters (potential 10–30% incremental tool spend per qualified line). Cross-asset: modest upward pressure on capex-sensitive high-yield tech credit spreads tightening if orders ramp; commodity germanium demand could lift specialty metal/gas suppliers by low-single-digit revenue, FX benefits to TSMC-related TWD, limited immediate bond market impact. Risks: Tail risks include scale-up failure (yield/thermal incompatibility), IP litigation slowing licensing, or export controls restricting tooling/supply to China — each could wipe out expected 2–5 year revenue streams. Timing: negligible market reaction in days, prototype/pilot news likely within 3–12 months, tangible revenue and market-share shifts 24–48 months. Hidden dependencies: integration into CMP/BEOL flows, yield drag, and germanium sourcing (recycling vs mining) could materially change unit economics. Trade implications: Direct plays — establish small, staged long exposure to AMAT/LRCX/KLAC (1–2% each) and TSM (1%) targeting 12–36 month windows; use 9–15 month call spreads to limit downside (buy ATM, sell 20–30% OTM). Pair trade — long AMAT (+1.0%) / short QRVO (−0.5%) to express tool demand vs GaAs displacement. Entry: scale in over 3 months; exit or hedge if no foundry pilot announcements within 12 months or if quarterlies miss capex guide by >15%. Contrarian view: Market will likely underprice timetable friction — material transitions historically take 3–7 years (SiGe, high-k). Adoption risk and potential germanium supply bottlenecks make a fast re-rating unlikely; therefore size positions conservatively and prefer option spreads over outright long. Unexpected consequence: aggressive adoption could accelerate equipment orders and tighten used-tool supply, creating short-term scarcity-driven rallies; hedge with short-dated puts sized 25–50% of position until pilot confirmations occur.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45