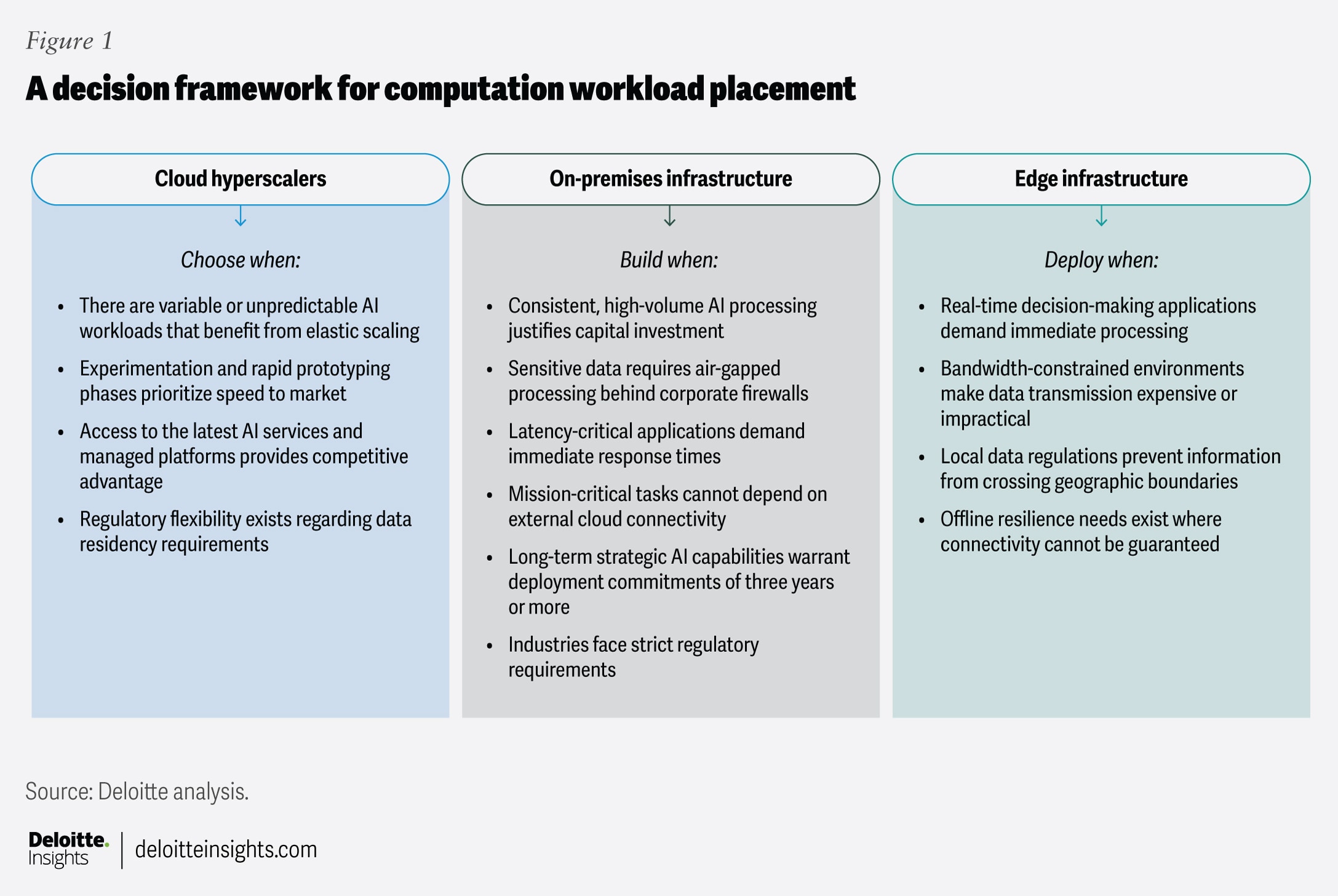

Enterprises moving AI from proofs-of-concept to production are seeing recurring inference demand far outstrip per-inference cost declines—inference costs have fallen roughly 280-fold in two years—driving explosive overall AI spending and monthly bills in the tens of millions for some firms, especially where continuous “agentic” AI is used. Economics, plus data sovereignty, latency, IP protection and resilience concerns, are pushing firms away from a binary cloud/on-prem choice toward three-tier hybrid architectures (cloud for elasticity, on‑prem for predictable high-volume inference, edge for ultra-low latency), fueling new data-center builds and colocation activity and prompting reassessment of capex vs. opex when cloud costs approach roughly 60–70% of equivalent hardware. For investors, the winners will likely be companies that control AI-optimized hardware, orchestration and “AI factory” stacks, data-center and advanced cooling technologies, and the skilled workforce and software agents needed to continuously optimize hybrid portfolios—with sustainability strategies (liquid cooling, renewables, even nuclear) an increasingly important differentiator.

Enterprises moving generative AI from proofs-of-concept to production report near-constant inference demand that has outpaced rapid per-inference cost declines; the article cites a roughly 280-fold drop in inference costs over two years, yet overall AI spending has surged with some organizations seeing monthly bills in the tens of millions and agentic (continuous inference) workloads identified as the largest cost driver. Beyond raw cost, firms are repricing infrastructure decisions around data sovereignty, latency (sub-10 ms requirements for real-time systems), intellectual-property protection, and resilience, prompting repatriation of compute and new regional data-center builds such as Thylander’s Danish colocations. Market and vendor responses favor hybrid, three-tier architectures: public cloud for elastic training and experimentation, on-premises for high-volume predictable inference, and edge for ultra-low-latency tasks, with Dell implementing governance via an architecture review board and proposing “AI factory” stacks; operational complexity and a talent gap mean enterprises seek unified orchestration (Amazon Bedrock agents are an early example) and will monitor a practical cost tipping point where cloud OPEX reaches about 60%–70% of equivalent hardware CapEx. Strategic implications include clear winners among providers of AI-optimized hardware, advanced cooling and networking, colocation and orchestration software, and training programs to close the skills gap; sustainability choices (liquid cooling, renewables, even nuclear) and the transition to mixed CPU/GPU and specialized processors will be differentiators. Signals show moderately positive sentiment (0.45) and medium market impact (0.5), with per-ticker sentiment favoring DELL (0.6) over AMZN (0.25) and MSFT (0.1), which aligns with the article’s focus on infrastructure vendors and orchestration platforms.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment