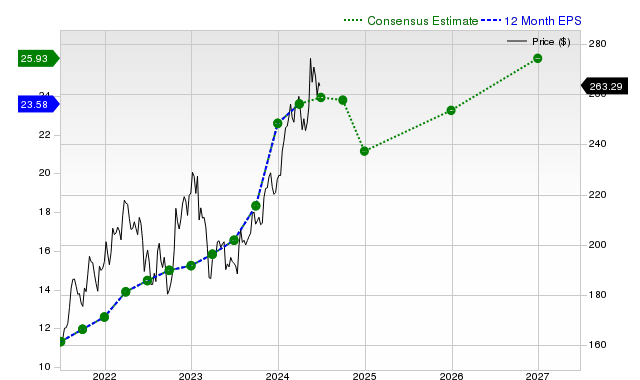

Chubb (CB) shares have underperformed the S&P 500 over the past month, gaining 0.7% versus the index's 3.9%, yet outperforming its P&C insurance industry peers. The company faces a mixed earnings outlook, with current fiscal year EPS projected to decline 5.8% to $21.21, but next fiscal year estimates anticipate a 19.2% increase to $25.28. While Chubb recently missed revenue estimates, it consistently beat EPS forecasts. The stock carries a Zacks Rank #3 (Hold), indicating expected in-line market performance, and its valuation is deemed at par with peers.

Chubb Limited (CB) exhibits a mixed fundamental picture, contributing to its recent market underperformance. Over the past month, the stock's +0.7% return has lagged the S&P 500's +3.9% gain, though it has outperformed its Property and Casualty insurance peer group, which declined by 2.5%. The earnings outlook presents a near-term challenge, with consensus estimates for the current fiscal year pointing to a 5.8% year-over-year decline in EPS to $21.21. However, this is followed by a strong rebound forecast for the next fiscal year, with expected EPS of $25.28, representing 19.2% growth. Notably, these analyst estimates have remained unchanged over the last 30 days, suggesting a lack of new catalysts to shift sentiment. In its last reported quarter, Chubb demonstrated a recurring pattern: it missed revenue consensus by 3.43% but surpassed EPS estimates by a significant 12.88%, a trend observed over the past year. This indicates effective bottom-line management but raises questions about top-line momentum, despite forecasts for 6-7% annual revenue growth. With a Zacks Rank #3 (Hold) and a 'C' grade for value, the stock is considered fairly valued relative to peers, suggesting it is likely to perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment