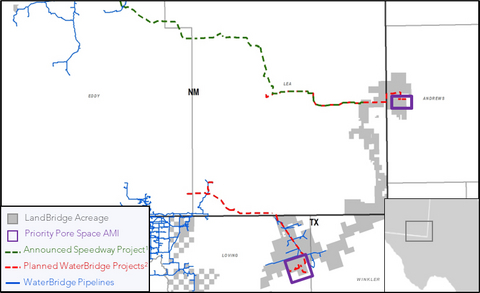

LandBridge (NYSE:LB) shares recently fell to a new 2025 low, down 42% from their 52-week high, despite the company reporting robust Q2 2025 results with revenues up 83% year-over-year to $47.5 million and an 89% adjusted EBITDA margin. The company, which operates a unique low-CapEx model monetizing Permian Basin surface and water rights, announced significant long-term agreements, including a 10-year pore space deal with Devon Energy and strategic partnerships supporting future data center development, further bolstered by a favorable Texas Supreme Court ruling on pore space ownership. While the market reacted to a slight guidance adjustment due to revenue timing and the absence of immediate major data center announcements, the article posits that these long-lead-time deals position LandBridge for substantial future growth in critical water management and 'Powered Land' solutions, suggesting its current 26x EV/EBITDA valuation undervalues its high-margin, predictable cash flows and long-term potential.

LandBridge (LB) has experienced a significant share price contraction, falling 42% from its 52-week high, despite reporting strong Q2 2025 financial results. The company posted an 83% year-over-year revenue increase to $47.5 million, underpinned by robust surface use royalties, and maintained exceptional profitability with an 89% adjusted EBITDA margin and a 76% free cash flow margin. The market's negative reaction appears driven by a modest downward revision of its full-year 2025 adjusted EBITDA guidance to a range of $160 million to $180 million, attributed to the timing of a solar project's revenue, and the absence of a major data center deal announcement. However, LandBridge secured several long-term strategic agreements, including a 10-year pore space reservation deal with Devon Energy (DVN) commencing in 2Q27 and partnerships with independent power producers to support future data center infrastructure. The company's unique, low-CapEx business model, which monetizes surface and water rights in the Permian Basin, is further bolstered by a recent Texas Supreme Court ruling that solidifies its ownership of valuable pore space. The stock's current valuation of 26x the EBITDA guidance midpoint and a high 20% short interest reflect a market debate between near-term concerns over project timelines and the company's long-term, contracted growth potential in critical water management and power infrastructure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment