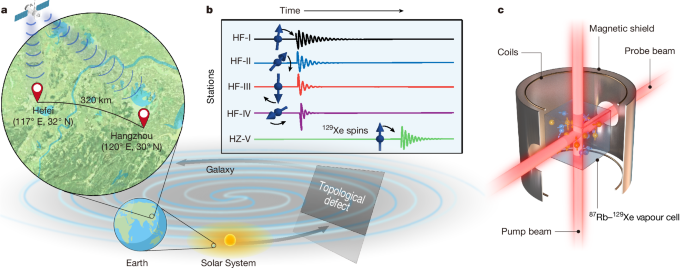

A distributed intercity network of five hyperpolarized noble-gas spin sensors measured transient spin rotations with ~10^-6 rad sensitivity and found no signal, setting laboratory constraints on the axion–nucleon coupling across axion masses from 10 peV to 0.2 μeV. The experiment establishes a limit of 4.1×10^10 GeV at 84 peV, exceeding some astrophysical bounds under different model assumptions, and validates a scalable quantum-sensor approach that could influence future investment and commercialization in quantum sensing technologies for fundamental-physics searches.

Market structure: This experiment strengthens demand signals for precision quantum- and spin-sensor instrumentation (nuclear magnetic resonance, magnetometers, cryogenics), favoring specialist instrument vendors with recurring service revenue (e.g., BRKR, TMO, A) and niche precision-manufacturing suppliers that win government R&D contracts. Mid-cap industrials (DOV) could see modest upside from specialized components but lack pricing power versus pure-play instrument vendors; commoditized suppliers could be losers if R&D budgets concentrate on a smaller set of high-end vendors. Expect modest reallocation of R&D spend: +5–15% annual growth in orders to specialized instrument makers over 12–36 months if follow-up funding occurs. Risk assessment: Principal tail risk is scientific non-reproducibility or null follow-ups that could cut government funding and vaporize forward revenue expectations—this is a 10–30% downside event for pure-play quantum names within 6–18 months. Regulatory/ export-control risks (sensitive sensor tech) create operational constraints and could delay commercialization by 1–3 years; supply-chain bottlenecks (rare-earths, cryo-coolers) are second-order risks. Catalysts that flip outcomes: public grant awards or large defense contracts (positive) vs. failed replication papers or funding freezes (negative). Trade implications: Tactical overweight scientific-instrument names: establish 1–2% long positions in BRKR and A each, horizon 6–18 months, target total return +20–40% on successful funding/collaboration announcements; hedge with 3–6 month protective puts if position >2%. Options: buy 9–15 month call spreads on BRKR (25–35% OTM) sized to 1–2% of portfolio to cap premium while keeping upside. Underweight generic industrial cyclicals by 1–2% (trim DOV exposure if it exceeds 3% allocation) and rotate into the instrument names on any pullback >10%. Contrarian angles: The market will likely overestimate short-term commercialization—realistic adoption is 2–5 years—so avoid paying rich multiples for small-cap “quantum” story stocks without defensible IP or service revenue. Look for mispricings where quality balance sheets + steady service revenue (BRKR, TMO) trade at <15x EV/EBITDA despite exposure to quantum upgrades; these are safer longs. Watch for negative sentiment triggers (failed replication, funding announcements) as high-conviction entry points if fundamentals remain intact.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment