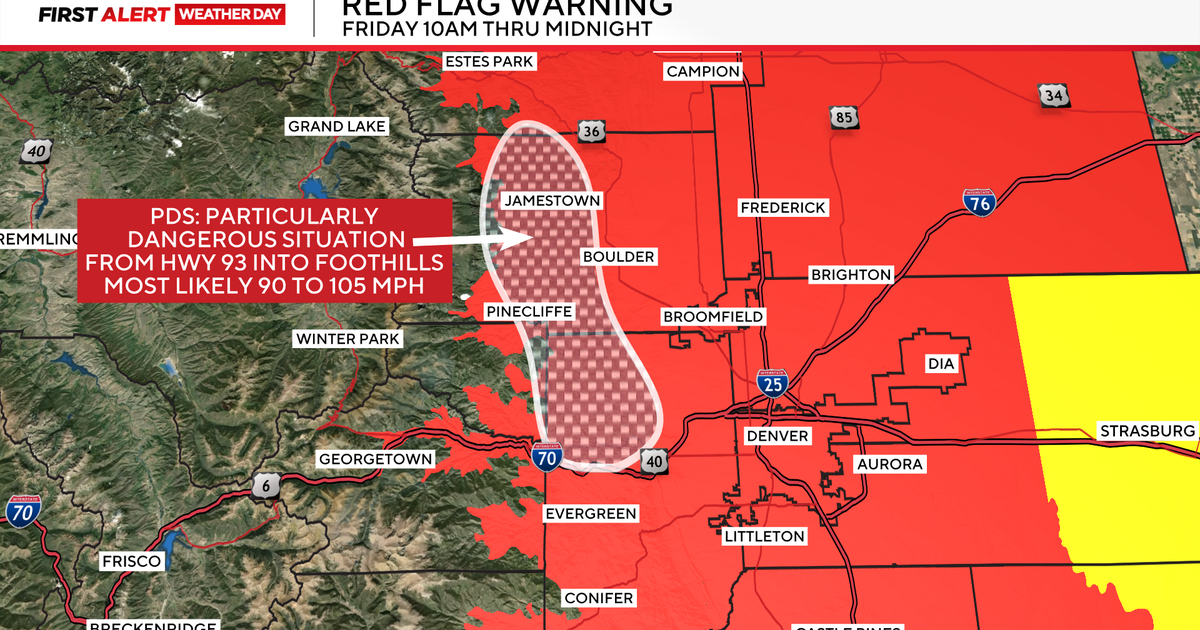

A red flag warning and an unprecedented 'Particularly Dangerous Situation' have been issued for parts of Colorado's Front Range for Friday (10 a.m.–midnight), with forecasted wind gusts of 85–105 mph in northwest Jefferson and western Boulder counties, gusts up to ~40 mph across the Denver metro, single-digit relative humidity and record-tying warm temperatures (Denver potential high ~70°F). The extreme fire-weather confluence—hurricane-force winds, record heat and very low humidity—elevates near-term operational and insured-loss risks for utilities, regional real estate, energy infrastructure and logistics; investors with exposures in Colorado should monitor burn bans, emergency declarations and potential disruption to local operations and insurance loss estimates.

Market structure: Acute wind-driven wildfire risk creates a two-tier effect — downside for regional property & casualty insurers and reinsurers (higher near-term claim frequency) and upside for building-supplies, remediation, and equipment suppliers that capture rebuild/clearing demand. Expect localized pricing power shifts: insurers with concentrated Colorado exposure (homeowners policies) will face rating pressure and potential premium increases of 10–30% over 6–18 months in high-risk ZIPs, while HD/LOW benefit from incremental demand and higher ASPs for replacement goods. Risk assessment: Immediate (0–7 days) is primarily operational — elevated equity/option volatility and potential physical asset loss; short-term (1–3 months) brings claims accrual, reserve adjustments, and reinsurance retro pricing; long-term (3–24 months) could see structural repricing of insurance in Front Range and wider spreads on Colorado munis if payouts exceed municipal budgets. Tail risk: a multi-county conflagration generating insured losses >$1B would materially widen P/C spreads and push reinsurance rates up 20–40% at next renewal. Trade implications: Tactical hedges and event trades are preferred — buy short-dated puts on insurers and call spreads on home improvement retailers; reduce long-duration muni exposure and increase cash/short-term Treasuries for 30–90 days. Cross-asset: expect a knee-jerk bid in oil/propane local logistics if shut-ins occur (limited national impact), a small widening in municipal credit spreads (bps move measurable within 3–10 days), and elevated equity implied vols for regional names. Contrarian view: The market may over-penalize national insurers with diversified footprints — if losses remain sub-$300M, names like TRV/ALL could mean-revert within 4–8 weeks. Historical parallels (Colorado 2012) show rapid repricing and recovery; monitor hard data (insurer loss notices, fire containment %) before scaling. Key trigger thresholds: insured loss >$500M — scale hedges; containment >70% within 7 days — unwind most shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35