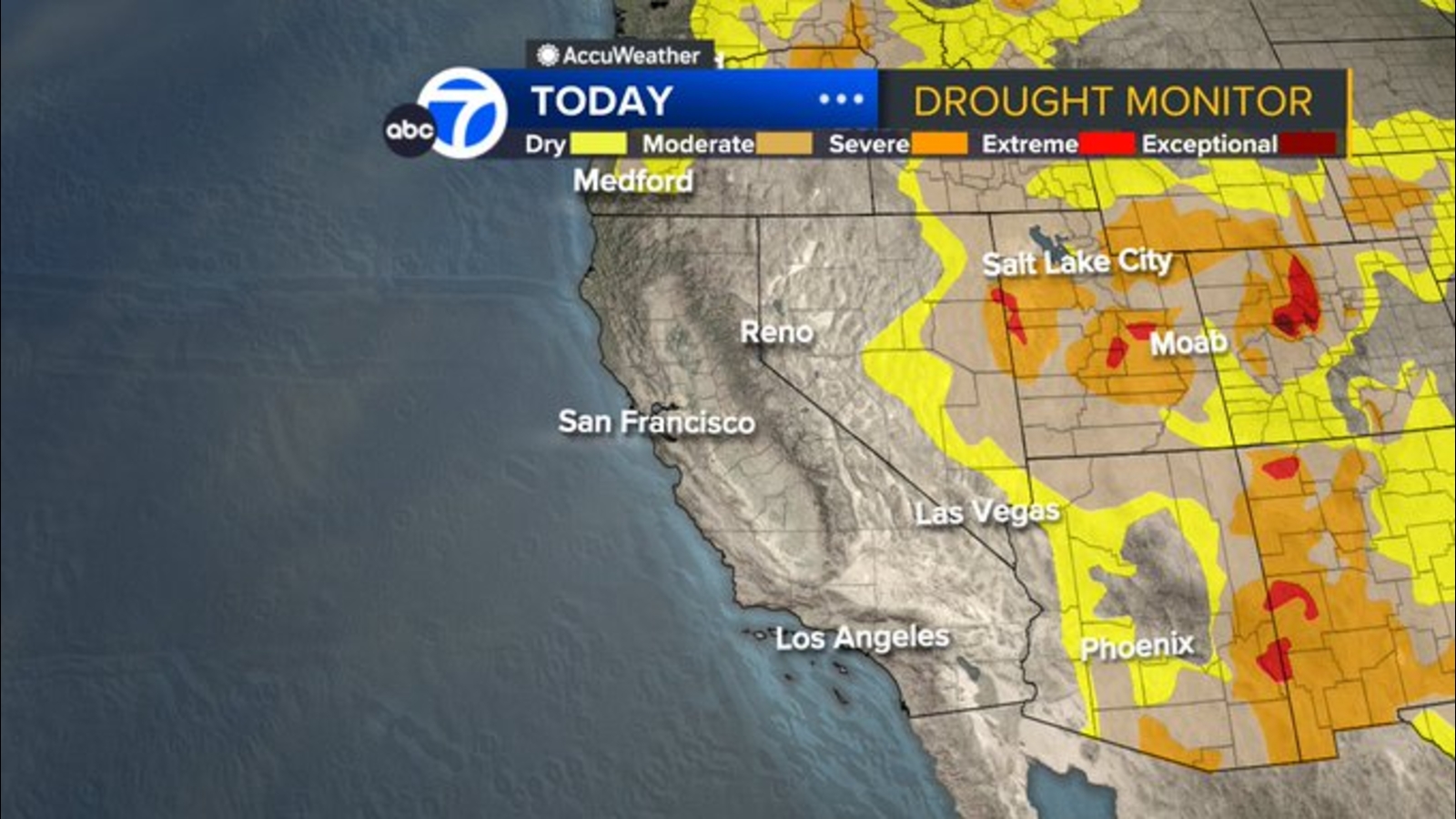

California is effectively drought-free for the first time in 25 years: the U.S. Drought Monitor reports 0% of the state's area in drought as of Dec. 30, 2025, with follow-up measurements on Jan. 8, 2026 showing virtually no dryness remaining. Heavy December storms and multi-year strong rainfall have pushed systemwide reservoir levels higher, with seven of 12 major state-owned reservoirs at 75% or more capacity, materially reducing near-term water stress for agriculture, municipalities and water-dependent economic activity.

Market structure: Wet conditions benefit California water utilities (e.g., CWT, AWR, WTRG), irrigation and water-technology suppliers (XYL, LNN, TTC), and civil engineers (J, ACM) through normalized supply, lower emergency water purchases and a shift to maintenance capex. Losers include short‑duration water spot traders, some upstream freshwater asset plays, and marginal gas peaker generation (NRG) as increased hydro reduces summer supply stress; expect CAISO spark spreads to compress an estimated 5–15% in summer 2026 if reservoirs remain ≥70% into May. Risk assessment: Tail risks include a rapid ENSO flip or two dry winters reversing benefits within 12–36 months, mandated reservoir releases causing flood damage and liability, and regulatory shifts (state funding moving from desalination to ecosystem restoration). Immediate (days–weeks) effects: tighter muni bond spreads for water agencies; short term (3–9 months): agricultural yield normalization and commodity price pressure; long term (1–5 years): capex reallocation from emergency supply to resilience and groundwater recharge projects. Key hidden dependency: groundwater recharge and snowpack melt timing—reservoir percent full is necessary but not sufficient for durable relief. Trade implications: Tactical plays favor selective longs in regulated water utilities (CWT, AWR) and irrigation equipment (LNN, XYL) with 6–12 month horizons, and short/put exposure to California peaker/generator stocks (NRG, PCG) into summer 2026. Use muni water revenue bonds (5–10yr) when spread to Treasuries >50bps to capture expected tightening. Options: buy 3–6 month call spreads on LNN/XYL to capture capex re-rating and buy put spreads on NRG for downside if CA spark spreads compress >10%. Contrarian angles: Consensus underestimates the persistence of allocation rules and groundwater deficits—wet reservoirs can coexist with stressed groundwater, sustaining demand for irrigation tech and recharge projects (benefit to LNN/XYL beyond a single season). Reaction may be underdone for engineering/infrastructure firms (J, ACM) that win large mitigation contracts; conversely, shorting desalination pure‑plays may be crowd‑pitched but premature if policy pivots to long‑term resilience. Monitor snow water equivalent (SWE) and CA Drought Monitor changes as 30–90 day catalysts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45