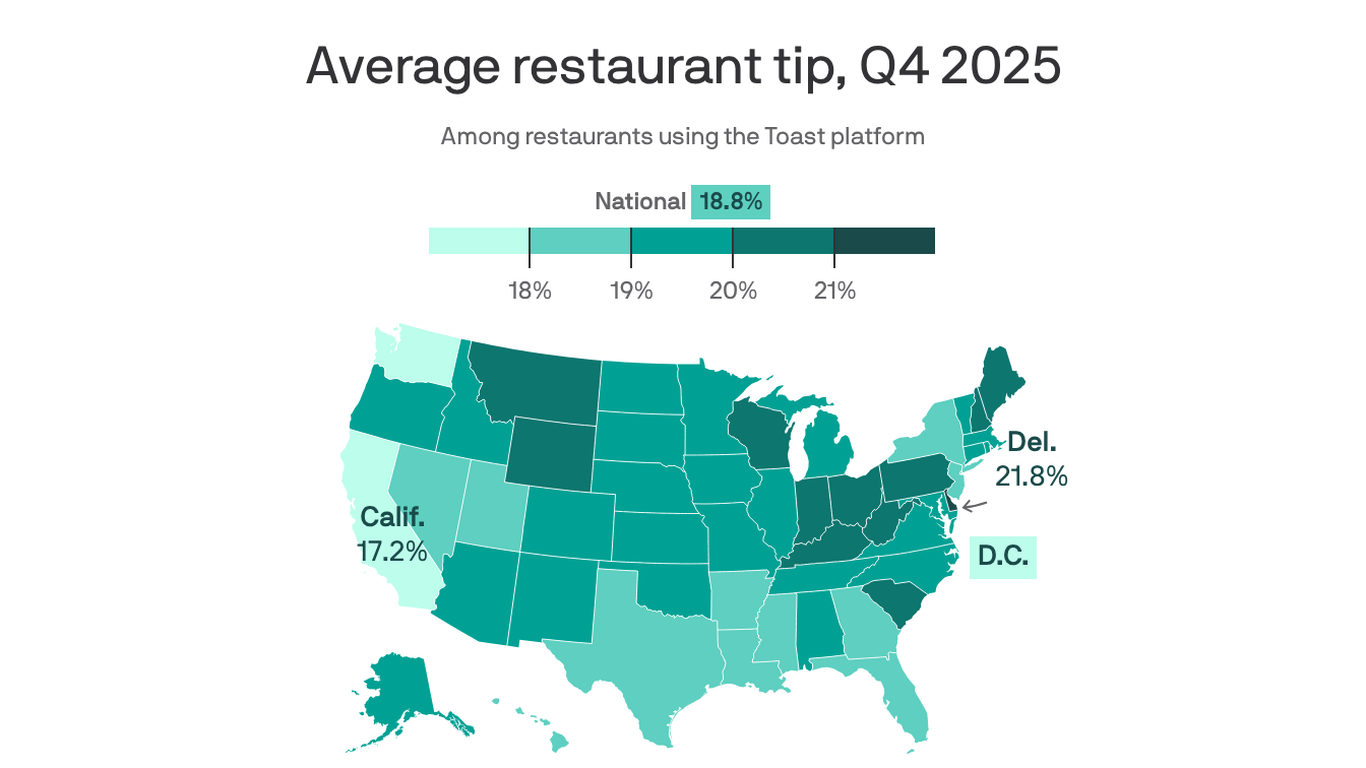

17.2% was the average tip left in California — the lowest on Toast — while nationwide tips at full-service restaurants using Toast averaged 19.2% in Q4 2025, unchanged from the prior quarter. Fast-food tips held at 15.8%, Delaware had the highest average at 21.8%, and the report covers only Toast platform transactions and excludes cash tips, limiting the sample.

Toast’s core revenue rests on two linked levers: dollar volume processed and SaaS spend per merchant. Digital tipping mechanics materially increase per-check dollar volume without meaningful incremental cost for the platform, so stable-to-rising card-tip acceptance converts directly into recurring processing revenue and longer merchant stickiness via deeper POS integration. Expect this coupling to show up in unit economics as higher take-rates on incremental transactions rather than a step-change in subscription revenue. Geographic heterogeneity in tip behavior is a leading indicator for how restaurants will restructure pay and pricing. Markets with weaker tipping create pressure for operators to implement service charges, higher menu prices, or shift wages onto payroll — each move changes cashflow timing, tax treatment, and whether amounts flow through Toast’s processing rails. States that historically lead in labor regulation could force quicker adoption of service charges, compressing servers’ card-tip volume and altering processed-dollar growth at the merchant level within 6–18 months. Competitive dynamics favor POS vendors that control the final checkout UX because suggested-tip prompts are low-friction revenue levers; that strengthens Toast’s moat against generic acquirers but also opens regulatory risk (consumer protection scrutiny of suggestive tipping) and technical risk from card network rules. A regulatory or card-fee change that reclassifies service charges or caps interchange on gratuities would be the fastest lever to dent Toast’s processing growth. Key catalysts to watch: state-level wage/tip legislation and any major card-network guidance on gratuity routing (both plausible in 3–12 months), quarterly merchant-addition and payment-volume cadence (near-term), and consumer spending elasticity if operators push mandatory service fees (6–18 months). Tail risks include a coordinated move by large chains to bypass third‑party tipping flows (routing service charges off-platform) which would convert processed-dollar growth into non-TOST payroll expense within 12–24 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment