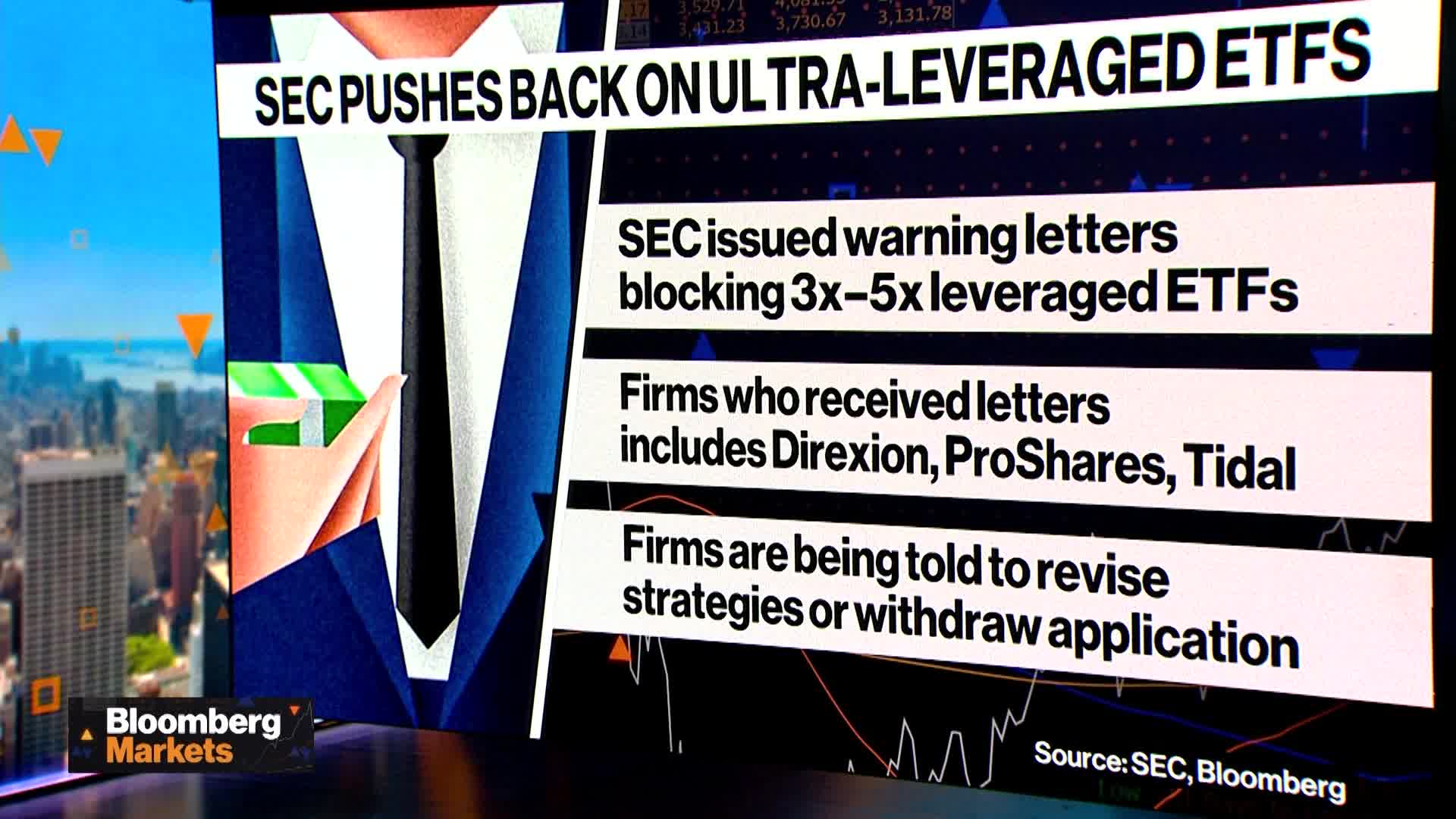

Issuers have been filing to launch leveraged single-stock and crypto ETFs using swaps and options to target 2x–5x exposure, attempting to push around a 2020 derivatives rule that roughly caps portfolio leverage at about 2x. Regulatory scrutiny — including companies like ProShares withdrawing triple-leveraged crypto applications — and the acute liquidation risk on large intraday moves (a ~50% single-day swing can destroy a 2x product) make these vehicles particularly hazardous for retail investors and a potential source of market volatility.

Market structure: Blocking or constraining 3x/5x single‑stock and crypto leveraged ETFs favors large custodial/ETF incumbents and clearing banks (BNY Mellon BK, State Street STT) that can market compliant 2x products and earn fee/settlement revenue; small issuers and retail platforms that rely on exotic product churn will lose distribution and fee income. Issuers of swaps and prime brokers (GS, JPM) face higher margin and legal risk if systemic liquidations occur, but near‑term revenue from derivatives will persist if demand for leverage remains. Supply/demand: demand for retail leverage is intact, but supply of structurally safe leverage is tightening — expect downward pressure on product innovation versus elevated retail flows into alternatives (options, CFDs). Cross‑asset: a liquidation of leveraged single‑stock ETFs would spike equity options/VIX and create funding/liquidity stress in short‑dated repo and prime broker funding; modest knock‑on to USD liquidity and commodity vols if concentrated names are commodity‑linked. Risk assessment: Tail risks include a forced liquidation event that triggers >30% intraday moves in one or more large single stocks, cascading margin calls and a 50–150% jump in VIX within 48 hours; regulatory tail risk is a broad prohibition on single‑name leverage that would compress issuer revenue 10–30% over 12 months. Time horizons: immediate (days) = volatility around filings/withdrawals; short (weeks–months) = re‑filings or SEC rule clarifications and shelfing; long (quarters) = permanent product mix shift toward capped leverage and higher compliance costs. Hidden dependencies: counterparty credit at prime brokers, ETF NAV calculation liquidity, and broker margin models — weakness in any can amplify losses; catalysts include high‑profile retail liquidations, SEC guidance or a market shock (earnings, macro) that moves a single name >33% in a day. Trade implications: Favor trade funding/clearing incumbents (long BK, STT) with 6–12 month horizon sized 2–3% each, and buy protective volatility: a 3‑month VIX 30/50 call spread (cost ~0.5–1% portfolio hedge) to cover a liquidation event. Short selective retail brokers with outsized crypto/leveraged revenue exposure (small 1–2% short in HOOD) for 3–6 months; cover on regulatory relief or if HOOD declines >30%. Avoid primary market participation in new 3x single‑stock ETFs until they survive 60–90 trading days without intraday >33% moves and until counterparty collateral terms are public. Contrarian angles: The consensus that all leverage issuance is bad misses demand migration: retail may shift into listed options, structured notes, or CFD providers — trade idea is to long listed options flow beneficiaries (ICE/ CBOE derivatives franchises) over 6–12 months. The panic view is likely overdone: if SEC enforces a 2x cap, incumbents will monetize via fee increases and structured products, creating a multi‑quarter re‑rating opportunity for large diversified asset managers (BLK, IVZ) that can reprice product suites. Unintended consequence: tighter exchange‑traded leverage could push risk into OTC/CFT venues with far less transparency, increasing systemic counterparty risk — justify active tail hedges until rules and filings stabilize (30–90 days).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45