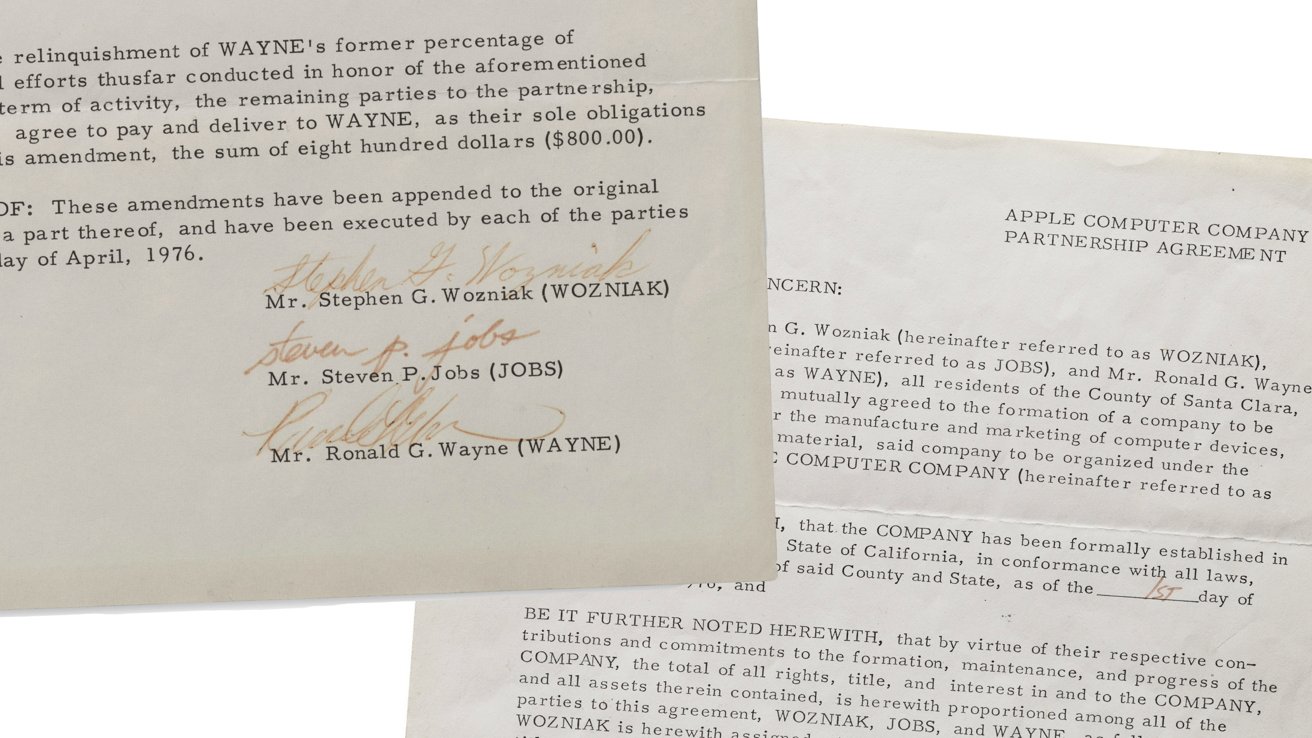

Christie's will offer the original three-page founding agreement of the Apple Computer Company at auction on January 23, 2026, with an estimated price of $2–4 million. The document, signed by Steve Jobs, Steve Wozniak and Ron Wayne, records original ownership stakes of 45%/45%/10%; Wayne sold his stake in April 1976 for $800 (plus a later $1,500), a decision often noted for its historical value given Apple's current market cap. Previously sold in 2011 for $1.5 million, the lot underscores strong collector demand for tech-origin memorabilia but is unlikely to have material impact on Apple’s financials or equity markets.

Market structure: the Christie's lot is a win for auction houses, high‑net‑worth sellers and luxury consumer names because it reinforces scarcity-driven pricing for tech memorabilia; winners include AAPL via brand halo and luxury equities where HNW spend concentrates. It has no measurable impact on Apple’s fundamentals or market share in devices — pricing power shift is intangible and likely to move sentiment by <1–2% around publicity windows. Risk assessment: tail risks are provenance/legal disputes or fraud that could dent the narrative (low probability, high reputational cost), and a collapse in HNW liquidity if rates spike (medium tail). Immediate (days) impact = PR spike around Jan 23, 2026; short term (weeks/months) = tiny sentiment lift; long term (quarters/years) = marginal support for premium positioning if HNW demand remains strong. Trade implications: prioritize small, defined‑risk exposure to AAPL (symmetry: capture brand halo without assuming fundamental change). Options (9–15 month) call spreads or small delta longs are preferred to outright equity; consider relative longs vs mass‑market OEMs (DELL, HPQ) to express pricing power. Rotate modestly into luxury/HNW proxies (e.g., LVMUY) where collectible demand maps to revenue resilience. Contrarian angles: consensus treats this as PR noise — underweights the persistent rise in HNW allocable assets which can sustain luxury/collector valuations for 1–3 years. Reaction risk is that memorabilia mania is cyclical and can reverse quickly if macro liquidity tightens; avoid extrapolating a single auction into structural demand for consumer device upgrades.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.10

Ticker Sentiment