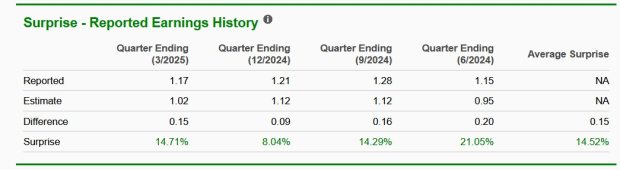

C.H. Robinson (CHRW) is forecast to report a 5.87% year-over-year revenue decline to $4.22 billion for Q2 2025, attributed to the divestiture of its Europe Surface Transportation business, decreased North America truckload volume, and lower ocean services pricing. While CHRW historically boasts an average earnings beat of 14.52% and reported a Q1 2025 EPS beat of $1.17, its Q2 earnings outlook is less certain; the consensus EPS estimate has been revised downward to $1.17, and the Zacks model does not conclusively predict a beat.

C.H. Robinson (CHRW) is approaching its second-quarter 2025 earnings with significant top-line headwinds, as consensus estimates project a 5.87% year-over-year revenue decline to $4.22 billion. This anticipated decrease is attributed to multiple factors, including the divestiture of its Europe Surface Transportation business, reduced volume in North American truckload services amid softer freight demand, and persistent pricing pressure in its ocean services segment. The weakness appears systemic across business units, with forecasted revenue declines of 0.8% in North American Surface Transportation, 14.9% in Global Forwarding, and 18.3% in its All Other and Corporate division. While the consensus EPS estimate of $1.17 suggests a modest 1.74% YoY growth, this figure has been revised downward by 1.68% over the past 60 days, indicating deteriorating analyst sentiment. The company's strong history, marked by an average earnings beat of 14.52% over the trailing four quarters, is now juxtaposed with a less favorable quantitative outlook; a negative Earnings ESP of -2.27% and a Zacks Rank #3 (Hold) suggest a low probability of an earnings surprise, creating a cautious setup for the upcoming report.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment